Running a dental practice is demanding. Between patient care, appointments, and managing staff, payroll can easily become an overwhelming task. With intricate regulations, constantly shifting tax laws, and the delicate balance between employee contentment and business profitability, it’s understandable that many dental practices find themselves grappling to meet their payroll responsibilities.

From deciphering the nuances of NHS pensions to following Auto Enrolment regulations, managing payroll can feel like walking a minefield. Payroll is more than simply writing out pay cheques and distributing them to your team. Payroll involves intricate regulations, employee classification, and meticulous record-keeping. Failing to navigate payroll correctly can result in costly errors, discontent among staff, and potential legal ramifications.

In this guide, we’ll break down everything you need to know about payroll so you can run your practice smoothly.

Understanding the Importance of Accurate Payroll

Managing payroll accurately is crucial for the success of any dental practice. It’s not just a matter of paying your employees on time, it’s also about fulfilling your legal responsibilities as an employer.

In the UK, HMRC scrutinises payroll accuracy closely, with even minor errors carrying the risk of substantial penalties and fines. Furthermore, errors in payroll can lead to disgruntled employees, denting morale, and productivity within your practice.

Imagine your diligent dental nurses or hygienists receiving incorrect pay slips or, worse yet, experiencing delays in payment. The repercussions can be extensive, impacting both employee contentment and your standing as a dependable employer.

Moreover, maintaining precise payroll is imperative for upholding compliance with UK employment laws, including Auto Enrolment, National Minimum Wage, and Statutory Payments.

Non-compliance with these regulations can result in severe financial penalties, legal repercussions, and tarnishing of your professional image. By ensuring accurate payroll management, you can sidestep these potential pitfalls and ensure your practice operates smoothly and legally. In doing so, you’ll be able to concentrate on your primary objectives – delivering exceptional patient care and advancing the growth of your practice.

Action Points:

Conduct a Payroll Audit: Regularly review your payroll processes to ensure accuracy, identify errors, and make improvements. This helps maintain compliance and avoid penalties.

Understand and Update Legal Knowledge: Stay informed about updates to UK employment laws affecting payroll, such as Auto Enrolment and National Minimum Wage. This knowledge is crucial for maintaining legal compliance. Full information can be found on the HMRC and Gov.uk websites.

Implement Regular Payroll Reviews: Schedule regular reviews of your payroll system to adapt to legal changes and enhance accuracy. This proactive approach prevents discrepancies and ensures employee satisfaction.

Understanding Payroll Basics

Understanding the basics of payroll is important for making sure your staff get paid correctly and on time. Firstly, you need to know the difference between gross pay, which is how much someone earns before deductions, and net pay, which is what they take home after deductions like tax and National Insurance.

It’s also important to understand common deductions, like money for pensions or paying off student loans, as well as any allowances they might be entitled to. You also need to think about how often you want to pay your staff, whether it’s every month or every two weeks, and what works best for your practice and your employees.

Action Points:

Identify Common Deductions: Recognize common payroll deductions like pension contributions, student loan repayments, and others.

Understand Allowances: Be aware of potential employee allowances that can affect pay.

Determine Pay Frequency: Decide on a pay schedule (monthly, bi-weekly) that suits both your practice and your staff.

The Role of HMRC in Dental Practice Payroll

As a dentist, understanding the role of HMRC (Her Majesty’s Revenue and Customs) within your dental practice’s payroll operations is essential.

HMRC is responsible for the collection of taxes, including National Insurance contributions, income tax, and student loan repayments, deducted from employees’ wages. As the authority on the UK’s tax system, HMRC ensures that employers comply with the payroll regulations.

In dental practice payroll, HMRC provides essential guidance on payroll taxes, specifying the rates and thresholds for income tax, National Insurance, and student loan repayments. They also issue instructions on how to calculate and deduct these taxes from employee earnings and are responsible for collecting these payments. It is essential you understand these rules and regulations.

As a dental practice owner, it’s crucial you fulfil your HMRC obligations. This includes business registration, submission of tax returns, and punctual payments. Failing to comply with HMRC regulations can attract penalties, fines, and potential legal repercussions. By grasping HMRC’s role within your dental practice’s payroll ecosystem, you can avoid common pitfalls and ensure the smooth operation of your practice.

Action Points:

Register with HMRC: If you haven’t already, ensure your dental practice is registered with HMRC. This is crucial for legal compliance and to enable you to start processing payroll.

Stay Informed: Keep updated on the latest changes in tax rates, thresholds, and regulations from HMRC to ensure your payroll system remains compliant.

Ensure Compliance: Strictly follow HMRC guidelines for calculating and deducting taxes from employees’ wages. This includes income tax, National Insurance, and student loan repayments.

Timely Submissions and Payments: Set up a reliable system to submit accurate tax returns and make payments by the due dates to avoid penalties and ensure the smooth financial operation of your practice.

What are the Different Types of Employees in a Dental Practice?

In running a dental practice, it’s important to know the different employment types of people who work there. There are dental nurses, hygienists, associates, and receptionists, and each plays a big role in how well the practice runs. But what might surprise you is that each of these roles has its own rules and details when it comes to paying them.

In a dental practice, you might have different kinds of work arrangements. Some people work full-time, some part-time, some are hired on contracts, and others work as freelancers. Some might have hours that change, or they might only get paid based on how much work they do. It’s important to understand all these different types of employees so that you can follow the rules about paying them correctly. This includes things like figuring out taxes, making National Insurance contributions, and enrolling them in a pension scheme.

For example, do you know the difference between an employee and a worker? Or how to tell if someone is a self-employed contractor or a freelancer? Understanding these things can help you avoid making expensive mistakes and make sure you’re following the laws about employing people.

Action Points:

Identify Staff Roles & Regulations: Be aware of the different dental practice staff roles (nurses, hygienists, associates, receptionists) and their specific pay regulations.

Understand Employment Types: Recognize the various work arrangements (full-time, part-time, contract, freelance) and their impact on pay and benefits.

Classify Employees Correctly: Differentiate between employees, workers, self-employed contractors, and freelancers to ensure proper classification for tax and benefit purposes.

Comply with Employment Laws: Familiarize yourself with regulations regarding taxes, National Insurance contributions, and pension schemes for different employee types.

Avoid Costly Errors: By understanding these classifications, you can avoid mistakes in payroll and ensure compliance with employment laws.

Calculating employee salaries and wages

Deciding how much to pay your employees is an important part of managing payroll for dental practice owners. You must be really careful to get it right, so that you don’t make any mistakes that could upset your employees or get you into trouble with HMRC. When you work out how much to pay someone, there are lots of things to think about, like their basic pay, how much tax and National Insurance to take off, and any other deductions they might have, like student loan repayments or pension contributions.

To make sure you get it all right, you need to know all about the different tax rules and allowances that apply to the people who work for your dental practice. For example, you need to understand things like tax-free allowances for things like mileage or pension contributions, and make sure you use the right tax codes for each person.

