Cyber security is an essential part of keeping your patients, data and business protected online.

With Samera Cyber Security, you get the tools you need, the know-how to use them and digital copies of all your data. This three-pronged approach means you can keep your business safe and your data safe.

Contact us today to find out more about how our cyber security training, digital protection products and back-up contingencies can help you.

Cyber security is an essential part of keeping your patients, data and business protected online.

With Samera Cyber Security, you get the tools you need, the know-how to use them and digital copies of all your data. This three-pronged approach means you can keep your business safe and your data safe.

Contact us today to find out more about how our cyber security training, digital protection products and back-up contingencies can help you.

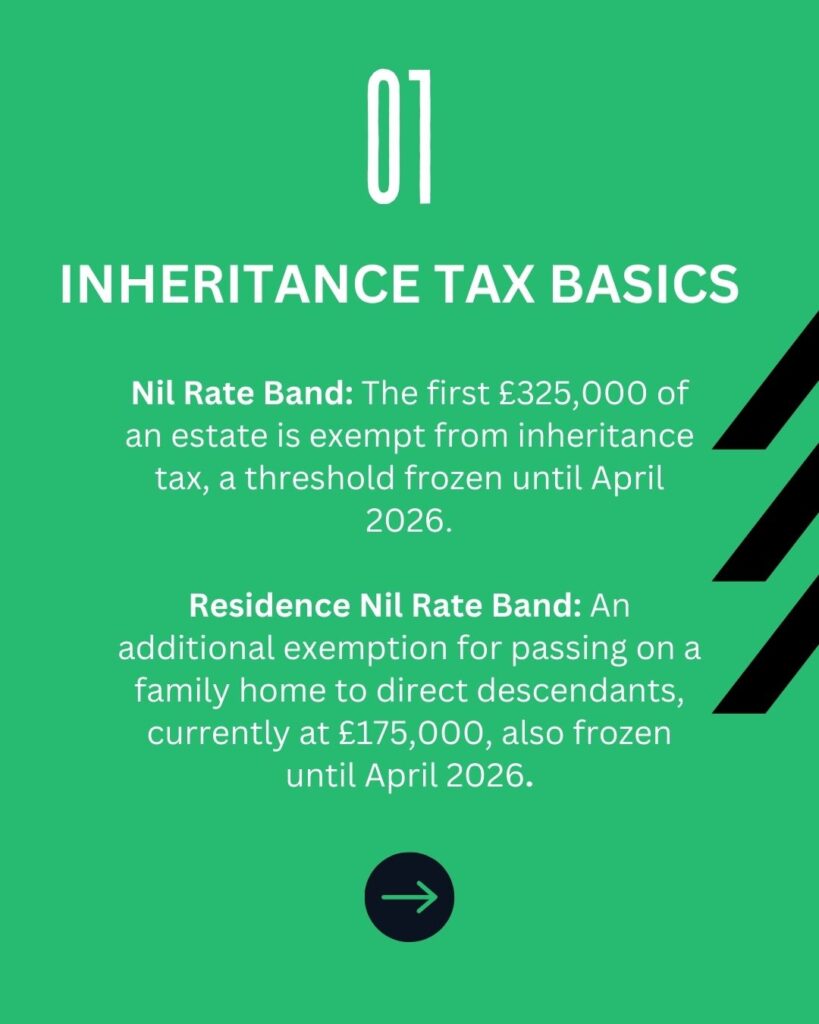

The inheritance tax nil rate band has been frozen at its current level of £325,000 since 6th April 2009. The nil rate band is the amount of your estate that is exempt from inheritance tax.

It will remain at its current level of £325,000 until 5th April 2026 – a 17-year freeze! However, since 6th April 2017, a new additional nil rate band has been available for the ‘family home’.

Generally speaking, effective inheritance tax planning should be carried out on a long-term basis. However, it is worth remembering the following points, which should be considered on an annual basis.

Annual exemption

The first £3,000 of gifts made by any individual during each tax year is completely exempt for inheritance tax. In addition to this, if the previous year’s annual exemption was not fully utilised, it can be carried forward into the following (current) tax year.

This means, in one tax year you are able to have up to £6000 of gifts that will be exempt from any tax only if you have not made any gifts during the previous tax year.

This exemption is specific to a per person basis, so married couples can also make gifts of £3,000 each.

Small Gifts Exemption

Gifts of up to £250 per tax year made to any one individual are also exempt from any inheritance tax and do not count towards the annual exemption. These types of small gifts are an exemption for you as you can make as many of these gifts as you like to different people.

However, the annual exemption cannot be used for further gifts to the same recipient in the same tax year.

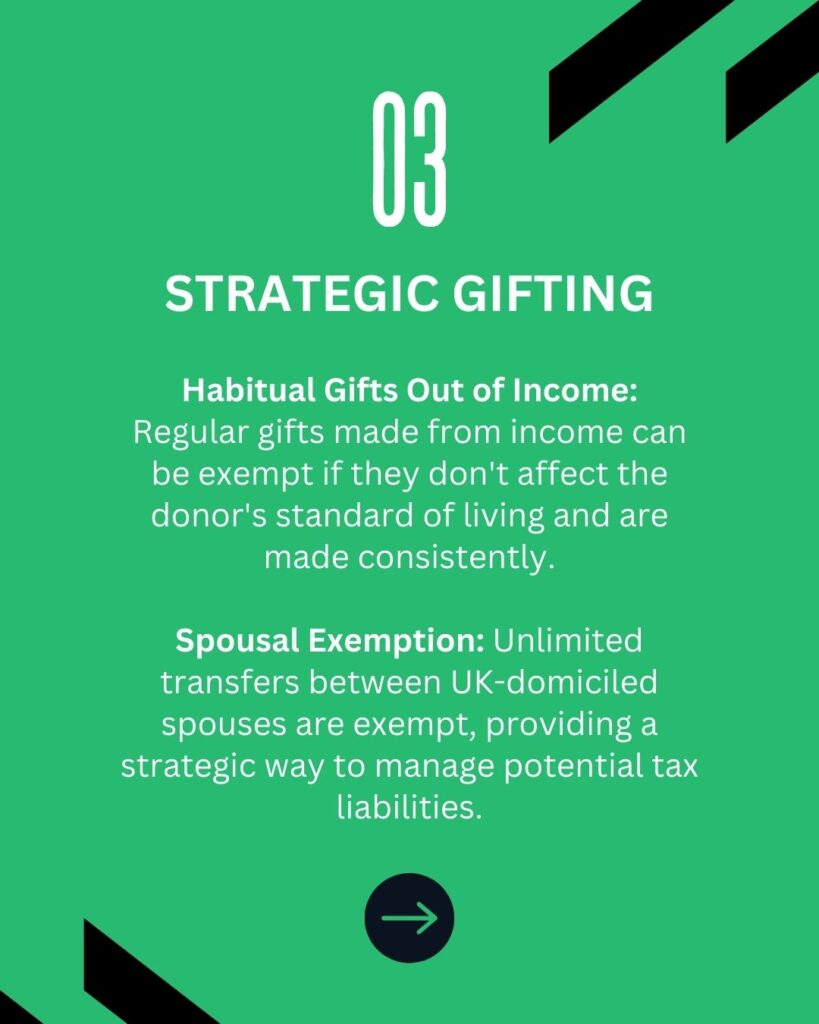

Habitual Gifts Out of Income

Habitual gifts out of income are an exemption from inheritance tax, in order for these gifts to be classed as ‘habitual’, they need to be made consistently for a number of years. Which is why it is important to remember to keep these up every tax year.

