Asset Finance for Dentists – Webinars and Podcasts

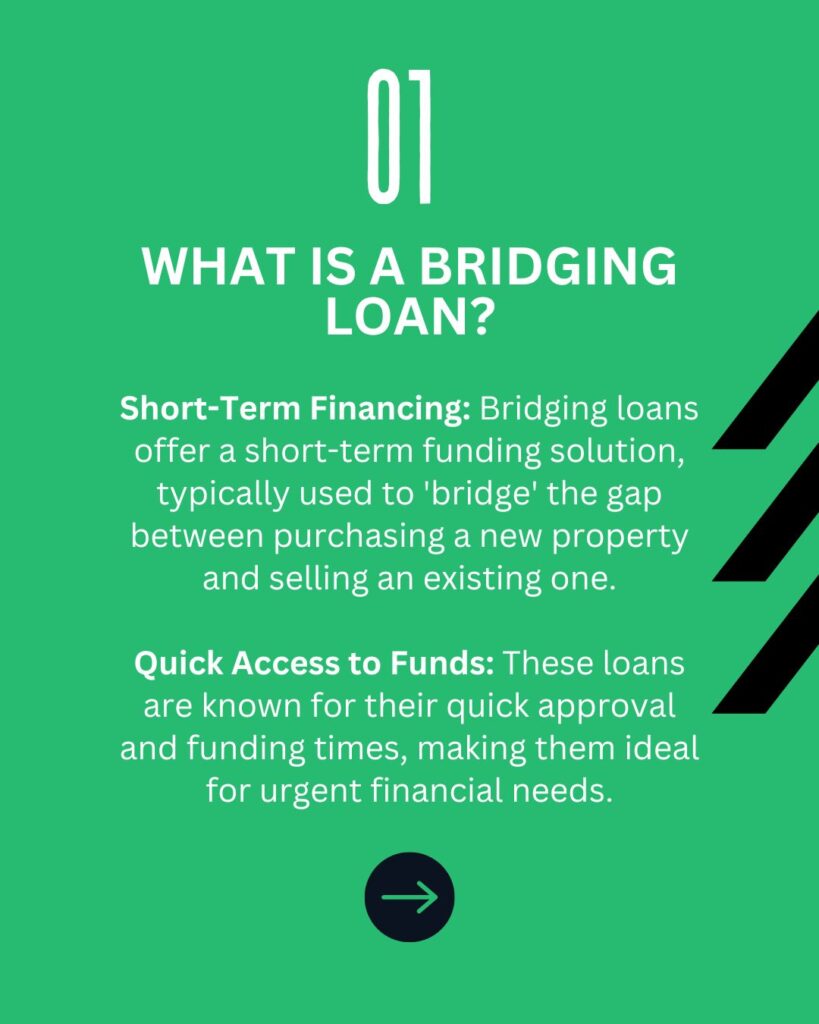

What is Asset Finance?

Asset finance is the funding raised by a company to either purchase or hire assets. Dental practices all require some kind of asset in order to operate. Whether this be general office equipment, specialised machinery or even furniture.

In many cases, companies do not have the up front cash required to purchase these assets, especially since most of the necessary equipment can be quite expensive. This is especially true of start-up businesses that have not had time to build up reserves of capital.

It is also true of more established businesses that are experiencing cash flow issues, or maybe wish to purchase extremely expensive equipment.

Fund the Purchase with Asset Finance

In these circumstances, many dental businesses will approach commercial finance providers to attempt to source asset finance to fund the purchase. Asset financing can work in a number of ways and the terms of the loan will vary depending on the provider.

For instance, the asset finance provider may provide you the money to buy the asset outright. On the other hand, they may prefer to buy the asset themselves and then loan the asset to your company.

At the end of the loan term the asset could become property of the borrowing company. On the other hand, the asset finance company may wish to keep the assert themselves once the loan term is completed.

Asset Finance vs Asset-based Finance.

Asset finance is similar to, but not to be confused with, asset-based finance. Asset finance is the money raised by a business to purchase or hire equipment for the company. However, asset-based finance refers to the security put up against a loan as a guarantee.