You also need to keep up with any changes to tax rates or allowances, as well as any updates to the National Minimum Wage or National Living Wage. By carefully working out how much to pay your employees, you can make sure your dental practice follows all the tax laws and rules in the UK and keeps everyone happy and working well together.

Action Points:

Research Tax & National Insurance: Thoroughly understand tax rules and National Insurance contributions for your dental practice employees.

Factor in Allowances & Deductions: Consider tax-free allowances (mileage, pension contributions) and deductions (student loans) when calculating pay.

Utilize Correct Tax Codes: Ensure you assign the appropriate tax code to each employee.

Stay Updated on Regulations: Monitor changes in tax rates, allowances, National Minimum Wage, and National Living Wage.

National Insurance Contributions (NICs) for Dental Practice Employees

Being a dentist involves more than just looking after people’s teeth. You also have to deal with paying your staff and sorting out taxes. One important part of this is National Insurance Contributions (NICs), which can be really confusing for dental practice owners. NICs are a big part of what your employees get paid, and if you get them wrong, you could end up with fines and a bad reputation. By understanding how NICs work, you can make sure you pay the right amount, avoid mistakes, and keep your staff happy and motivated.

Action Points:

Understand National Insurance Contributions (NICs): Gain a thorough understanding of how NICs work for dental practice employees.

Prioritize Accurate NIC Payments: Ensure you pay the correct amount of NICs to avoid penalties.

One important thing to remember when managing employees is setting up pension schemes through auto-enrolment. It’s important to get this right, not just to avoid fines but also to show your staff that you appreciate them and want to support their future.

Auto-enrolment is part of a government plan to encourage people to save for when they retire. As an employer, you have to provide a pension scheme for eligible staff. This means automatically signing up those who qualify for the scheme and making contributions to their pension pot. But don’t worry, it’s not as complicated as it sounds at first.

If you understand the basics of auto-enrollment, pension schemes, and your responsibilities as an employer, you can handle this part of managing payroll confidently, focusing on what you do best – giving great care to your patients.

Action Points:

Implement Auto-Enrolment Pension Scheme: Establish a pension scheme for eligible dental practice staff.

Auto-Enrol Qualifying Employees: Automatically sign-up staff who meet the eligibility criteria.

Contribute to Employee Pension Pots: Make contributions towards employee retirement savings.

Understand Auto-Enrollment Basics: Gain a basic understanding of auto-enrollment, pension schemes, and employer responsibilities.

How to Handle Paye and Tax Deductions

Understanding how PAYE and tax deductions work is important when managing payroll, and it can be tricky, even for experienced dental practice owners. Your main job is taking care of your patients, not dealing with complicated tax rules and laws. But mistakes in this area can lead to fines, penalties, and a lot of stress. So, how can you make sure you’re getting PAYE and tax deductions right?

Firstly, it’s important to know that as an employer, you have to take Income Tax and National Insurance Contributions (NICs) from your employees’ wages using the PAYE system. This means working out how much tax to take off each person’s pay, based on their tax code and personal situation. It might seem simple, but it gets more complicated when tax rates, allowances, and reliefs change.

You also need to think about other deductions, like student loan repayments, pension contributions, and any court orders. And with Real Time Information (RTI), you have to report your payroll details to HMRC as it happens, so accuracy is really important.

Action Points:

Grasp PAYE System: Understand the PAYE system for deducting Income Tax and National Insurance from employee wages.

Calculate Accurate Tax Withholdings: Utilize tax codes and personal information to determine proper tax deductions.

Stay Updated on Tax Changes: Monitor updates to tax rates, allowances, and reliefs.

Consider All Deductions: Factor in student loans, pension contributions, and court orders when calculating deductions.

Maintain Accurate & Timely RTI Reporting: Ensure precise and real-time payroll information is reported to HMRC.

Managing Employee Benefits and Expenses

Making sure that your employees get the right benefits and expenses is an important part of managing payroll, but it often gets overlooked. It’s important to offer good benefits to attract and keep the best people working for you, while also keeping an eye on costs to make sure your practice stays profitable. This includes things like pensions, life insurance, and extra perks for employees, such as gym memberships or help with childcare.

When it comes to expenses, you need to think about all the costs involved in running a dental practice, like buying equipment, getting supplies, and covering travel expenses. You also need to follow the rules from HMRC and make sure your employees are reimbursed correctly for any work-related costs they have.

To manage benefits and expenses well, you need to understand the rules about payroll and have a good system in place to keep track of everything accurately. If you do this properly, you can create a happy and rewarding workplace for your employees while also keeping your practice financially healthy.

Action Points:

Offer Competitive Benefits Packages: Provide attractive benefits (pensions, life insurance) to recruit and retain top talent.

Balance Costs & Benefits: Maintain a balance between offering desirable benefits and keeping practice finances healthy.

Track Expenses Accurately: Implement a system to meticulously record all practice expenses (equipment, supplies, travel).

Comply with Reimbursement Rules: Ensure employees are reimbursed correctly for work-related expenses according to HMRC guidelines.

Outsourcing Payroll vs. In-House Management

When it comes to managing your dental practice’s payroll, you have to decide whether to do it yourself or hire someone else to do it. Each option has its good points and bad points, so you need to think carefully about what’s best for you.

Managing payroll yourself might seem like the cheaper and more controllable option at first. But it can take up a lot of your time and resources. You’ll need to buy payroll software, make sure your team knows how to use it and keep up with all the rules, and spend time doing the payroll each month. You’ll also have to deal with any questions or mistakes that come up. And because the rules about payroll are always changing, it can be hard to keep up and make sure you’re doing everything right.

On the other hand, hiring a specialist payroll provider can take a lot of the pressure off you. These experts know exactly what they’re doing and have all the right tools to get the job done accurately and on time. They’ll make sure you follow all the rules and that your employees get paid correctly. They can also give you advice on tricky payroll issues, like setting up pensions or dealing with student loan payments. By outsourcing your payroll, you can free up your time to focus on what you do best – looking after your patients and growing your dental practice.

Action Points:

Evaluate Payroll Management Options: Consider both in-house and outsourced payroll management.

Assess In-House Payroll Challenges: Be aware of the time commitment, software costs, training needs, and regulatory updates associated with managing payroll internally.

Recognize Benefits of Outsourcing Payroll: Understand the advantages of using a payroll provider, including expertise, accuracy, time savings, and access to expert advice.

The Importance of Payroll Record-Keeping and Compliance

As a dentist, you know how important it is to keep careful records in your practice. From notes on patients to plans for treatments, every little detail matters. The same goes for keeping records of your payroll and following the rules.

It’s important to keep accurate and detailed records to make sure you’re following the law as an employer and that your staff get paid correctly. HMRC says that employers have to keep good records of how much their employees earn, what tax is taken off, and any national insurance contributions. If you don’t follow these rules, you could end up with fines or legal problems. Plus, if your record-keeping isn’t up to scratch, you might make mistakes when paying your staff, which could affect your practice’s money and reputation.