The Family Home

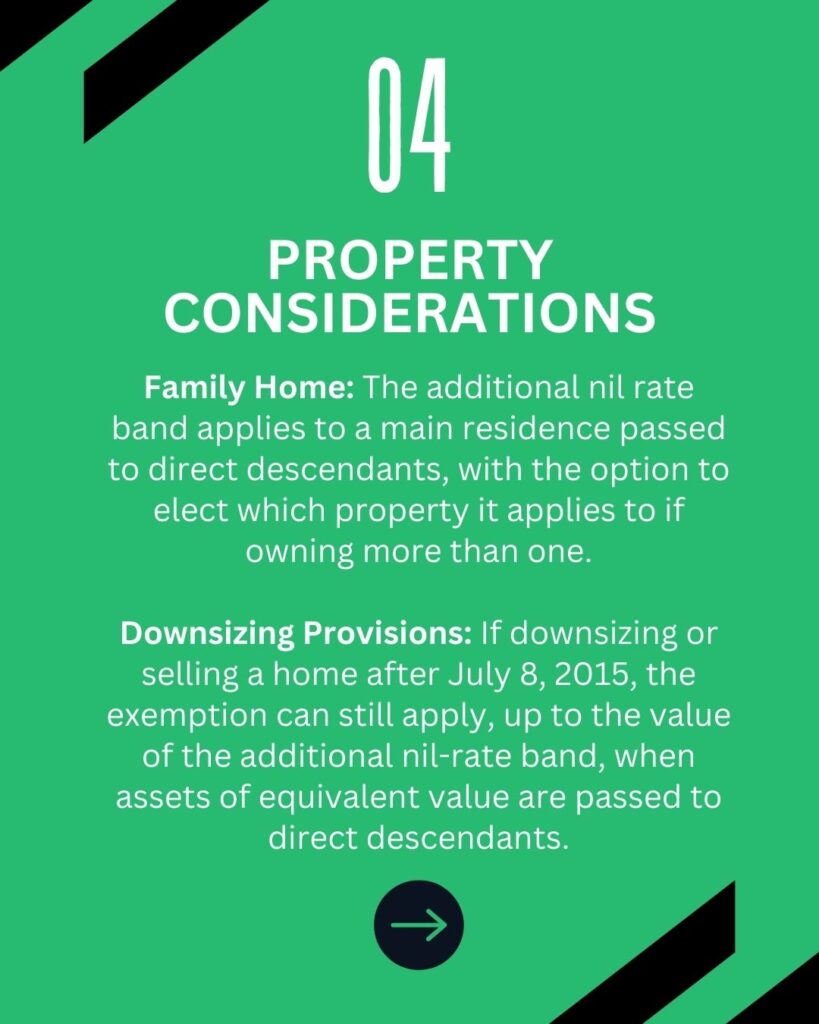

An additional nil rate band is available for the ‘family home’ for any deaths occurring after 6 April 2017. This exemption is only available on a property which has been the deceased residence at some point during their life. If the deceased has passed while owning more than one or multiple qualifying properties, the personal electives can elect which property this exemption should apply to.

The exemption is only applied once the property is passed. This is usually done to a direct descendant of the deceased and in this case, any stepchildren, foster children or adopted children are all accorded the same status as one another for this sole purpose.

Similar to the £325,000 nil rate band, any unused proportion of the exemption will pass to the deceased’s partner or spouse.

When a person downsizes or ceases to own a home after 8 July 2015, the residence nil rate band is available to them as well as assets of an equivalent value, up to the value of the additional nil-rate band, are passed to direct descendants.

The residence nil-rate band that was introduced in 2017/18 and increased from £100,000 to its current value to £175,000. This level is set to remain until 5 April 2026.

Margaret divorced her husband many years before her death in June 2021.

She leaves her estate, worth £600,000, to her daughter.

Margaret’s estate includes her former home, which is worth £250,000 at the time of her death. The residence nil rate band available for 2021/22 exempts £175,000 of the value of Margaret’s former home. This reduces her taxable estate to £425,000 before deduction of her main nil rate band of £325,000, which reduces it to £100,000.

The IHT payable on Margaret’s estate at 40% is thus £40,000. The residence nil rate band is withdrawn from estates worth in excess of £2 million (this threshold is also frozen until 5th April 2026).

This withdrawal is at the rate of £1 for every £2 by which the estate exceeds £2 million. Any mortgages or other loans secured over a property will have to be taken into account when allocating the exemption. For example, where the deceased held a property worth £250,000 which was subject to a mortgage of £180,000, the exemption will be limited to just £70,000.

A Guide to Inheritance Tax FAQ

What is inheritance tax in the UK?

Inheritance tax in the UK is a tax on the estate of someone who has passed away. The estate includes assets such as property, money, and personal possessions. The tax is applied to the portion of the estate that exceeds the tax-free threshold, which is currently £325,000. Anything above this amount may be taxed at a rate of 40%. However, there are exemptions and reliefs available, such as passing assets to a spouse or civil partner, which can reduce or eliminate the tax liability.

How much is the inheritance tax rate in the UK?

The inheritance tax rate in the UK is 40% on the value of an estate that exceeds the tax-free threshold, which is currently set at £325,000. However, if 10% or more of the estate is left to charity, the rate can be reduced to 36%. Additionally, some exemptions and allowances, such as the residence nil-rate band, can further reduce the taxable amount.

Who pays inheritance tax on an estate?

Inheritance tax on an estate is typically paid by the executor of the will or the administrator if there is no will. The tax is paid using funds from the estate before assets are distributed to the beneficiaries. Beneficiaries usually do not pay inheritance tax directly, unless they receive certain types of gifts or trusts that may have specific tax implications. If the tax isn’t paid on time, interest may be charged on the amount owed.

What is the current inheritance tax threshold?

The current inheritance tax threshold in the UK is £325,000. This is known as the nil-rate band, meaning no inheritance tax is due on estates valued up to this amount. Any part of the estate exceeding this threshold is typically taxed at a rate of 40%. However, the threshold can be increased with the residence nil-rate band, allowing an additional £175,000 if the deceased passes their home to direct descendants, such as children or grandchildren.

Can you avoid paying inheritance tax legally?

Yes, there are several legal ways to reduce or avoid paying inheritance tax in the UK:

Gifting Assets: You can give away assets during your lifetime. Gifts made more than 7 years before your death are typically exempt from inheritance tax under the “7-year rule.”

Spouse or Civil Partner Exemption: Anything left to your spouse or civil partner is exempt from inheritance tax.

Charitable Donations: Gifts to charities are inheritance tax-free, and if you leave 10% or more of your estate to charity, the tax rate on the remaining estate can be reduced from 40% to 36%.

Trusts: Placing assets in a trust can reduce the inheritance tax liability by removing them from your estate.

Residence Nil-Rate Band: Passing your home to children or grandchildren can increase your tax-free threshold by an additional £175,000.

Life Insurance: A life insurance policy can be set up to cover the inheritance tax liability, ensuring that beneficiaries don’t have to sell assets to pay the tax.

Effective estate planning with these methods can significantly reduce or eliminate the inheritance tax burden.

Are there any exemptions from inheritance tax?

Yes, several exemptions from inheritance tax exist in the UK, including:

Spouse or Civil Partner Exemption: Any assets passed to a surviving spouse or civil partner are exempt from inheritance tax, regardless of the estate’s value.

Charitable Donations: Gifts left to registered charities are exempt from inheritance tax. Additionally, if 10% or more of your estate is donated to charity, the inheritance tax rate on the remaining estate is reduced to 36%.

Annual Gift Exemptions: Each year, you can give away up to £3,000 in gifts without it being counted towards inheritance tax. Unused allowances can be carried forward for one year.

Small Gifts Exemption: Gifts of up to £250 per person per year are exempt, provided the recipient hasn’t benefited from your £3,000 annual allowance.

Gifts Between 7 Years of Death: Gifts made more than 7 years before death are typically exempt under the “7-year rule.”

Residence Nil-Rate Band: An additional £175,000 tax-free allowance is available if you pass your home to direct descendants like children or grandchildren.

These exemptions can significantly reduce or eliminate inheritance tax liability.

What is the 7-year rule for inheritance tax on gifts?

The 7-year rule for inheritance tax in the UK applies to gifts you make during your lifetime. According to this rule, if you gift assets and survive for 7 years after making the gift, the gift will be exempt from inheritance tax.

If you pass away within 7 years of making the gift, the gift may still be subject to inheritance tax. However, the tax rate can decrease on a sliding scale, known as taper relief, depending on how many years have passed since the gift was made:

Less than 3 years: 40% (full inheritance tax rate) 3 to 4 years: 32% 4 to 5 years: 24% 5 to 6 years: 16% 6 to 7 years: 8% After 7 years: 0% (no inheritance tax)

This rule allows you to reduce inheritance tax by gifting assets early in life.

How does the residence nil-rate band affect inheritance tax?

The residence nil-rate band (RNRB) is an additional tax-free allowance that can reduce inheritance tax when you pass your home to direct descendants, such as children or grandchildren. It works alongside the standard inheritance tax threshold and can significantly increase the amount of your estate that is exempt from tax.

Key Points:

Additional Allowance: As of now, the RNRB provides an extra £175,000 on top of the standard inheritance tax threshold of £325,000. This means your estate could potentially pass on up to £500,000 tax-free, if the home is included.