Asset-based lending is often used by companies which need short-term lending to alleviate problems in cash flow, such as payroll issues, and to keep the business running on a day-to-day basis.

Secure a loan using an asset

Asset-based finance is a method commercial finance lenders use to guarantee their investments. Asset-based finance is, in essence, a process whereby a lender will secure their loan using one of the company’s assets.

Lenders will usually use assets such as specialised equipment or machinery, company vehicles, any property the company may own and even accounts receivable.

These assets are used to guarantee the loan repayment. In other words, if the borrowing company is unable to pay back the loan in full or on time, the asset-based finance lender will seize the asset (or assets) and sell them in order to recuperate their loss.

Asset and Asset-based Finance Together

Asset finance and Asset-based finance can also be used in tandem. If you are a start-up dental practice with minimal working capital, or perhaps an established practice struggling with liquid capital or cash flow problems, you can use asset-based finance to purchase equipment.

In these cases, businesses use the asset itself which they are borrowing to buy as the collateral. For instance, you may be a dentist opening your first dental practice and you need to purchase expensive x-ray machines.

What do you do if you don’t have tens of thousands of pounds lying around to buy it?

You would use asset-based finance to raise the money you need to purchase the machine. However, the lender is also using that x-ray itself as the collateral asset. This means that if you are unable to pay back the loan, the lender will seize that x-ray and sell it on to recoup the loan.

Contact us to find out more

What is an asset?

To understand asset finance it is important to understand what an asset is. An asset is essentially any piece of property owned by a business, not including land or a building.

The assets a business owns will vary from company to company and industry to industry.

Most businesses will need general office supplies such as desks, chairs, IT equipment and even smaller items like stationary. A dental surgery will have dentist chairs, special lighting and a lot of specialist equipment. These are considered business assets and can be purchased using asset finance or asset-based finance.

Company vehicles can also be purchased using asset finance. These vehicles could be large lorries and trucks used to haul heavy goods or equipment around the country. They could also be small private cars intended solely for business related travel.

Industry-specific companies will also need to purchase specialised machinery and equipment for their day-to-day operations and these are often incredibly expensive.

For instance, a dentist’s private practice will need surgical chairs, the medical equipment and general office supplies.

However, there will be incredibly expensive, specialised machinery such as x-ray machines, scanners and digital imagery equipment, machinery for manufacturing dentures, implants and retainers and much more!

Durable, Identifiable, Moveable and Saleable

That is not to say that lenders will fund any product you tell them you wish to purchase. Generally speaking, to be eligible for asset finance, an asset must meet criteria known as the DIMS criteria.

DIMS stands for – Durable, Identifiable, Moveable and Saleable. These criteria are used by asset finance lenders to determine whether the asset being purchased is suitable for asset financing and, thus, a safe investment for their money.

Assets eligible for financing are often split into 2 categories. Hard and soft assets.

Hard Assets

Hard Assets are those assets which are durable and have a good resale value at the end of their term with your business. Hard assets are most often used as security against asset-based finance due to their high resale value.

In other words, if you fail to pay the debt, hard assets will be able to pay it off instead. Hard assets include items such as heavy machinery and vehicles.

Soft Assets

Soft assets are those assets which have a greatly reduced resale value at the end of their lease term. Due to this fact, soft assets may require additional security on the part of the borrowing party to lower the risk of the borrower, and thus secure the loan.

Soft assets include things such as IT software and medical equipment which cannot be reused.

Very few businesses, especially newer start-ups, will be able to raise the funds themselves necessary to purchase this much equipment. Established dental practices will a healthy client base will find it easier to fund new equipment with their cash reserves.

However, expensive equipment can eat up entire emergency cash reserves and it may be advisable to borrow the money instead to protect the day-to-day running of the business.

Vehicle Finance

Vehicles are a very common asset purchased through asset financing. Vehicles are expensive but necessary aspects to many businesses. However, it can be difficult to raise enough money to buy one, let alone an entire fleet.

Most vehicle dealerships will offer their own payment structures and schedules. However, it may be more economical to purchase the vehicle outright using an asset financing company and paying them instead.