By keeping careful records of your payroll, you can make sure you’re following all the laws, like the National Minimum Wage and rules about working hours and pensions. Good records also make it easier to give your staff the right information when they ask and help you make smart decisions about things like hiring and how to use your resources.

There are lots of tools and software available to help you keep track of your payroll and follow the rules. From online systems to programs that do reports for you, there are plenty of options to make managing your payroll easier. By using these tools, you can reduce the risk of making mistakes and save time.

Action Points:

Maintain Accurate & Detailed Payroll Records: Ensure comprehensive records on employee earnings, tax deductions, and National Insurance contributions.

Comply with HMRC Regulations: Adhere to HMRC guidelines for payroll record-keeping to avoid legal issues and fines.

Prevent Payroll Errors: Accurate records minimize the risk of employee pay mistakes, protecting your practice’s finances and reputation.

Payroll Tools & Software: Explore online systems and reporting software to streamline record-keeping and reduce errors.

How to Choose the Right Payroll Software for your Dental Practice

Choosing the right payroll software for your dental practice is a big decision. It can make things run smoother, cut down on mistakes, and make sure you’re following the rules from HMRC. But with so many options out there, it can be hard to know which one is best for your practice.

When you’re looking at payroll software, there are a few important things to think about. First, it should be easy to use, with a simple layout that anyone can understand, no matter how much they know about payroll. It should also have features that automate tasks, so you don’t have to spend ages doing things manually. And it needs to be able to grow with your practice, so it can handle changes like hiring more staff or changing how much people get paid.

It’s also important that the software works well with any other systems you already use, like your practice management software. This makes it easier to transfer data between them and reduces the risk of mistakes. And having real-time reporting features is a big plus too, because it means you can see how your practice is doing financially whenever you need to.

Action Points:

Prioritize User-Friendliness: Select software with a simple and intuitive interface for ease of use.

Automate Tasks: Opt for software with features that automate payroll processes to minimize manual work.

Scalability: Choose software that can adapt to growth, accommodating additional staff or changing pay structures.

Integration: Ensure compatibility with existing practice management software to facilitate data transfer and reduce errors.

Real-Time Reporting: Prioritize software with real-time reporting functionalities.

Understanding Your Business Structure

Understanding the different types of business structures is important for managing your finances properly.

If you’re a sole trader, you’re in charge of everything, but you’re also personally responsible for any money the business makes or loses. You’ll need to fill in a Self-Assessment tax return each year, which includes income tax and Class 2 NICs on your profits.

If you’re in a partnership, you and your partners share the money the business makes or loses based on what you’ve agreed. Each partner pays tax and Class 2 NICs on their share of the profits.

If you have a limited company, your personal money is separate from what the business makes. You’ll get paid a salary and might also get dividends, which have different tax rules. The company pays Corporation Tax on its profits, and has to pay Employer’s NICs.

Action Points:

Identify Business Structure: Understand the financial implications of your chosen business structure (sole trader, partnership, limited company).

Sole Trader Taxes: Be aware of personal responsibility for business finances and the requirement to file Self-Assessment tax returns (income tax & Class 2 NICs).

Partnership Taxes: Recognize shared responsibility for profits/losses with partners and individual tax obligations based on profit share (income tax & Class 2 NICs).

Limited Company Taxes: Distinguish between personal income (salary/dividends) and company profits. Salary and dividends have separate tax implications.

Company Tax Obligations: The company is liable for Corporation Tax on profits and Employer’s NICs.

Paying Yourself as a Practice Owner

Deciding how to pay yourself as a practice owner involves thinking about a few things. Firstly, you need to consider what’s fair for you and how much money the practice can afford to pay you. Then, you might want to think about whether to pay yourself through a salary or dividends.

If you pay yourself a salary, you’ll have to pay income tax and National Insurance on it, but you can also make contributions towards your pension. On the other hand, if you pay yourself dividends, you might pay less tax overall, but it depends on how much profit the practice makes and your personal tax situation. It’s important to get advice from a professional accountant to make sure you’re making the best choice for you and your practice.

Action Points:

Balance Fair Pay & Practice Affordability: Determine a salary that is fair for your contributions while considering the financial health of the practice.

Salary vs. Dividends: Evaluate the pros and cons of paying yourself through salary (income tax & National Insurance but allows pension contributions) or dividends (potentially lower tax but depends on profits and personal tax situation).

Seek Professional Advice: Consult with an accountant to determine the optimal compensation strategy for you and your practice.

Payroll for Dentists FAQs

What is payroll, and why is it important for dental practices?

Payroll is the process of managing employee compensation, including salaries, wages, bonuses, and deductions. It’s crucial for dental practices to ensure accurate and timely payments to staff, comply with tax laws, and meet obligations like PAYE (Pay As You Earn) and National Insurance contributions. Proper payroll management also helps with financial planning, maintaining staff satisfaction, and avoiding penalties from HMRC for late or incorrect filings.

How do I set up payroll for my dental practice?

To set up payroll for your dental practice, start by registering as an employer with HMRC to obtain a PAYE (Pay As You Earn) reference. Choose payroll software that suits your needs, ensuring it can handle tasks like calculating taxes, National Insurance contributions, and managing employee benefits. You’ll need to keep accurate records, submit Real Time Information (RTI) to HMRC each time you pay employees, and ensure compliance with auto-enrollment pension requirements.

What are PAYE and National Insurance contributions?

PAYE (Pay As You Earn) is a system where employers deduct income tax and National Insurance contributions from employees’ wages before they are paid. National Insurance contributions are payments made by both employers and employees to fund state benefits like the NHS and pensions. These contributions are calculated based on earnings and must be reported to HMRC through payroll. Managing PAYE and National Insurance correctly is crucial for compliance and ensuring employees receive the correct entitlements.

What are the key payroll deadlines for dental practices?

Key payroll deadlines for dental practices include:

Monthly PAYE submissions: Must be sent to HMRC on or before each payday.

PAYE payments: Due to HMRC by the 22nd of the following month (or the 19th if paying by post).

End-of-year tasks: Submit final Full Payment Submission (FPS) by 5th April and issue P60s to employees by 31st May.

P11D forms: Must be submitted by 6th July for employee benefits.

Missing these deadlines can result in penalties from HMRC.

How do I manage auto-enrollment for pensions?

To manage auto-enrollment for pensions in your dental practice, first, assess your employees’ eligibility. Then, select a suitable pension scheme that meets government criteria. Automatically enroll eligible employees and ensure contributions are made both by the employee and the employer. Communicate with your staff about the scheme and their rights, including how they can opt out if they choose. Regularly review and update your payroll systems to ensure ongoing compliance with auto-enrollment regulations.

What payroll software is recommended for dental practices?