Married Couples and Civil Partners: If you’re married or in a civil partnership, any unused allowance can be transferred to your partner, allowing a combined tax-free threshold of up to £1 million.

Eligibility: The RNRB applies only if you leave your primary residence to direct descendants (children, stepchildren, grandchildren, etc.). It doesn’t apply if you leave your home to other relatives or friends.

Estates Over £2 Million: For estates valued over £2 million, the RNRB is reduced by £1 for every £2 over the threshold. This is known as the tapering effect, which can eventually eliminate the RNRB for very large estates.

The residence nil-rate band can help reduce or even eliminate inheritance tax on the value of your home when passed to your heirs.

Do gifts reduce inheritance tax liability?

Yes, gifts can reduce inheritance tax liability if structured correctly. Several rules and exemptions apply to gifts that can help minimize the amount of inheritance tax due:

Key Ways Gifts Reduce Inheritance Tax:

The 7-Year Rule: Gifts made more than 7 years before your death are exempt from inheritance tax. If you survive for 7 years after making the gift, it will not count towards the value of your estate.

Annual Exemptions: You can give away up to £3,000 per tax year without it being counted towards inheritance tax. If unused, this allowance can be carried over for one year, allowing up to £6,000 in tax-free gifts.

Small Gifts Exemption: You can give gifts of up to £250 to any number of individuals each tax year, as long as these gifts don’t exceed £250 per recipient.

Gifts for Weddings or Civil Partnerships: Gifts to a child for their wedding or civil partnership are exempt up to £5,000; for a grandchild or great-grandchild, the limit is £2,500, and for others, it’s £1,000.

Regular Gifts from Income: If you can prove that you regularly give gifts from your surplus income and it doesn’t reduce your standard of living, these gifts may be exempt from inheritance tax. This is called “normal expenditure out of income.”

Charitable Donations: Any gifts left to charity are completely free from inheritance tax. Additionally, leaving 10% or more of your estate to charity can reduce the overall inheritance tax rate from 40% to 36%.

Using these gift exemptions effectively can help reduce the overall size of your taxable estate, lowering or even eliminating the inheritance tax liability.

How do trusts help with inheritance tax planning?

Trusts are a valuable tool for inheritance tax planning because they allow individuals to control how their assets are distributed while potentially reducing the amount of inheritance tax (IHT) due. Here’s how trusts can help with inheritance tax planning:

Life Interest Trusts:

These trusts allow a beneficiary (often a spouse) to benefit from income generated by the trust during their lifetime, while the assets themselves are passed to other beneficiaries (like children) after their death. The trust can provide for a spouse while reducing the taxable value of the estate for IHT purposes.

Removing Assets from the Estate:

When you place assets in a trust, they are no longer considered part of your estate for inheritance tax purposes, provided you survive for 7 years after transferring the assets. This can significantly reduce the value of your taxable estate.

Controlling Asset Distribution:

Trusts allow you to set specific conditions on how and when beneficiaries receive the assets. This helps protect wealth for future generations and ensures assets are not taxed multiple times as they pass from one generation to the next.

Potential IHT Relief on Business Assets:

Certain types of trusts, such as business property relief trusts, allow business assets to be transferred while reducing or eliminating inheritance tax liability, particularly if the assets qualify for business relief or agricultural relief.

Gifting with Trusts:

Trusts can facilitate tax-efficient gifting. For example, bare trusts allow gifts to minors, and provided the donor survives for 7 years, the assets in the trust won’t be subject to IHT.

Protection from the 40% IHT Rate:

Trusts like discretionary trusts allow assets to be held for future beneficiaries without giving them direct access. While discretionary trusts may have their own tax rules, they can offer greater protection and flexibility compared to leaving assets directly, which are taxed at 40%.

Avoiding Double Taxation:

Trusts can help avoid double taxation. For example, instead of passing assets directly to children (who may also be liable for IHT later), assets can be placed in a generation-skipping trust, which can reduce IHT when passed on to grandchildren.

By using trusts, individuals can manage their estate more effectively, potentially minimizing inheritance tax liabilities and ensuring assets are distributed according to their wishes. Trusts should be set up with professional advice to ensure they are structured in compliance with tax laws and estate planning goals.

Do pensions count towards inheritance tax?

In most cases, pensions do not count towards inheritance tax (IHT) in the UK. Here’s a breakdown:

Defined Contribution Pensions:

Not subject to IHT.

If you die before age 75, beneficiaries inherit tax-free.

If you die after age 75, beneficiaries pay income tax on withdrawals.

Defined Benefit Pensions:

Typically, it is not part of your estate for IHT. Survivor pensions are also IHT-exempt.

Lifetime Annuities:

Usually die with you unless death benefits are included, which may also be exempt from IHT.

Drawdown Pensions:

Remaining funds are not subject to IHT; withdrawals after age 75 are taxed as income.

Exception:

Moving pension funds out deliberately to avoid IHT could bring them back into your estate for tax purposes.

In summary, pensions are generally exempt from IHT, making them a tax-efficient way to pass on wealth. Proper planning ensures beneficiaries receive them with minimal tax implications.

Can life insurance cover inheritance tax costs?

Yes, life insurance can be used to cover inheritance tax (IHT) costs. A life insurance policy can be structured to provide your beneficiaries with funds to pay the inheritance tax due on your estate, ensuring they don’t have to sell assets to cover the tax bill.

How it works:

Whole-of-Life Policy: A whole-of-life insurance policy can be taken out, which guarantees a payout upon death, providing funds to cover IHT costs.

Writing the Policy in Trust: For the payout to be exempt from IHT, the life insurance policy should be written in trust. This ensures that the payout does not form part of your taxable estate and goes directly to your beneficiaries or an executor to pay the IHT.

Covering Tax Liabilities: The insurance payout can match the estimated IHT liability, allowing your beneficiaries to cover the tax without selling property or other assets.

Benefits:

Liquidity: Provides immediate funds to pay IHT, avoiding delays or forced asset sales.

Exempt from IHT: When written in trust, the payout is not subject to inheritance tax.

Peace of Mind: Ensures your estate passes to your beneficiaries without financial burden.

In summary, life insurance is a practical solution to cover inheritance tax costs, ensuring your assets are passed on as intended without the risk of liquidation.

What is taper relief for inheritance tax on gifts?

Taper relief reduces the amount of inheritance tax (IHT) on gifts made between 3 and 7 years before your death. It applies to gifts that exceed the £325,000 inheritance tax threshold and are subject to tax if you pass away within 7 years of making the gift. The longer you live after making the gift, the lower the tax rate on that gift.

Taper Relief Breakdown:

Less than 3 years: 40% (full inheritance tax rate)

3 to 4 years: 32%

4 to 5 years: 24%

5 to 6 years: 16%

6 to 7 years: 8%

After 7 years: 0% (no inheritance tax)

Key Points:

Taper relief only reduces the tax on the gift, not the value of the gift itself.

It applies only if the total value of gifts in the 7 years before death exceeds the IHT threshold.

In summary, taper relief can significantly reduce the tax on large gifts, making gifting an effective estate planning tool if done early.

When does inheritance tax need to be paid?

Inheritance tax (IHT) needs to be paid by the end of the sixth month after the person’s death. If not paid by this deadline, interest will be charged on the amount owed.

Key Points:

Deadline: IHT must be settled within 6 months of the individual’s death.

Who Pays: The executor or administrator of the estate is responsible for ensuring the tax is paid.

Payment in Instalments: If the estate includes assets like property, the tax can be paid in instalments over 10 years, although interest will still accrue on unpaid amounts.

Advance Payments: Some tax can be paid before the final valuation of the estate is complete to reduce interest charges.

Paying IHT on time is crucial to avoid additional interest costs.

How can I plan effectively to reduce inheritance tax on my estate?

To effectively reduce inheritance tax (IHT) on your estate, consider these strategies:

Business Property Relief (BPR):

Invest in qualifying businesses to potentially reduce the IHT on those assets by up to 100%.

Utilize Gift Allowances:

Use your annual gift allowance of £3,000 per year (or £6,000 if you didn’t use the previous year’s allowance) to reduce the size of your estate.

Give small gifts of up to £250 per person, which are exempt from IHT.

Make Gifts Early:

Gifts made more than 7 years before your death are IHT-free, so consider gifting assets early to take advantage of the 7-year rule.