This is because asset financing companies are usually more flexible on the kind of loan terms they can offer.

Asset finance can make a lot of sense when purchasing vehicles for several reasons. Firstly, businesses have the option to purchase expensive assets without having to raise the full amount first.

Additionally, since many asset finance terms mean that the finance company retains ownership of the vehicle, companies are protected from maintenance fees and depreciation.

Why use Asset Finance?

Asset financing is used by all kinds of businesses but is especially helpful for dental practices as it helps aid the purchase of necessary equipment for their operations. Limited companies, social enterprises, charities and sole traders are all eligible to apply for and secure asset finance.

Historically, asset financing was mostly used by larger companies. However, in recent years the threshold for the amount that can be applied for has lowered.

Borrow money to buy an asset

There are a multitude of reasons why a company or sole trader may use asset finance to grow their business. The simplest reason for most businesses is that they cannot afford to buy the asset outright.

The more expensive assets such as specialised heavy machinery, cutting-edge technology and vehicles can be almost impossible to purchase in one lump sum for many businesses.

This is especially true of newer start-ups and small to medium enterprises (SMEs). Without the large reserves of capital that the more established businesses have, it can be extremely difficult to fund the early purchases of necessary equipment.

Spread payments over a number of months

In these situations, it might make more sense to apply for asset financing. This spreads the cost of the asset over a more manageable term.

Instead of paying out a large lump sum, asset financing allows you to spread the payments out over several months. This allows you to better plan and budget your company’s cash flow.

Save capital for an emergency

Even if your company, or you as a sole trader, have the cash available to purchase an asset, you may still wish to apply for it via financing. One of the reasons for this is, simply, that you may need that money for other things.

The asset in question may be essential to your business however, purchasing it immediately with your only available cash reserve is not essential.

Why give up your rainy day fund or disrupt your company’s cash flow when you can apply for asset financing and spread the cost?

What happens if you purchase a new company car with your reserve of capital and the next day your first company car breaks down.

Now you’re back to only having one car. Only this time you don’t have that rainy day fund to get it repaired.

However, if you had purchased or hired the new car on asset financing, you’d still have the ready cash to take the broken car to the garage!

Contact us to find out more

Advantages of Asset Financing.

There are several advantages to using asset finance to purchase or loan equipment, as opposed to using your own capital.

Reduce upfront costs

Using asset finance reduces the upfront costs incurred by your business by spreading the payments for the asset over a period of months.

This helps to keep your business’s cash flow stable by splitting the cost into smaller lumps, instead of incurring one large payment.

Plan your financial year

Since these payments are then fixed, it makes it easier for you to budget and plan your year financially. Spreading the cost also frees up your business’s capital to be used in other areas of growing the business.

If you’re purchasing a high-value hard asset, you can also benefit from using the asset itself as security for the loan.

Secured loans

As we mentioned earlier, you do not need to put up additional security for the loan in many instances. This is especially true of expensive, hard assets.

Instead of putting up extra collateral for the asset, you simply hand the asset over to the lender in the eventuality that you cannot make the payments.

You don’t pay for maintenance

Another great advantage of using asset financing is that any servicing, maintenance or repair costs that need to be undertaken during the life of the asset are incurred by the provider.

This protects your business from sudden, unforeseen costs when things break down or go wrong.

Using asset-based finance can also allow your business to secure better loan terms than they otherwise would.

Secure better terms than traditional lending

Using your company’s assets to secure a loan with an asset finance provider can help you secure far better terms (for instance, in terms of interest rates or payment structure) for a loan that you would from a high street lender such as a bank.

Don’t pay for depreciation

Most assets suffer some level of depreciation during their lifetime – in other words, a reduction in their value. This is true for everything from machinery to vehicles.

Since most companies and individuals will not pay full price for an item that is second hand, you will not be able to recuperate the full value of an asset.

A common saying is that a car loses around 10%-20% of its value the second you drive it off the lot. In many cases, the asset purchased via asset financing is in fact owned by the commercial finance lender.