Recommended payroll software for dental practices typically includes features like automated PAYE calculations, National Insurance management, and pension auto-enrollment. Popular options are Xero, QuickBooks, and Sage, which offer user-friendly interfaces and integration with other accounting tools. These platforms can help streamline payroll processing, ensure compliance with HMRC regulations, and manage employee benefits efficiently. Choosing software that meets the specific needs of your practice is crucial for effective payroll management.

Can I outsource payroll management?

Yes, you can outsource payroll management for your dental practice. Outsourcing to a specialized payroll service provider can save time, reduce errors, and ensure compliance with tax laws and regulations like PAYE, National Insurance, and pension auto-enrollment. It also allows you to focus more on patient care and practice management while ensuring that payroll is handled professionally and accurately.

How do I handle payroll for part-time and full-time staff?

To handle payroll for both part-time and full-time staff, ensure that pay calculations reflect their respective hours worked. For full-time staff, calculate their pay based on their contracted salary or hourly rate. For part-time staff, calculate based on the actual hours worked or their agreed part-time schedule. Apply appropriate tax, National Insurance contributions, and benefits proportional to their working hours. Using payroll software can help automate these calculations and ensure accuracy.

What are the tax implications of paying bonuses?

Paying bonuses to employees has tax implications, as bonuses are treated as part of their income and are subject to income tax and National Insurance contributions. The bonus amount is added to the employee’s regular earnings for that period, which may push them into a higher tax bracket, resulting in higher tax rates on the bonus. Employers must also consider their own National Insurance contributions on the bonus amounts paid.

How do I report employee benefits through payroll?

To report employee benefits through payroll, you must use the P11D form to inform HMRC of any taxable benefits provided to employees, such as company cars, private health insurance, or other perks. You’ll also need to calculate the Class 1A National Insurance contributions on these benefits and pay them to HMRC. If you use payrolling benefits, the tax on these benefits is deducted through payroll, simplifying the process and reducing the need for P11D forms.

What are RTI (Real Time Information) submissions?

Real-Time Information (RTI) submissions are reports that employers must send to HMRC every time they pay employees. These submissions include details of pay, tax, National Insurance contributions, and other deductions. RTI ensures that HMRC has up-to-date information on each employee’s income and tax status, which helps reduce errors and streamline the process of tax collection. It is a mandatory process for all employers in the UK.

How do I manage payroll for locum dentists?

To manage payroll for locum dentists, treat them as either self-employed contractors or temporary employees, depending on their employment status. If they are self-employed, ensure they invoice your practice, and no tax deductions are made; they handle their own tax and National Insurance. If they are temporary employees, include them in your PAYE system, making appropriate tax and NI deductions. Accurate record-keeping is essential to ensure compliance with HMRC regulations.

What records should I keep for payroll?

For payroll, you should keep records of:

Employee details (names, addresses, National Insurance numbers).

Pay details (gross pay, net pay, deductions, bonuses).

Tax and National Insurance contributions.

Hours worked (especially for part-time and hourly staff).

RTI submissions to HMRC.

Payslips provided to employees.

Records of any benefits provided.

Pension contributions and auto-enrollment details.

Contracts and terms of employment.

Any adjustments or corrections made to payroll.

How do I correct payroll errors or discrepancies?

To correct payroll errors or discrepancies, first identify and verify the mistake, whether it’s an underpayment, overpayment, or incorrect tax calculation. Once confirmed, adjust the payroll records and inform the affected employee(s) of the correction. Submit an amended Full Payment Submission (FPS) to HMRC if necessary. It’s crucial to document the error and the steps taken to correct it, and ensure future payroll runs are accurate to prevent recurring issues.

What are the consequences of missing payroll deadlines?

Missing payroll deadlines can lead to several consequences, including penalties and interest charges from HMRC for late submissions or payments. Employees may also face issues with their tax codes and National Insurance contributions, potentially leading to underpayments or overpayments of tax. Additionally, repeated delays can damage employee trust and morale. It’s crucial to meet all payroll deadlines to avoid these financial and legal complications.

Learn more: Related Articles

Invoice Finance for Pharmacists

This post aims to delve into the mechanics of invoice financing, as well as its advantages and how it can help pharmacists manage their cash flow more effectively.

This post aims to delve into the mechanics of invoice financing, as well as its advantages and how it can help pharmacists manage their cash flow more effectively.

Neha Jain is a skilled content writer with a rich background in business and financial knowledge. With a bachelor’s degree in English Literature and Psychology, Neha has honed her writing skills, furthering her expertise with the Content Writing Master Course (CWMC) at IIM SKILLS and a Content Marketing Certification from HubSpot Academy.

Working alongside our business development experts, Neha specialises in helping accountants, dentists and other healthcare professionals start, scale and sell their businesses.

Reviewed By:

Arun Mehra Samera CEO

Arun, CEO of Samera, is an experienced accountant and dental practice owner. He specialises in accountancy, financial directorship, squat practices and practice management.

Dental Accounts & Tax Specialists

As dental practice owners ourselves, we know what makes a clinic tick. We have been working with dentists for over 20 years to help manage their accounts and tax.

Whether you’re a dental associate, run your own practice or own a dental group and are looking to save time, money and effort on your accounts and tax then we want to hear from you. Our digital platform takes the hassle and the paperwork out of accounts.

To find out more about how you can save time, money and effort on your accounts and tax when you automate your finances with Samera, book a free consultation with one of our accounting team today.

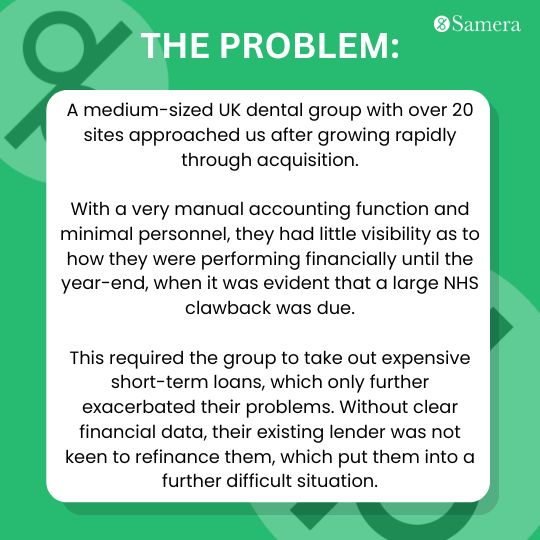

Over the last 20 years, we have seen many dental groups emerge across all parts of the world. Some very large, others smaller, but often seeking to be acquired by the larger groups at some stage, or even the vague hope of an IPO (Initial Public Offering).

The basic premise has always been to buy a dental practice or office at a certain price multiple of EBITDA , add a few more, or a few hundred more, and then sell the whole group at a much higher multiple (with a much bigger EBITDA) than what the individual practices have been acquired for.

Sounds simple – what could go wrong?