Use Trusts:

Place assets in trusts to reduce the value of your estate for IHT purposes. Trusts allow you to pass wealth to beneficiaries while controlling how and when they receive it.

Maximize Exemptions:

Leave assets to a spouse or civil partner, as they are exempt from IHT. Additionally, leave assets to charity to avoid IHT and reduce the tax rate to 36% if 10% or more of your estate is donated.

Residence Nil-Rate Band:

Pass your home to direct descendants (children or grandchildren) to benefit from the additional £175,000 residence nil-rate band, increasing your tax-free threshold to £500,000 (or £1 million for couples).

Take Out Life Insurance:

A life insurance policy, written in trust, can cover the IHT liability, ensuring your beneficiaries do not have to sell assets to pay the tax.

Pensions:

Keep funds in your pension, as pensions are usually exempt from IHT and can be passed on to beneficiaries tax-efficiently.

Effective planning with professional advice ensures that your estate is structured to minimize IHT and preserve wealth for your beneficiaries.

Further Information on Accounts & Tax

Our team of specialist accountants and tax experts can help manage, process and structure your business’s finances. From management accounts and payroll & pensions to tax planning and cash flow management, we can take care of the full back-office function of your business.

Book a free, no-obligation consultation with one of the team to find out how we can make your accounts & tax easier, quicker and cheaper.

Our in-house finance brokers are former bankers who help general practitioners and primary care specialists raise the finance they need to build and grow their business. You will most likely need different forms of funding to support for primary care business, ranging from buying into a GP practice, refurbishment projects, office space, new equipment or simply to pay your tax bill.

Getting the right financial solutions is essential for you to operate your practice to the best of its ability. We help GPs find the best finance solutions to their needs.

Finance options for GPs

Funding to buy an existing medical practice

You can either buy a GP practice outright or you can buy into an existing practice as a partner. Both of these options require significant funding, as well as a lot of in-depth research carried out by yourself or your team.

This research needs to include the performance of the business if it is an already existing practice and understand its current value as a business, or of the premises alone. The location is everything when it comes to how successful your business will be.

The patient base, the premises and any existing equipment that may be there, as well as the value of any NHS contracts, need to be both assessed and understood before you can begin the process of buying your GP practice.

We can help you arrange the type of finance that will be best suited to you and your business. The two main types of loans that may be useful to you are either a Secured Loan or a Partner Equity Loan.

A secured loan is one answer, with the security of this loan being the practice itself. Partner equity loans are the best option if you are thinking of buying into an already existing larger practice as a partner or a buy-out for an existing partner who may be retiring.

Buy-in and Buy-out finance can also be a great option for you as it can accommodate the challenges of buying in and out of a GP practice, as it is funding tailored to help you make full use of the opportunity.

Don’t be concerned, most lenders are keen to lend finance for GPs for the buy-in loan that you will require, and lenders are not generally seeking additional security to secure the facilities they will lend on an unsecured basis

There are normally two situations when you will be offered the chance to buy into a practice as a partner.

An existing partner is retiring/leaving and wants to sell their share of the partnership

The existing partners would like to bring a new partner in and they will be willing to reduce their current ownership share so you can buy-in.

Either scenario is acceptable to lenders who are used to providing finance for GPs.

Most doctors own the doctor’s surgery where they are based as GPs and can’t sell the goodwill of the practice, so buy-in loans are normally calculated on a percentage of the freehold owned by the partnership.

The partners will all need to agree the percentage that you will need to purchase (most partners would all have an equal ownership share of the practice). Based on a partnership of 4 GP’s with all partners having a 25% ownership and the freehold being valued at £1m, the buy-in amount needed would be £250k.

The freehold value would need to be confirmed by an independent valuer and all the partners must agree to the final buy-in figure.

The majority of buy-in loans agreed are on an unsecured basis, but you can offer additional security if you wanted to secure a lower interest rate. That being said, most lenders will be comfortable funding 100% of the buy-in amount totally unsecured.

Buy-in loans are normally termed over 15-20 years. Some banks will allow you to make lump sum repayments with no charge, which can help reduce the term and allow you to repay the loan earlier if that is your plan.

Most partners earn more than a salaried GP. As a partner you will earn a share of the primary care practice’s profits and a share of the notional rent. The average salary for a partner in England is over £100k.

The loan serviceability will be calculated on your new salary, less tax and your current personal outgoings.

The benefits of becoming a GP partner

Firstly, you have a say in how the practice is run. You will have an input on who the practice employs and what new services the practice can look to offer.

Of course, there is also the increased income. As a partner you will receive a higher salary and notional rent from the practice.

You will now own part of an asset, being the freehold of the practice. Once you come to the point of leaving or retiring from the practice, you would have hoped that the asset would have increased in value and you will receive a higher return on the asset than what you originally paid.

As with most things in life, there are also negatives to becoming a partner.

You will shoulder more of the responsibility. Unlike being a salaried GP, you are responsible for the running of the practice and will have extra duties as a partner.

If the practice has any loans in the partnership name, you will be jointly and severally liable for that facility once you become a partner. Make sure you understand the full financial position at the practice.

What are the other important factors to take into account?

Partnership agreements make sure that you sign an up-to-date copy of the agreement once you become a partner. This will set out their rules and expectations at the practice.

Once you become a partner, you are no longer an employee. You will need to understand sickness, annual leave entitlement, paternity/maternity leave and how the practice deals with any disciplinary matters.

Setting up a new primary care practice

When you are setting up a new General Practice it can be both rewarding and liberating, especially if you are setting up your own private practice. Going private frees you from a lot of the burden that is accompanied by NHS regulations and allows you to spend a lot more time with your patients. Being a private practice means that you do not have any target to meet or any QOF (Quality and Outcomes Framework) points and a lot less government interference with your business.

Whether you are a new start-up or you need funding for your already-established primary care practice, you will need a range of equipment. This equipment can take quite a toll on your expenses.

The type of equipment you may need will include:

X-ray equipment

Equipment sterilizers

IT equipment

Practice room equipment

New or used?

Good quality equipment doesn’t always necessarily mean new equipment, the goal is to get good quality equipment which can also be used. Many business owners miss out on potential savings because they believe that they have to go for brand new equipment.

This is not the case, especially when you are a start-up business, buying good quality used equipment will help you buy the equipment you need for your practice for a fraction of the cost it would have cost you to get the same thing brand new in turn, saving you a lot of money.

Leasing equipment or a vehicle will allow you to get the latest equipment or asset you need without the hefty cost of owning it outright. Leading will give you the flexibility and freedom you need. Leasing also means that any maintenance that needs to be carried out is not your responsibility. These duties lie within the leading company therefore reducing costs for the equipment further down the line.

Hire purchase

Hire purchase is a great solution for you if you need equipment that you want to keep giving you good service for years and years. Hire purchase allows you up to five years to spread the most of most of the different types of equipment your general practice surgery will need.

Tax loans

VAT and tax demands can be a huge strain on any business, especially start-ups. Tax loans can help alleviate some of this stress by allowing you to pay back what is owed at manageable monthly costs.

Vat and tax loans will spread the costs of your taxes into affordable monthly payments there ensuring that you have a surplus of cash flow in your business rather than facing cash flow difficulties due to your tax bills.

A practice loan is a loan solely based on your status as a doctor and your GP service and does not require any security. This loan can provide a relatively high level of funding at very favourable interest rates. Practice loans are not only for start-ups, you can use this loan can be used for many purposes including Buy-ins, cashflow support, any refurbishments or a capital injection for your business.

Working capital finance

Working capital is also known as net working capital. It is a loan that is taken to finance a company’s everyday operations. These loans are not designed to buy long term assets or investments. It is often used for specific growth projects; it is solely designed to boost the working capital available to a business.

One of the first issues to be addressed by a practitioner is where the location of their private services is going to be carried out.

Demographics

There are two important sides that you should look into when looking at demographics. Firstly, you need to consider who your customers are and how important their proximity to your chosen location is. For a general practice, this is critical. You need to ensure that the local residents are affluent enough to continuously use your service.

The demographics you have of your target market should reflect the type of residents that are located in the area you chose your business to be in. The second side is to then look at the community. If your customer base will mostly be locals, which is highly probable for a GP surgery, does a sufficient percentage of the community population match your customer profile in order to support and sustain your business?

Foot Traffic, Accessibility & Parking:

For most retail businesses foot traffic is extremely important. Being a local business, you don’t want to be tucked away in a corner when people are likely to bypass you and not take any notice that your business even exists there.