The lender purchases the asset and then leases it to the business. Therefore, the loss in value is in fact incurred by the lender, not your business. As the actual owner of the asset, they actually suffer the loss in value.

Disadvantages of Asset Financing

Despite its advantages, there are some drawbacks to using asset finance that must be highlighted.

If you cant pay, they’ll take it away

Firstly, the most obvious drawback is that you will lose the asset should you be unable to make your payments, which if happens, will be an obvious hinderance to your day to day dental practices.

Whether you have purchased the asset and have simply borrowed the money to do so, or your lender has purchased the asset and you are leasing it from them, you do stand to lose the asset in the eventuality that you cannot meet the loan terms.

You may not own the asset

Similarly, since many asset finance structures mean you do not actually own the asset, you do not always have full control over its usage. This can mean that modifications may need to be approved by the lender.

This also means that if you need to raise some quick cash for your business, you will not be able to sell the asset on.

Therefore, the asset does not provide quite as much financial security than it otherwise would have if you had bought it yourself.

It’s not a short-term fix

On top of this, asset financing is primarily used as a long-term solution for cash flow issues when it comes to purchasing assets. Short-term asset financing is incredibly rare.

Most agreements are termed for at least 1 year. If your business is looking for short-term financial assistance then asset finance would not be a workable option in most circumstances.

Lastly, although any servicing or maintenance work that is covered by the agreement will be funded by the lender, not all such repair work will be covered.

If your asset is damaged in a way that is not covered in your agreement, your business will incur the costs of any work that needs to be done.

You may need to buy additional insurance on top of your loan payments to protect against this.

Contact us to find out more

Different types of Asset Finance

Generally speaking, asset finance is split into 3 categories; Hire Purchase, Finance Lease and Operating Lease. However, there are several other types of asset finance alongside these.

Hire Purchase

Hire Purchasing in asset finance is an agreement whereby the borrowing company pays for the asset in instalments over time and retains the option to purchase the asset at the end of the term.

In other words, you hire the asset until the end of the loan term when you then purchase it.

During the loan term period, the asset finance company will have ownership of the asset. Until the loan has been fully paid off, your company will only be hiring the asset.

Terms can usually last between 1 and 5 years and it is common for a 10% deposit and the full VAT to be paid upfront. Once the loan has been paid off, your company will have the option to purchase the asset outright.

Under some hire purchase agreements you can show the asset on your balance sheet at the beginning of the loan term.

There are several benefits to using Hire Purchasing for asset finance. Firstly, it allows your business to purchase necessary equipment and supplies without the need to pay huge amounts upfront.

Since you are spreading the cost of the asset over a 1 – 5 year loan term, you can avoid unnecessary disruptions to your company’s cash flow.

You can also often benefit from fairly low (10% is quite common) deposit payments. Additionally, the loan is secured against the asset itself. You will very rarely require any added form of collateral to guarantee the loan.

Finance Lease

A finance lease agreement is a type of asset financing whereby the asset finance provider purchases the asset outright and then leases it to the borrowing company.

This differs from hire purchasing in that the borrowing company never gains full ownership of the asset, they only ever rent it. Once the asset is returned to the asset finance company, it is either sold off or leased off again.

Finance lease agreements usually last from 1 to 5 years. During this time, the borrowing company will have full control and responsibility for the asset.

Unlike hire purchasing, where the asset provider is liable for maintenance and servicing, the borrowing company is liable under a finance lease agreement.

In other words, the borrowing company takes on all of the risks of owning the asset, alongside all of the rewards i.e. usage.

Finance leases usually cover the usable life of the asset. At the end of the loan term, there are generally 3 options.

- Return the asset to the asset finance company.

- The borrowing company enters into a second lease arrangement

- The asset is sold off and proceeds split between both parties.

Operating Lease

An operating lease is a business contract hire which allows companies to lease an asset for just part of its usable life.

Whereas finance leases last for the economic lifespan of the asset, operating leases only last for a fraction. This means that there is much greater resale value at the end of the lease period.

Since they are shorter term leases, operating leases allow businesses to loan assets for shorter periods of time. This makes them good options for companies who need to regularly upgrade equipment or who only need quick usage from an asset.