Well in a rising market, buyers and group owners who timed their exits rightly have done well financially.

But what about the many hundreds or even thousands of dental groups across the globe that still are operating, but the arbitrage exit opportunity they were hoping for has not manifested?

In the UK in this current high-interest rate environment things look very different for many dental groups.

When rates were low, borrowing was cheap, which aided the growth strategies of many of these groups, yet today, whilst some groups are buying, the appetite to purchase a practice has drastically diminished from not only the smaller groups but also PE-backed ventures too.

Along with the aforementioned higher interest rates, the cost-of-living crisis, and a difficulty in recruitment, have also contributed to the slowdown in many dental groups.

The lack of available manpower has contributed to many NHS-funded dental groups, returning funds to the Department of Health unable to meet their UDA targets.

According to the FT, NHS Dental clawback was around £150million in 2022-23. I expect it won’t be very pretty this year either, from the groups I have been talking to.

Whilst some private dental groups, have struggled to grow the top line as quickly as they had hoped, again due to manpower issues, increased competition and a lack of personnel.

In the good times, its relatively straightforward to make money building a dental group, but in my view it will be the groups that really get to grips with their financials that will emerge strongest in the down times.

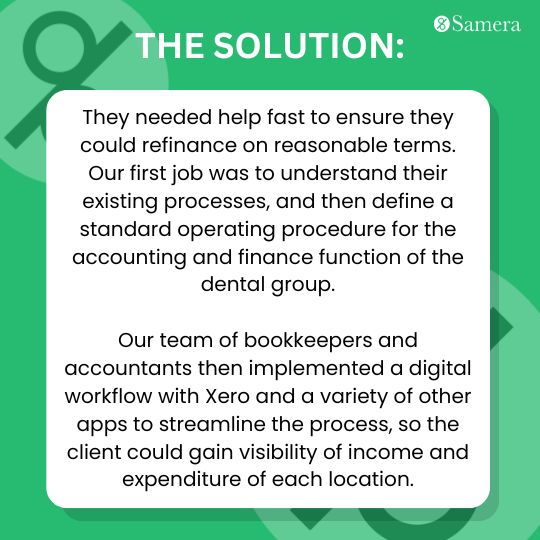

With my wealth of experience over the last 20 years working with a whole host of groups, these are my 6 tips to build a finance and accounting function that will actually grow your EBITDA, but also ensure you achieve the price multiple you desire upon exit.

Tip 1: Have you got a Systems Based Mindset?

The backbone of anything successful organisation are its systems – with the financial and accounting function paramount to success. Unfortunately, I have seen this as a major afterthought by many dental group or DSO owners, seeing it as an overhead rather than something that could help them grow a successful empire.

The first step really is about changing your mindset, and thinking about what data and information do you need to have available at your fingertips to make better decisions.

As it will be interpreting the data to ensure high quality decisions that will determine the success of your group.

You will need robust systems for everything from HR to marketing to compliance to accounting.

I personally like to call it a Systems Based Mindset. So, If you have this, you are on the right track.

Now in the context of finance and accounting, you need to have a solid framework and system in place.

If you don’t, that’s your first starting point. So ask yourself what financial data do you need to know to make good decisions? Examples could include:

Profitability by location

Profitability by Associate Dentist

Hourly rate of each Associate Dentist

Key Overheads as a % of Turnover

Cost of acquiring a new patient

EBITDA to interest coverage ratio

The list is endless, but the above are a good starting point.

The framework will depend on your business structure and how you organised your group but the key factor here is you must be able to see the performance of each of your practices in your group.

There really is no excuse to not be able to see which sites are doing great and which ones aren’t.

They may all be under one company, but it really is essential to have the financial visibility of each site. If you don’t have this, you are at a significant disadvantage when it comes to making quality decisions.

Remember, quality business decisions can only occur when you have visibility of performance. If it’s all jumbled together, you will only get so far, and you won’t be able to develop your group further until you have clarity of performance.

Once you know you need to have financial performance information for each site, then there are numerous accounting systems available to really help you gather the information and automate much of this process.

But the key has to be implementing this correctly. You will need to consider the following:

How to get invoice and income information into the system?

Will it be with an automated OCR system?

Which bookkeeping system is most suitable?

What about standardised charts of accounts?

Will all information be centralised, or will each practice have to send the information separately?

What about purchasing and payment authorities? Do you have controls in place?

Have you a hierarchy in place for this for sign offs?

What about automating much of the accounts payable side of things to speed up payments to suppliers and make your group much more efficient?

More questions than answers, but this process of evaluating the right technology and software is paramount to ensure an efficient finance and accounting function for your dental group.

Tip 4: Choosing the right accounting tech stack for your group.

The world of accounting software has exploded in the last decade.

Of course, the software should be cloud-based, but apart from that you will need professional help to determine the right accounting technology stack for your dental group.

In terms of bookkeeping software, there are well-known products such as Xero, Quickbooks, Sage just to name a few.

But then there is the range of additional apps that could help you streamline and speed up the whole data capture side of things, these include Dext, hubdoc, Approvalmax, Lightyear.

Then when it comes to accounts payable you will want software that will integrate into your chosen bookkeeping software. Software such as Telleroo, Crezco, Payhawk are examples here.

Then for reporting purposes, you may want to consider Spotlight, Syft or Joinn.

The right tech stack can only be implemented once a full understanding of the workflow within your accounting function has been determined.

Tip 5: What About Your Accounting Team?

Time and time again, I have seen inexperienced non-accounting team members get involved in probably one of the most important parts of the group – the money.

Why have a practice manager perform the bookkeeping, when a bookkeeper could do this efficiently and properly?

Garbage in means, garbage out, it is essential to have accurate data entry in a standardised manner, or else any reports you rely on will be inaccurate and lead to poor decision-making.

Therefore, having the right people doing the right job is a pre-requisite here.

The larger the dental group the larger the team will be, which will include bookkeepers and accountants.

You can hire internally for these roles, or alternatively outsource this to firms like ours that have the experienced manpower to support your group.

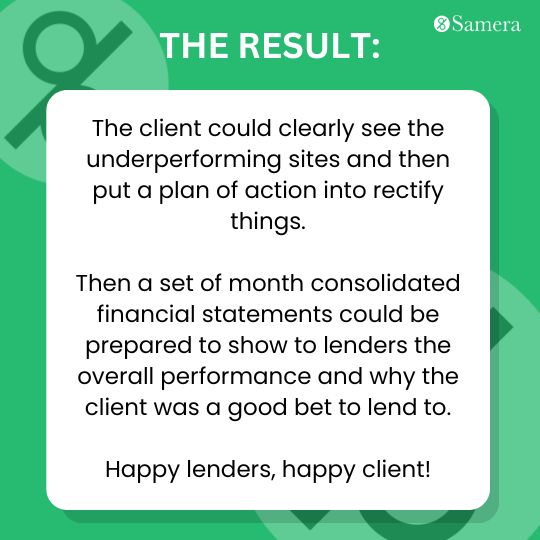

The bookkeeping should be done daily, with the management accounts available at the end of each month, and a review of each practice’s performance should be evaluated – that’s when you know if things are going to plan.