You also need to consider how accessible the facility will be for everyone who will be using it, this includes customers and employees. If you are on a busy street you need to consider how easy it is for cars to get in and out of allotted parking spaces, you need to consider whether there even is adequate parking for your customers. As a GP practice, you need to also consider disability access.

Local competition

You will not only have other private practices that are your competition, but you will also have NHS practices. You need to know if these competing companies are located nearby, if so, how close are they? Sometimes if you are surrounded by other practices that are also private, comparison shopping may work in your favour depending on if your prices, reviews and services are more favourable than your competitors. You may also catch the overflow from existing businesses which could be a positive thing for you.

Proximity to other businesses

Look at the proximity of other businesses to your business. If you can see if you reap any benefits from these businesses being located next to you it will be great. You may be able to benefit from them by the customer traffic they generate. This is because those companies and their employees and even their own customer base could become your customers.

Although the aim for your practice is to help people, the end goal for your business is to make money, specifically, to make a profit and to pay yourself as well as any staff you have an income. The reality of your business will be, in the private sector, time is quite literally money and the more time you spend in your business, the more money you will be able to make. Unlike with NHS practices, you will only get paid for the specific services you provide.

When you are starting up, you will need enough income in order to cover the various set up costs including funding the premises, tax requirements as well as paying your staff and yourself a decent salary. Your profit will not be evident within the first couple of months at least, therefore, you will need enough funding to cover these costs over the first couple months while you start up.

Private or NHS

There is also the risk that your practice may not succeed in the way you think it will, which means that you should always be open to continuing your medical services with the NHS. The very popular perception that private GPs earning much larger sums of money is often untrue and should not be the primary reason to get up a private practice.

There are a variety of factors to consider when setting up in private practice. Remember, the grass is not always greener on the private side rather than the NHS. With the NHS, there is a lot more security for your business. It is also important to note that NHS indemnity schemes do not cover any private work therefore it is essential that all private practitioners have an adequate level of indemnity cover from one of the medical defence bodies. That being said, having a private practice can be quite lucrative.

Taxes

One of the first things you need to do within the first three months of starting your General Practice is to register with HMRC that you are starting a private practice that is fee charging. If you fail to do this, it is likely that you will be charged a fine.

Bookkeeping

Even though you are in the healthcare sector, at its core, your practice is a business that needs a separate business bank account to keep track of cash flow and taxation for all the doctors in the practice. You will need to develop a form of bookkeeping that is well organised and easy to use and understand.

Your GP services

Everyone needs a GP at some point, but what you are competing against is free NHS GPs. So, you need to make sure that you have a market for the primary care services you are offering. Most private general practices are in quite affluent areas where there is a high density of people who can afford the services that you will be providing.

Patients accessing your service will also expect a higher level of service since they are paying for a service that they could otherwise get for free. They will expect to get same-day appointments, longer appointment times and greater access with the doctor.

Applying for funding as a GP

When you apply for finance for your GP clinic, lenders will need to see from you:

A personal profile which details your background assets and your monthly income/outgoings

3 years of financial accounts for the partnership

3 months personal bank statements

Confirmation of the amount and the percentage that you are buying

An indication of the salary that you will earn as a partner and what share of the notional rent you will receive

This information is needed by lenders to assess firstly, whether you can afford the loan against your present lifestyle/expenditure, and also that the existing business you are buying into or your plan for the business you intend to build is financially sound.

Whether you are already working in private practice or considering setting up your own surgery we can help you find the financing option specific for your individual needs and circumstances. We can help with:

We specialise in sourcing and negotiating the best terms for medical health professionals when they take out a business loan. Our team know exactly how to give your application the best chance of success. We know who to approach for the best rates. We know how to negotiate more favourable terms.

We understand how to raise finance for medical businesses.

If you’re looking to raise finance for a GP practice, Samera can help make sure you get the best possible deal for your business.

“Understanding how GP practices are financed is key to securing the best terms available. This means using a broker that knows the GP market and also the banks requirements is key to funding your GP practice”

We’ve been helping to fund the future of British healthcare businesses for over 20 years and our team are made up of former bankers with decades of experience in the UK’s healthcare lending sector.

You can find out more about working with Samera and the financial services we offer by booking a free consultation with one of the Samera team at a time that suits you (including evenings) or by reading more about our financial services at the links below.

Make sure you never miss any of our articles, webinars, videos or events by following us on Facebook, LinkedIn, YouTube and Instagram.

Reviewed By:

Nigel Crossman

Head of Commercial Finance

Nigel is a former banker and head of commercial finance at Samera. He specialises in raising finance, negotiating deals and structuring finance applications for healthcare businesses.

Chris O’Shea

Head of Marketing

Chris is Head of Marketing at Samera. With his wealth of knowledge in SEO, PPC, user experience and lead generation, he is an expert at helping private dental practices and accountants increase their brand awareness and grow their patient list.

Tax bills are a recurring expense for all businesses including dental practices that can often take their toll. This is where tax loans come in and help manage this overbearing expense by helping you take control of your cash flow. They also help ease the costs of taxes by spreading the costs of your tax bill into manageable monthly payments.

The amount of taxation that a business incurs is based on current tax laws that determines their tax liability. Tax liability is the amount of tax debt owed by an individual, business, corporation or any other entity. Tax liabilities are therefore incurred from earning any income from a business, a gain on the sale of an asset, estate or other taxable events.

When a business’s tax liability is due, as a dental practice, they have to ensure that they have enough cash flow at hand to meet the demand of the tax laws in place. Unfortunately owing tax isn’t an easy debt to get out of. A tax bill cannot be put off until the business itself pays the bill. HMRC do not hesitate in issuing penalties for late or non payments. The tax rules are very strict and failure to adhere to them can become very costly for you and your business.

In some instances, late penalties are one of the more tranquil consequences that the HMRC gives out. Penalties for late payment or non payment can have very bad consequences on your business. If you default on your payments for a very long time, the interest of your tax bill increases and so does your fines. This could lead to you having to liquidate a company in its entirety or its assets in order to fully pay HMRC what is owed through your tax liabilities.

It is normal for a business’s cash flow to fluctuate over the different seasons, however, it is imperative that funds are put aside in order to meet tax obligations. However, this is often not always the case. The cash flow may not always be there and unforeseen circumstances do occur to hinder you from being able to pay your taxes. This is where tax loans come in handy for businesses.

VAT and corporation tax payments come around regularly but they can still be a problem if your business does not have sufficient funds. Tax loans are designed to help manage your cash flow. Tax loans can fund personal tax, corporation, capital gains, inheritance tax amongst other overbearing tax bills you may incur. Tax loans allow you to spread the cost of your tax demand into more affordable monthly payments, allowing you to pay your tax bill comfortably.

When quarterly VAT payments are looming for your dental practice and there is limited cash in the business to secure paying this bill, access to additional finance is very useful.

VAT funding enables businesses to pay your quarterly VAT payments over the course of an agreed term (usually 12 months). This will be paid back over a series of monthly payments. This loan provides the liquid funds needed for businesses to settle their VAT bill without provoking any consequences from HMRC. Obtaining this loan will boost the company’s overall cash flow position as well as pay your VAT bills smoothly.

As a business owner, there are a few things that may be worrisome for you. Owing the government funds can unfortunately often be part of that worry. A lot of business owners are not aware of the options that are available to them when they do not have enough working capital to pay the necessary bills.

Businesses try to optimise their profits and strive to have working capital to reinvest and take advantage of business opportunities. For this reason, tax loans are becoming increasingly popular. These loans allow businesses to free up cash flow while meeting the demands of HMRC on time.

Forfeiting a tax payment or paying late is something you must try to avoid at all costs. Owing a debt to the HMRC is not something to be taken lightly. Often those who default on their tax payments are dealt with enforcement actions being taken against them.

Regardless of what your business is, taking out a tax loan can be the financial solution that you need as it will enable you to spread out the cost of your tax bill over the course of a 6-12 month term helping businesses navigate through the costs of tax while avoiding the wrath of HMRC and racking up late payment charges.

Why are tax loans useful?

Tax loans are incredibly helpful and convenient to help pay your tax bill on time. On the one hand, it is in your best interest to stay within HMRC’s good graces by paying all your tax bills on time while on the other, you also want to leave yourself available cash for the essential day to day running of your business. Tax loans help you do both, very comfortably.