The shorter loan term also means that the borrowing company takes on none of the ownership risks associated with the asset. All servicing and maintenance costs and responsibility rests with the asset finance provider.

Another advantage is that since the asset appears as a rental on the business balance sheet, it can be offset against company profits.

At the end of the rental agreement, the asset provider will take back ownership of the asset. This can either then be re-hired in a second loan agreement or loaned out to a new company.

Contact us to find out more

Asset-based Refinancing

Refinancing is a process businesses can use to raise capital against their assets, using them as security. Businesses can sell their assets to a refinancing company for a lump sum.

The refinancing company then loans the asset back to the original owners. The business then pays back the lump sum (plus interest) by effectively renting the asset back from the refinancers.

Refinancing is used by businesses who are rich in assets that need to raise quick liquid capital. By refinicaning against their assets, they can raise money without losing the use of their equipment.

Most assets with a high value can be used as security to refinance. Since the loan terms depend purely on the value of the asset, the company’s financial situation and credit history will rarely affect the loan terms.

Balloon Finance

A Balloon Loan is one that allows the borrowing company to pay back a large lump sum as part of their payment schedule, usually towards the end of the loan term.

Smaller monthly payments are made, as per a regular loan agreement. However, Balloon Loans include a much larger amount at the close of the term.

Balloon Loans allow companies to keep their initial deposit and monthly payments lower than they otherwise would be. By paying off the majority (or at least a large portion) of the loan towards the end, you can keep initial costs down.

This makes balloon financing a great option for businesses that have limited capital initially, but are confident of raising enough to pay a larger amount at a later date.

Balloon Financing is a great way for start-ups and early-stage businesses to purchase the assets they need to grow their business.

Click here to read our blog on how to finance a healthcare business

Annual Investment Allowance

The Annual Investment Allowance scheme allows businesses to claim back tax relief against assets they have purchased. If the assets qualify for the scheme, you can claim back 100% of the value of the asset in tax relief.

It is important to note that you may need to pay tax if you then sell the asset after claiming Annual Investment Allowance.

You can claim Annual Investment Allowance on most assets purchased, such as heavy machinery.

However, some assets cannot be claimed. You cannot claim AIA on company cars and other vehicles, assets gifted to the business or items purchased before or for reasons other than usage in the business.

The Annual Investment Allowance amount can change from year to year so it is advisable to contact your accountant or check the UK Government website here.

Annual Investment Allowance can only be claimed during the period in which you purchased the asset.

If the asset has been purchased in a hire purchase agreement, you can claim for as yet unmade payments before you actually start using the item. It is important to note that you cannot claim on interest payments.

Join the Samera Alliance Buying Group

The Samera Alliance is our growing network of dentists, practices and leading industry suppliers, designed to help you save money, grow your profits and build a better dental business.

Join today for free to be a part of our dental buying group, which gives you access to exclusive discounts and offers on the consumables, equipment and products you need to run a successful dental business.

You’ll also get better rates and terms for a wide range of services like HR, IT, utilities, insurance, legal services and much more!

Business Loans for Healthcare Businesses

We’ve been helping to fund the future of British healthcare businesses for over 20 years and our team are made up of former bankers with decades of experience in the UK’s healthcare lending sector.

You can find out more about working with Samera and the financial services we offer by booking a free consultation with one of the Samera team at a time that suits you (including evenings) or by reading more about our financial services at the links below.

For more information on raising finance for your healthcare business, including more articles, videos and webinars check out our Learning Centre here, full of articles and webinars like our How to Guide on Financing a Dental Practice.

Make sure you never miss any of our articles, webinars, videos or events by following us on Facebook, LinkedIn, YouTube and Instagram.

Reviewed By:

Nigel Crossman

Head of Commercial Finance

Nigel is a former banker and head of commercial finance at Samera. He specialises in raising finance, negotiating deals and structuring finance applications for healthcare businesses.

Dan Fearon

Finance Manager

Dan is a former banker and the head of our dental practice sales team. He specialises in asset finance for healthcare businesses and dental practice sales.