Without a regular review of performance, assuming you have followed steps 1 to 5 above, it would have been a pointless exercise.

Therefore, make sure you review the performance of each site and then take any necessary action swiftly.

The numbers always tell the story, but your whole finance and accounting function must been structured and enabled to tell you the full story, not a half-baked cobbled-together story of your dental group’s performance.

If you are a Dental Group or DSO anywhere across the world, with our shared service centre with talented team members, we can help you implement and run a much more efficient accounting and finance function but also help you grow a better dental group or DSO.

As that’s the ultimate aim, to build a quality dental group that creates value for all stakeholders.

Good luck, and get in touch if you need assistance.

How should I set up accounting systems for a dental group?

To set up accounting systems for a dental group, start by choosing robust accounting software that can handle multiple locations and centralize financial data. Implement standardized processes across all practices for tracking income, expenses, and payroll. Set up a unified chart of accounts to maintain consistency in financial reporting. Ensure regular financial reviews and reconciliations to monitor performance and cash flow. Finally, train staff on the accounting procedures to ensure accuracy and compliance.

What are the best practices for managing cash flow across multiple practices?

To manage cash flow across multiple dental practices, maintain a centralized cash flow management system to monitor income and expenses. Implement standardized invoicing and payment processes to ensure timely billing and collection. Regularly review cash flow statements to identify trends and address issues quickly. Use budgeting and forecasting tools to plan for future cash needs and allocate resources efficiently. Keep reserves for unexpected expenses and consider inter-practice loans to balance cash flow between locations.

How do I ensure compliance with tax regulations for a dental group?

To ensure compliance with tax regulations for a dental group, centralize your accounting to track all income, expenses, and payroll accurately. Regularly review tax obligations for each practice, including VAT, corporation tax, and PAYE, and ensure timely submissions to HMRC. Implement standardized processes across all locations and work with a tax advisor familiar with dental practices to stay updated on regulatory changes. Conduct regular audits to identify and correct any discrepancies.

What accounting software is recommended for dental groups?

For dental groups, recommended accounting software includes options like Xero, QuickBooks, and Sage. These platforms offer features tailored for multi-practice management, such as centralized financial tracking, payroll integration, and real-time reporting. They also provide scalability to accommodate the growth of your dental group and ensure compliance with tax regulations. It’s important to choose software that integrates well with other tools you use and provides robust support for managing multiple locations.

How can I streamline payroll for multiple dental practices?

To streamline payroll for multiple dental practices, use centralized payroll software that handles multi-location payroll processing efficiently. Automate calculations for salaries, taxes, and benefits across all practices, ensuring consistency. Set up a unified system for employee records and time tracking to simplify payroll management. Regularly review and update payroll data to ensure accuracy and compliance with tax regulations. Outsourcing payroll management to a specialized provider can also reduce administrative burden and ensure efficiency.

What financial reports are essential for managing a dental group?

Essential financial reports for managing a dental group include:

Profit and Loss Statement: Tracks income and expenses, showing overall profitability.

Cash Flow Statement: Monitors cash inflows and outflows, ensuring liquidity.

Balance Sheet: Displays the group’s assets, liabilities, and equity.

Budget vs. Actual Report: Compares projected budgets with actual financial performance.

Payroll Report: Details employee compensation, including taxes and benefits.

These reports are critical for making informed financial decisions and maintaining the financial health of the dental group.

How do I handle inter-practice billing and expenses?

To handle inter-practice billing and expenses within a dental group, establish a centralized system to track and allocate costs accurately across all practices. Use accounting software to automate the allocation of shared expenses, such as marketing or administrative costs, to ensure each practice bears its fair share. Implement clear policies for inter-practice billing, detailing how expenses will be tracked, billed, and reconciled. Regularly review these processes to maintain transparency and ensure accuracy.

What are the key considerations for budgeting in a dental group?

Key considerations for budgeting in a dental group include:

Revenue Projections: Estimate income for each practice based on patient volume and services offered.

Expense Management: Track fixed and variable costs, including salaries, rent, and supplies.

Cash Flow Planning: Ensure liquidity to cover operational costs and unforeseen expenses.

Capital Expenditures: Plan for investments in new equipment or technology.

Profit Margins: Monitor profitability across all practices to maintain financial health.

How often should I review financial performance across practices?

You should review financial performance across practices on a monthly basis. Regular monthly reviews help you monitor key metrics like revenue, expenses, and profitability, allowing you to address issues promptly and adjust strategies as needed. Quarterly reviews can provide a broader perspective on trends, while annual reviews are essential for strategic planning and setting long-term goals. Consistent monitoring ensures that each practice remains financially healthy and contributes positively to the overall group.

How do I manage debt and credit within a dental group?

To manage debt and credit within a dental group, first, establish clear policies for borrowing and repayment to maintain healthy cash flow. Regularly review debt levels across practices and prioritize paying off high-interest debt to reduce financial strain. Use credit responsibly to finance essential investments, and monitor credit terms closely to avoid penalties. Maintain a strong relationship with lenders and ensure that all practices contribute to meeting debt obligations.

What role does inventory management play in accounting for a dental group?

Inventory management plays a crucial role in accounting for a dental group by ensuring accurate tracking of supplies and materials across practices. Effective inventory management helps control costs, reduce waste, and maintain optimal stock levels, which directly impacts cash flow and profitability. It also supports accurate financial reporting by aligning inventory levels with expenses, ensuring that supplies are accounted for in the right periods. Implementing inventory management software can streamline this process and improve overall financial efficiency.