Many lenders design your loan specific to your needs, there are loans that are specifically designed to pay tax bills. In some cases, funding a VAT bill can have tax benefits. This is because interest payments are often offset against corporation tax later in the financial year.

Benefits of tax loans

Improved cash flow as well as control of cash flow

Easy, fixed monthly repayments

Flexible repayment terms

Easy quick and simple to arrange

HMRC receive payments directly and on time

Protects existing bank facilities

Keeps your bank funding lines open

Fixed rates

Fast decisions and fast funding

Personal service and dedicated account manager

Many tax loan facilities operate in ways to enable you to receive the funds you need in a simple and timely manner. The main benefits tax loans have to businesses is that this loan will allow their cash flow to remain in their control, lift the weight of their tax bills by spreading out the costs into manageable monthly payments and avoiding any late payment consequences.

How do I apply for tax bill funding?

As a dental business owner, VAT or tax payments can be detrimental to your business profits. Time constraints are very common, especially when it comes closer to the time to pay your tax bills. This is why the process of applying for funding is quite quick and simple.

Unlike many other loans, detailed business plans and security assets are not needed, nor is it necessary to make long winded appointments to discuss the security of your loan. Many processes are flexible and quick with great affordability and transparency.

Tax refund

Loan against tax refund

Taking out a loan against your tax refund is also known as a refund-advance loan. It is a type of secured loan. This means that you need to put up something in this loan to use as collateral. Usually this would mean an asset or an estate but in this case collateral refers to your anticipated tax refund.

Tax refund loans are short term loans that must be repaid when you receive your tax refund. You will often receive this loan as a deposit into your bank account . When you get your tax refunded, it will be deposited into that same bank account and the loan amount will be deducted from the amount given. Interest and other fees will also be deducted from the amount of tax refund given to you.

Pros and cons of tax refunded loans

Here are a few things to consider before you take out a tax-refund loan.

Pros of tax-refunded loans

Fast funding

When you apply and are approved for a ta-refund loan, the funds are available to you as little as 24 hours after you are approved. Usually the time it takes from your tax to actually be refunded to you is a minimum 21 days.

Cons of tax-refunded loans

Fees

Unfortunately getting a tax refund loan may often involve paying interest on said loan. This is not the case with all tax refund loans, there are some lenders that are able to give you an interest free loan. However, even with an interest free loan, there still may be fees you will need to pay, for example, administrative fees that are associated with transferring your refund.

High risk

There are potential risks with this kind of refund loan. The key risk being that the amount of the loan is based on how much you anticipate getting back in the refund. This may not accurately represent how much your tax refund will actually be. There are several factors that could impact that amount you are expected to receive and the actual amount you are given.

An example of this is that if you owe a state debt such as a student loan or back taxes. These debts will be taken from your tax, therefore, your tax refund will be reduced. This will result in you receiving less funds than you had anticipated when taking out the loan.

Tax refund loans

While tax refund advance loans can be a helpful and timely option to get the quick cash flow you need, there are many factors you must keep in mind before you decide to apply for this type of loan.

If you do decide to apply for a tax-refund advance here are a few things we advise:

Proceed with caution:

These loans can often come with a high interest rate and hidden fees.

Read the terms and conditions carefully:

To allow yourself to make the most out of this loan, you must ensure that you fully understand the terms and conditions of the loan and all the costs in their entirety. This includes any contractually included late fees or any prepaid card costs associated with the loan.

Corporation tax is the one of the most important taxes your business, however large or small, will pay. If you are unable to pay your corporation tax bill, you will be hit with penalty charges which will increase the longer you default on your payment and will exceed the overall amount you originally owed, fundamentally resulting in you being in a worse financial situation.

Charges begin from the day your payment is late, the interest of the lay payment will also continue to rack up over time so it is important to meet your payment deadlines.

If you are unable to pay your tax bill because the time for paying your taxes has come at a very inconvenient time for you, then a corporation tax loan would be ideal for your situation. It is an effective way to spread your tax demands across monthly repayments that are affordable for you.

What is corporation tax?

Corporation tax is a tax that all limited companies must pay. It is a tax that is payable against the profits the company makes. A corporation tax bill is based on the level of income a business has earnt through trading. It is the income derived from taxable events throughout the tax year such as asset sales. You are liable to pay corporation tax if your business is a member’s only club, a trade association, a limited company, a trade or housing association, or a group of individuals outside a partnership operating as a business.

The current rate in the UK for corporation tax is 20%. This also applies to any companies you may have overseas but have an office or branch residing in the UK. HMRC usually calculates your corporation tax bill roughly 9 months after the business accounting year comes to an end.

If your tax liabilities are not paid on time, similar to your business tax expenses, there will be penalties issued by HMRC. If your tax bill is quite high, the business itself could be forced to liquidate completely in order to pay your tax bill. The real truth for many businesses is that they sometimes simply are not in a position to be able to pay their bill which is why corporation tax bills can be very useful. It is important to note that HMRC will not send reminders about your tax bill until you are overdue.

This is a difficult situation to be in, especially if your current available capital does not allow you to meet the demanded amount of the corporation tax bill. Ideally, the best option is to set aside funds during the year to meet your tax bill however, It is normal for cash flow to fluctuate over the year based on different activities. This makes it hard to put a large amount of money aside especially when you have unexpected costs to pay. This is why corporation loans are becoming increasingly popular to help regulate cash flow and pay for a business’s tax bill.

Who pays corporation tax?

All limited companies are liable for corporation tax. The tax is also aligned to the financial year of the business. However, there are a few exceptions such as when a new business changes its year end accounting date.

Businesses are bound to pay taxes on any profits the business makes in its financial year. Corporation tax is also due on any money the business makes from investments and any chargeable gains.

Benefits of a corporation tax loan

Corporation tax loans improve a businesses cash flow which is why they are increasing immensely in popularity amongst many different types of businesses. This added stable cash flow allows businesses to take advantage of this added capital to their business to fund unexpected costs or any drops in income.

A major benefit of a corporation taking a loan is the added cash flow to your business. The loan also helps avoid the risk of high and very costly charges for late or non payment of your taxes. The loan itself will improve the flow of your capital, this means that when your next corporation tax loan is due, you will be in a much better position to comfortably pay the bill.

Regardless of the type of business you operate, it is possible for you to qualify to apply and receive a corporation tax loan. The loans have various options that are flexible for you and they will enable you to spread your tax bill over the course of several months. You will have fixed monthly or quarterly payments to repay your loan.

There are a variety of lenders who specialise in commercial finance loans. They are able to design a plan that is flexible and suited to your specific repayment abilities to ensure that you will be able to pay your tax bill comfortably with monthly installments.

Using corporation tax funding allows businesses to avoid the potentially costly HMRC penalties for late or non payments. You can usually get a decision on your corporation tax loan inquiry within as little as 24 hours in most cases.

Where to apply for a corporation tax loan

There are a number of lenders who specialise in finance loans specific to paying tax such as corporation tax loans, which gives you many options to choose from. There are various online comparison tools that will be perfectly aligned to the needs of your business. These comparison tools and websites will also help you filter through different loans that are best suited to you with the lowest interest rates.

Tax loans for dentists are specialized financial products designed to help dental professionals cover their tax liabilities, such as income tax, VAT, or corporation tax. These loans provide immediate funds to pay tax bills, allowing dentists to spread the repayment over manageable installments. By doing so, tax loans help avoid late payment penalties, improve cash flow, and ensure the smooth operation of the dental practice without the burden of large, lump-sum payments.

How do tax loans help dental practices?

Tax loans help dental practices by providing immediate funds to cover tax obligations, such as income tax, VAT, or corporation tax, without draining cash reserves. By spreading tax payments over several months, these loans improve cash flow and allow practices to manage other essential expenses, like payroll and equipment purchases. Additionally, tax loans prevent late payment penalties, ensuring that taxes are paid on time, and help dentists maintain financial stability, especially during periods of fluctuating revenue.

Can I get a tax loan for my dental practice with bad credit?

Yes, you can still get a tax loan for your dental practice with bad credit, although it may be more challenging. Some lenders specialize in providing loans to businesses or individuals with less-than-perfect credit. However, the terms might include:

Higher interest rates: Due to the increased risk, lenders may charge higher interest rates.

Collateral: You may need to provide collateral, such as equipment or property, to secure the loan.

Shorter repayment terms: Lenders might offer shorter repayment periods to minimize their risk.

Working with a lender experienced in healthcare or dental practice financing can improve your chances of securing a tax loan, even with bad credit.

What types of taxes can tax loans cover for dentists?

Tax loans for dentists can cover various types of tax liabilities, including:

Income Tax: Helps dentists pay personal or business-related income tax on time.

VAT (Value Added Tax): Covers quarterly or annual VAT payments for dental practices.

Corporation Tax: Assists in covering taxes due on company profits for incorporated dental practices.

National Insurance Contributions (NICs): Can help pay required NICs for both employers and employees.

Other Business-Related Taxes: Includes any additional taxes owed related to business operations, such as local taxes or payroll taxes.

These loans allow dentists to spread out tax payments, easing financial pressure and maintaining healthy cash flow.

How quickly can dentists get approved for tax loans?

Dentists can typically get approved for tax loans within 24 to 48 hours, depending on the lender and the completeness of the application. Some factors that can influence approval time include:

Lender Type: Specialized lenders may offer faster approval compared to traditional banks.

Application Completeness: Providing accurate and complete financial documentation, such as tax statements and business accounts, can speed up the process.

Credit Check: While some lenders process credit checks quickly, poor credit may require additional review and extend the approval time.

In most cases, fast approvals ensure that dentists can pay their tax bills on time, avoiding late fees or penalties.

What are the typical interest rates on tax loans for dentists?

The typical interest rates on tax loans for dentists can vary depending on several factors, such as the lender, loan amount, and the borrower’s credit profile. Generally, interest rates range from 4% to 12%.

Factors that influence interest rates include:

Credit Score: Dentists with higher credit scores typically qualify for lower rates, while those with bad credit may face higher rates.

Loan Term: Shorter-term loans may offer lower interest rates, while longer repayment terms may have slightly higher rates.

Secured vs. Unsecured: Secured tax loans, where collateral is provided, often have lower interest rates compared to unsecured loans.

Lender Type: Traditional banks may offer lower rates, while specialized or alternative lenders may charge more for faster approval or more flexible terms.

It’s important to compare lenders and terms to find the best interest rate for your practice.

How long can I take to repay a tax loan for my dental practice?

The repayment term for a tax loan for your dental practice typically ranges from 6 to 12 months, depending on the lender and your financial situation. Some lenders may offer flexible repayment terms based on your needs.

Key factors affecting repayment terms:

Loan Amount: Larger loans may come with slightly longer repayment terms.

Lender Policies: Some lenders might offer extended terms, while others focus on shorter repayment periods.

Your Financial Situation: A strong financial profile could allow you to negotiate more favourable, flexible repayment terms.

Repaying over 6 to 12 months allows you to manage cash flow more effectively, ensuring timely tax payments without a heavy financial burden.

Can I use a tax loan to pay both personal and business taxes as a dentist?

Yes, you can use a tax loan to pay both personal and business taxes as a dentist. Tax loans are versatile and can cover various types of tax obligations, including:

Personal Taxes: Income tax or National Insurance Contributions (NICs) that you owe as an individual.

Business Taxes: Taxes related to your dental practice, such as VAT, corporation tax, or payroll taxes.

This flexibility allows you to manage both personal and business tax liabilities without straining your cash flow, ensuring you meet deadlines and avoid penalties.

Are tax loans for dentists secured or unsecured?

Tax loans for dentists can be either secured or unsecured, depending on the lender and your financial situation:

Secured Tax Loans:

Require collateral, such as dental equipment, property, or other assets.

Typically offer lower interest rates and more favorable terms since the lender’s risk is reduced.

Unsecured Tax Loans:

Do not require collateral, making them easier to access for those without significant assets.

Interest rates may be higher due to the increased risk to the lender.

Dentists can choose between secured and unsecured options based on their credit profile, financial needs, and whether they prefer to pledge collateral.

What is the process for applying for a tax loan for my dental practice?

The process for applying for a tax loan for your dental practice is typically straightforward. Here are the general steps:

Evaluate Your Tax Liability: Determine the amount you need to cover your tax obligations, such as income tax, VAT, or corporation tax.

Research Lenders: Look for lenders that specialize in offering tax loans to dental practices. Compare interest rates, terms, and repayment options.

Gather Financial Documents: Prepare essential documents, including: Tax bills or statements Recent bank statements Business financial records (profit and loss, balance sheet) Personal credit report (if required)

Submit the Application: Fill out the lender’s application form, either online or in-person, providing the necessary documents and information.

Approval Process: The lender will review your application, assess your creditworthiness, and may conduct a credit check. Approval can often happen within 24 to 48 hours.

Receive Funds: Once approved, the funds are typically deposited directly into your account, allowing you to pay your tax liabilities.

Repay the Loan: Follow the agreed-upon repayment schedule, usually spread over 6 to 12 months, to manage cash flow while settling the loan.

This process is designed to be quick, helping you meet tax deadlines and avoid penalties.

Will a tax loan improve cash flow in my dental practice?

Yes, a tax loan can improve cash flow in your dental practice by allowing you to spread out large tax payments over manageable monthly installments. Here’s how it helps:

Avoid Large Lump-Sum Payments: Instead of paying a large tax bill upfront, a tax loan lets you break it into smaller, regular payments, preserving cash for other essential expenses.

Prevent Late Payment Penalties: By ensuring you can pay your tax liabilities on time, you avoid fines and interest charges, which could otherwise strain your finances.

Free Up Capital: With a tax loan, you keep more working capital available for day-to-day operations, such as payroll, supplies, and equipment purchases.

Stabilize Financial Planning: It helps smooth out cash flow fluctuations, especially during periods of lower revenue, by spreading out payments over several months.

In summary, a tax loan offers financial flexibility, allowing you to manage tax obligations while maintaining the cash flow needed to run your practice efficiently.

Can I refinance an existing tax loan for my dental practice?

Yes, you can refinance an existing tax loan for your dental practice. Refinancing allows you to adjust the terms of your current loan, potentially offering several benefits:

Lower Interest Rates: If market rates have dropped or your credit has improved, you may qualify for a lower interest rate, reducing your monthly payments.

Extended Repayment Terms: Refinancing can extend the loan’s repayment period, making monthly payments smaller and easier to manage, which can help improve cash flow.

Better Loan Terms: You may secure more favourable terms, such as flexible payment options or reduced fees, by refinancing with another lender.

Consolidate Debt: If you have multiple loans, refinancing can help consolidate them into one, simplifying payments and possibly lowering your overall interest rate.

Refinancing is an effective way to adjust your financial strategy and better align your loan with your practice’s current needs.

What happens if I miss a payment on my tax loan?

If you miss a payment on your tax loan, several consequences may follow, depending on your lender’s policies. Here’s what can happen:

Late Fees and Penalties: Most lenders will charge late payment fees, which can increase the overall cost of the loan.

Increased Interest: Some lenders may increase the interest rate or add additional charges for missed payments.

Damage to Credit Score: Missing a payment could negatively impact your credit score, making it harder to secure loans or favorable terms in the future.

Loan Default: If multiple payments are missed, the lender could classify the loan as in default, leading to more severe actions, such as legal proceedings or the seizure of collateral (for secured loans).

Negative Impact on Cash Flow: Late fees and penalties can strain your cash flow, further complicating the financial situation for your dental practice.

If you’re at risk of missing a payment, it’s best to contact your lender immediately to discuss potential solutions, such as restructuring the loan or adjusting the payment schedule.

Are there any fees involved in getting a tax loan for dentists?

Yes, there may be several fees involved in getting a tax loan for dentists, depending on the lender. Common fees include:

Arrangement or Origination Fee: A fee charged by the lender to process and set up the loan, typically a percentage of the loan amount.

Late Payment Fees: If you miss a scheduled payment, the lender may charge a penalty fee for late payments.

Early Repayment Fee: Some lenders may charge a fee if you pay off the loan earlier than the agreed term, known as a prepayment or early settlement fee.

Processing or Administration Fees: Fees for handling paperwork and managing the loan account.

Interest Charges: While not a fee in itself, interest is a significant cost associated with the loan, and it may be affected by your creditworthiness or loan term.

It’s essential to review the loan terms carefully and ask the lender about any potential fees before committing.

Is there a maximum amount I can borrow with a tax loan for my dental practice?

The maximum amount you can borrow with a tax loan for your dental practice typically depends on several factors, including:

Your Tax Liability: Lenders often provide tax loans that are directly tied to the amount you owe in taxes, whether for income tax, VAT, or corporation tax.