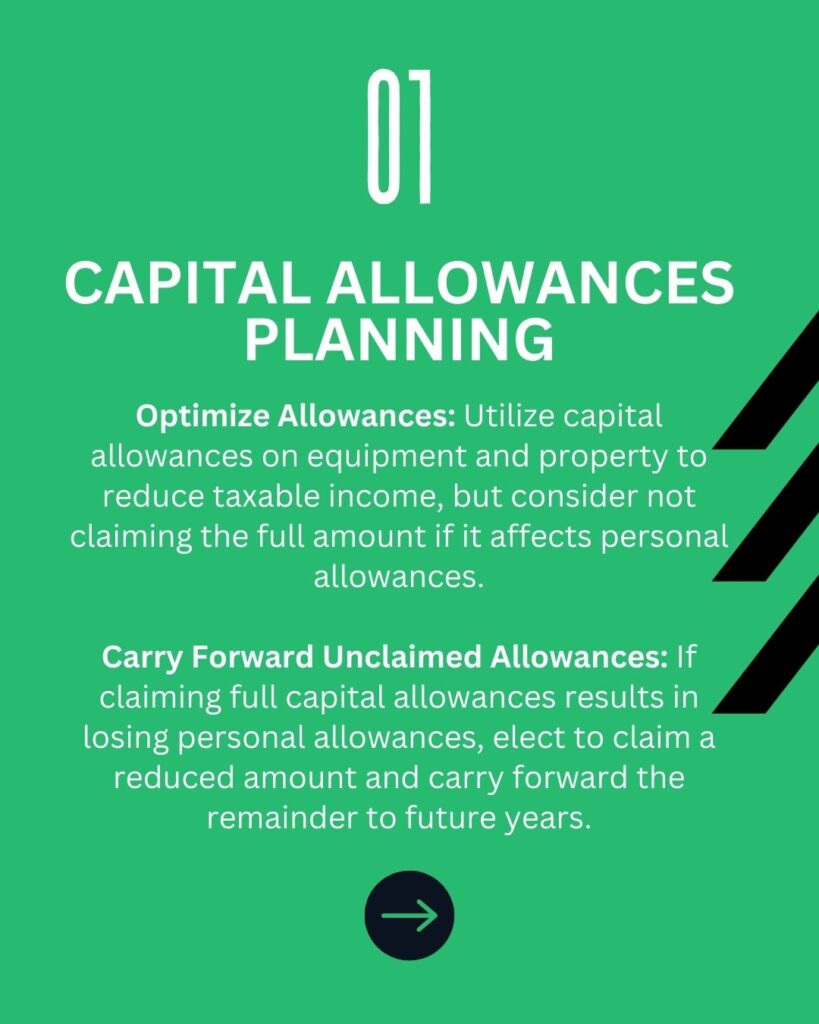

How can I optimize tax planning for a dental group?

To optimize tax planning for a dental group, consider consolidating expenses and leveraging tax-efficient structures like group relief to offset profits and losses across practices. Utilize capital allowances for equipment and property investments, and ensure that you maximize allowable deductions and credits. Strategic timing of income and expenses, along with regular reviews of tax liabilities, can help reduce the overall tax burden. Consulting with a tax advisor who specializes in dental practices can provide tailored strategies for your group.

What are the benefits of centralized vs. decentralized accounting?

Centralized Accounting:

Offers consistency and control by consolidating financial data from all practices in one place.

Enhances efficiency through standardized processes and reporting.

Facilitates easier compliance with regulations.

Decentralized Accounting:

Allows individual practices to maintain control over their financial operations.

Can be more responsive to the specific needs of each practice.

May lead to inconsistencies and require more oversight to ensure accuracy and compliance across the group.

How do I track profitability for each practice in a dental group?

o track profitability for each practice in a dental group:

Use Individual Profit and Loss Statements: Generate P&L statements for each practice to monitor revenue, expenses, and net income.

Allocate Shared Costs: Distribute shared expenses, like marketing or administrative costs, proportionally.

Monitor Key Metrics: Track metrics such as patient revenue, cost per patient, and operating margins.

Use Accounting Software: Implement software that supports multi-practice financial tracking.

Regularly review these reports to assess performance and make informed decisions.

What challenges might I face in managing the accounts of a growing dental group?

Managing the accounts of a growing dental group can present several challenges:

Complexity: Increased financial transactions and inter-practice billing can complicate accounting.

Consistency: Ensuring standardized financial processes across multiple practices is difficult.

Compliance: Keeping up with tax regulations and legal requirements across all practices can be challenging.

Cash Flow Management: Balancing cash flow between practices and funding growth without overextending resources is essential.

Scalability: Accounting systems may need upgrades to handle the expanded operations effectively.

I have a small dental group of just 2 sites, does the methodology outlined apply here too?

Yes.

In our experience, having a well-thought-through workflow which is expandable is key to success. Get this structure right, and you then have a solid platform for your 2 sites, and any additional sites you acquire or start up.

This sounds complex, can Samera help my dental group?

Simply yes. We can help you with the whole set up and running of the accounting and finance operation of your dental group, or just one aspect, including providing experienced team members to carry out all aspects of the work required.

What’s the first step in setting this all up?

In our experience, the key is to understand your existing processes and workflows, and then define a detailed workflow for your organisation. Our advice would be to implement this stage by stage, rather than all at once.

How much experience does team Samera have in this area?

We have been working with Dental groups and DSO’s for over twenty years, so we have seen most things, and also through our sister business, The Neem Tree Dental Group, we test all our processes, to ensure they are robust before sharing with our dental group clients.

Does team Samera work with international Dental Group clients?

Yes.

Our expertise in this area is second to none, so we can work with DSO’s or Dental Groups across the UK, Europe, North America, the Middle East and Asia.

With almost twenty years of commercial experience and knowledge in Dentistry, Arun’s expertise is valued by hundreds of businesses across the UK. His financial acumen and know-how, along with his hands-on commercial expertise have helped clients, large and small, new and established to achieve great things.

Arun is the founder of the Samera Group, starting the business with just one client sitting at his father’s dining table. Fifteen years on, Team Samera now service hundreds of Dental clients, run exciting events, help clients raise finance, and are very active in helping clients buy or sell Dental practices.

Dental Accounts & Tax Specialists

As dental practice owners ourselves, we know what makes a clinic tick. We have been working with dentists for over 20 years to help manage their accounts and tax.

Whether you’re a dental associate, run your own practice or own a dental group and are looking to save time, money and effort on your accounts and tax then we want to hear from you. Our digital platform takes the hassle and the paperwork out of accounts.

To find out more about how you can save time, money and effort on your accounts and tax when you automate your finances with Samera, book a free consultation with one of our accounting team today.

Simplifying Bookkeeping: Essential Tips for Dentists

Running a successful dental practice involves more than just being a good dentist. You also need to take care of your money. Keeping track of your finances and managing your payroll are important, but they can be complicated and take up a lot of time.

With accurate records and keeping track of your money, you’ll be on top of things like taxes, have enough cash to keep the office running, and be able to make smart choices about your practice, like buying new equipment or hiring more staff.

As a dentist, your time is valuable and should be spent on treating your patients well. That’s why it’s important to simplify your financial tasks. In this article, we’ll explain the basics of bookkeeping and give you essential tips and methods to help you make your financial tasks easier. We’ll talk about everything from choosing the right accounting software to outsourcing your financial tasks. By following these tips, you’ll be able to improve your financial management and focus on providing good dental care to your patients.

What is Bookkeeping?

Bookkeeping is like having a detailed diary for your dental practice’s financial activities. It’s all about jotting down every penny that comes in (like payments from patients) and every penny that goes out (like paying bills for supplies or staff salaries). Basically, it’s keeping track of all the money-related things happening in your practice.

Now, let’s talk about bookkeeping versus accounting. Think of bookkeeping as the groundwork, like laying bricks for a house. It’s about recording every financial move and keeping things organized day-to-day.