Your Financial Profile: The lender will consider your dental practice’s revenue, cash flow, and creditworthiness when determining the loan amount.

Lender Policies: Different lenders have varying maximum loan limits, which may range from £10,000 to £500,000 or more, depending on the lender’s criteria and your business size.

To determine the exact amount, consult with a lender specializing in tax loans for healthcare or dental practices, as they can offer tailored solutions based on your specific tax obligations and financial situation.

Business Loans for Healthcare Businesses

We’ve been helping to fund the future of British healthcare businesses for over 20 years and our team are made up of former bankers with decades of experience in the UK’s healthcare lending sector.

You can find out more about working with Samera and the financial services we offer by booking a free consultation with one of the Samera team at a time that suits you (including evenings) or by reading more about our financial services at the links below.

Bridging loans are a short term financing option that are quite different from a standard bank loan. They are often used by property buyers to essentially ‘bridge’ the financial gap between the sale of their current home and the final sale of their next property investment. However, these loans can be very helpful in many ways for businesses to use immediate funds to obtain quick capital for their dental practice, integrate cash flow or make necessary refurbishments. They are one of the most useful and viable options when you need to move quickly to buy a property.

Bridging loans are usually offered between 1-18 months, with the loan repayable in full at the end of the term. An open bridging loan does not have a repayment date, but will still be a short term loan. For example, a 12 month bridging loan must be repaid on the 12th month or before the 12 month period ends. It is in your interest to repay the loan as early as possible in order to save on interest payments.

Bridging loans are very easily accessible and immediate financing which means that they typically have high interest rates and fees.

What is Bridging Finance?

Bridging finance is a kind of commercial property finance which is usually used by companies and sole traders to quickly fund the purchase of a property. Traditional commercial mortgages often take months to arrange. Bridging finance companies can lend money much faster. This type of funding allows clients to obtain immediate funds to complete the purchase of a property or to bridge the gap between selling and buying a new estate. The loan will usually be secured against a charge of the property you are purchasing.

How Much Can I borrow with a Bridging Loan?

The amount that you can borrow is solely dependent on the value and the type of security property that you use. Bridging lenders will quote a maximum loan to value (LTV), this is usually between 65-80%. You are able to get a bigger loan depending on your exit strategy.

Bridging loans are only meant for short term periods, so attempting to get a very large amount of money through a bridging loan without an adequate exit strategy is quite unlikely.

Why is Bridging Finance Useful?

Bridging finance is useful for dental practice businesses because it is a loan option that is fast and flexible. This short term property loan option can be approved and released so quickly that it could be done in a matter of days. In many cases, this is a very valuable asset to obtain in the property industry.

These loans are a highly useful tool for businesses to bridge the gap between two property transactions. Bridging loans are a practical solution for those who need extra time to sustain suitable long term finance.

Bridge capital is temporary funding that helps businesses cover its costs until it can get permanent capital. The repayment terms for bridge capital vary on the individual, but usually payment is made in full when the loan reaches the end of the term. Usually, by this time, the company receives the necessary capital from their investment or a longer term loan. Bridging loans are typically secured on any real estate asset a borrower can offer. This can include commercial or mixed-use properties.

How do I get a Bridging Loan?

Bridging loans are not widely available and are not offered by a lot of high street banks. Bridging loans are usually highly available from mortgage brokers and advisers.

Although bridging loans are generally quicker to arrange than a mortgage, do not make the mistake that they are easier because lenders are less thorough. Lenders still make thorough checks of your current finances, the value or your perspective property and your current home.

How Much do Bridging Loans Cost?

Bridging loans can end up being very expensive because they charge you a range of fees as well as interest. You will be charged monthly interest on your loan. Your lender will not quote the annual percentage rate (APR) as most bridging loans do not even last a whole year.

You will be charged interest on your loan in 1 of 3 ways:

Monthly interest: This is the most common way interest will be added to your loan. You will pay the interest each month, and it will not be added to the balance of your loan. You will pay off the full balance at the end of the term.

Rolled up interest: This is when you pay all of the interest including your original loan, at the end of the term. The interest will be added each month and accumulated this way, however you will just pay the full amount when your term comes to an end.

Retained interest: Your lender will calculate the amount of interest you will have to pay over the time-frame of your term when you first take out your loan. You will borrow the interest amount from the bridging lender when you apply for your loan including your initial figure. This will cover the monthly interest payments for a set period. You will then pay the loan back and the end of the term including the extra money borrowed for interest payments.

Exit Strategies for Bridging Loans

An exit strategy is the term used to explain how the bridging loan will be repaid at the end of the term. A strong exit strategy is a vital part of any bridging loan application. It is having a strong exit strategy that makes the process of the loan application faster and lenders to be more flexible with your requests.

Why is an Exit Strategy Important?

Having a preplanned and strong exit strategy is very important on a bridging finance provider’s checklist. These loans are based on an interest only basis. How you plan to settle the end of your loan at the end of its term is the most crucial part of your loan.

When your term has come to an end, your lender will expect your loan to be paid back in full as agreed. In the case that you are unable to do this, your account will then be put into default. If this happens it could affect your credit record. In order to avoid this situation you will need to resolve the situation as quickly as possible.

Here are a few options for you:

Extend your loan with your lender. This may mean that you will continue to add interest on your current loan if you are near your maximum loan to value. It is also important to note that your lender may not agree to renew the loan. If they do agree, they may charge a higher interest rate in exchange for the renewal.

Refinance to a new lender. This option could get very expensive for you as you will have to restart the process and pay all setup costs again.

Remember that if you do refinance your loan, you still need to consider what your exit plan is for your new loan. Refinancing blindly is a temporary solution, you will just be delaying the inevitable unless you plan a way to properly pay back the loan.

What if I can’t Pay Back the Loan by the End of the Agreed Term?

Bridge loans in their nature are arranged for short term requirements and the lender expects all clients to contractually abide by the terms of repayment within the set time frame agreed.

Bridge loans, like many other loans, are set up with a set plan to arrange how the loan will be repaid. Usually, the lender will not allow the loan to proceed if there are any hesitations about your ability to repay the loan.

When you hit the end of your term, you are expected to repay the loan in full. Acceptable exit methods are usually sale of property or refinance. There are a range of different exit strategies that may work for you.

Loans are a contractual agreement, however, it is inevitable that some loans will overrun the agreed term. The lender will often contact you (the borrower) at least 3 months prior to the end of the agreed term to examine how things are going for you and determine whether you will be able to pay back the loan in time of the agreed term. If the lender believes that it is not likely, they will usually recommend other steps that you can take to ensure that you can get back on track and eventually, you will be able to fully repay your loan.

The lender will obviously want the loan repaid as and when agreed but they will normally work with borrowers who have over run their term only if the borrower is open about their situation and is in continuous regular contact with the lender. This way you and your lender are able to work out a plan to get you back on track together.

We always recommend that when taking out a bridging loan, you opt for the longest term available as many plans can over run the expected timeframe.

How Long Can I Take Out a Bridging Loan for?

The average term for a bridging loan is approximately 6-7 months. In different circumstances, longer terms can be discussed and arranged. It is often dependent on how much your loan is for that your term can be extended.

Are Bridging Loans Regulated?

A bridging loan becomes ‘regulated’ when the loan is secured against a property that is or will be occupied by the borrower. A regulated loan can be secured by a first or second charge, the bridging loan will be regulated by the FCA.

Bridging loans that are unregulated are usually associated with commercial buy-to-let properties.

Can I Get a Bridging Loan Without a Credit Check?

No. Like most other loans, bridging finance involves a thorough check into the finances of the borrower.

Applicants with clean credit history are often more attractive to lenders which results in these applicants receiving favourable rates. However, good credit is not only what lenders look for. There are other aspects and details of your loan that will help you get approved by your lender even though you may have a bad credit history.

Can I Still Get a Bridging Loan if I Have Credit Issues?

Although thorough checks into your credit history will be taken before you take out your loan, bridging loans can still be available to you even if you have a poor credit rating. Your bridging finance is often determined by the security of the property being offered as well as the exit route. Your lender will also take into account the size of your deposit and the assets you put up as security.

A lender’s biggest concern is that having poor credit history will prevent you from repaying the loan at the end of the term. It is highly dependent on what you put up as security and what your exit strategy is. If you have a strong exit strategy such as, to sell the property or another estate, then there is a lesser chance to have an impact on you taking out the loan.

Closed-Bridge and Open-Bridge Loans

What is a closed bridging loan?