On the flip side, accounting is like taking those bricks and building a whole house. Accountants use the info from bookkeeping to analyse how your practice is doing financially. They look at stuff like how much money is coming in, how much is going out, and how profitable your practice is. They also help with smart money decisions and making sure you’re all good with taxes.

So, in short, bookkeeping is like keeping track of the score by writing down every money move. And accounting is taking that score and figuring out what it all means for your practice’s financial health.

The Bookkeeping Process Explained

Conducting bookkeeping for your dental practice involves several key steps:

Choosing a System: With recent changes in UK tax and accounting laws, it is now required that you use an automated, digital accounting software. This software has to be compliant with the Making Tax Digital regulations. Systems like Xero and Quickbooks are some of the more well known.

Recording Transactions: It’s crucial to track income and expenses daily to maintain accurate financial records. This includes recording payments from patients, insurance reimbursements, supplier invoices, payroll expenses, and any other financial transactions related to the practice. Daily tracking ensures that no transactions are overlooked and provides real-time insight into the practice’s financial health.

Categorizing Expenses: Proper expense categorization is essential for generating accurate financial reports and analysing spending patterns. Dentists should categorize expenses into relevant categories such as office supplies, rent, utilities, payroll, equipment maintenance, and marketing. Consistent categorization makes it easier to track and manage expenses and ensures compliance with tax regulations.

Reconciling Bank Statements: Dentists should regularly reconcile their bank statements with their bookkeeping records to verify accuracy and identify any discrepancies. This involves comparing the transactions recorded in the bookkeeping system with those listed on the bank statement and investigating any discrepancies. Reconciliation ensures that all transactions are accounted for and helps detect errors or unauthorized charges.

Generating Reports: Dentists should regularly generate basic financial reports such as income statements and balance sheets to assess the practice’s financial performance and position. Income statements provide an overview of revenue and expenses over a specific period, while balance sheets summarize the practice’s assets, liabilities, and equity. These reports help dentists track profitability, monitor cash flow, and make informed financial decisions to support practice growth and sustainability.

By following these steps, practice owners. can effectively conduct bookkeeping for their dental practice, ensuring accurate financial records, compliance with regulations, and informed decision-making to achieve long-term success.

The Importance of Simplified Bookkeeping and Payroll for Dentists

As a dental practice owner, it’s crucial to understand your practice’s finances and follow the rules for the dental industry and the UK’s tax codes. Here’s why:

Informed Financial Decisions: Accurate bookkeeping provides dentists with a clear picture of their practice’s financial health, enabling them to make informed decisions about important investments such as equipment purchases and staffing levels. By understanding their revenue streams and expenses, dentists can allocate resources effectively to support the growth and efficiency of their practice.

Payroll Management: Managing payroll is equally important for dentists. As a business owner, you have legal responsibilities to your employees, including making accurate payroll calculations, making timely payments, and complying with labor laws. By simplifying your payroll process, you can ensure that your staff are paid correctly and on time, reducing the risk of disputes or legal complications.

Accurate Tax Filing: Proper bookkeeping ensures that dentists maintain detailed records of income, expenses, and deductions, facilitating accurate tax filing. By staying organized throughout the year, dentists can minimize their tax liabilities and avoid penalties or audits from tax authorities.

Practice Profitability: Through diligent bookkeeping, dentists can track practice profitability by analysing revenue, expenses, and profit margins. This insight allows them to identify areas for improvement, optimize operational efficiency, and maximize profitability over time.

Cash Flow Management: Effective bookkeeping helps dentists manage cash flow by monitoring incoming revenue and outgoing expenses. By staying on top of cash flow, dentists can ensure they have sufficient funds to cover operational expenses, such as payroll and supplies, and maintain financial stability even during periods of fluctuating income.

Insurance Payments and Patient Billing: Bookkeeping also plays a crucial role in managing insurance payments and patient billing. By accurately recording insurance reimbursements and patient payments, dentists can track outstanding balances, follow up on unpaid invoices, and maintain strong financial relationships with insurance providers and patients.

In summary, improved accounting and payroll are essential for dentists to ensure financial stability, compliance with regulatory requirements, and efficient practice management. By paying attention to these aspects of your business, you can streamline your operations, reduce stress, and allocate more time to delivering excellent dental services to your patients.

In the following sections, we will explore practical tips and strategies to help you simplify your accounting and payroll processes, empowering you to take control of your dental practice’s financial well-being.

Understanding the Specific Bookkeeping and Payroll Requirements for Dentists

As a dentist, it’s important to know the unique financial rules that apply to your job. Dental practices have their own money-related considerations that are different from other businesses. Being aware of these details will make it easier to manage your finances.

One crucial thing to think about is the money coming in and going out. In dentistry, you might have various sources of income, like patient fees, payments from government healthcare programs, and insurance payments. It’s essential to keep accurate records of all these income sources for proper financial reporting.

Dental practices also have various expenses, such as staff salaries, dental supplies, equipment maintenance, and rental costs. Keeping detailed records of these expenses will not only help with accurate financial reports but also identify areas where you can save money and plan your budget.

Besides income and expenses, dentists need to follow the rules set by organizations like the General Dental Council (GDC) and HM Revenue and Customs (HMRC). These organizations have specific requirements for record-keeping and tax obligations. Failing to meet these requirements can lead to penalties and legal problems. So, it’s crucial to stay updated on the latest rules and make sure your financial processes follow the necessary guidelines.

To simplify your financial management as a dentist, consider using specialized accounting software designed for dental professionals. These software solutions often have features that cater to the unique needs of dentists, such as tracking lab fees, managing patient records, and generating reports tailored to the dental industry. Implementing such software can streamline your financial processes, save you time, and reduce the chances of errors.

By understanding the specific financial requirements for dentists, you can ensure accurate financial records, compliance with regulations, and more efficient management of your dental practice’s finances. Improving these processes will not only save you valuable time and effort but also contribute to the overall success and stability of your dental business.

Action points

Identify Income Sources: List all the ways your practice generates income (patient fees, insurance, government programs).

Track Expenses by Category: Separate your business costs into categories (salaries, supplies, equipment, rent) for better budgeting.

Research GDC & HMRC Regulations: Look up the latest record-keeping and tax requirements from the GDC and HMRC to ensure compliance.

Choosing the Right Accounting Software for Efficient Record-keeping

Choosing the right accounting software is crucial for dentists to maintain efficient record-keeping practices. Thanks to technology advancements, dentists have various options to choose from, each with its own unique features and benefits.

First, it’s important to consider your dental practice’s specific needs. Look for accounting software designed for healthcare professionals, offering features like invoicing, expense tracking, and payroll management. This ensures you have a comprehensive system that can handle all your financial and payroll requirements.

Another important factor to think about is how easy the software is to use. As a dentist, you may not have extensive accounting knowledge or experience, so it’s essential to choose user-friendly software that is easy to navigate. Look for features like a simple interface, clear instructions, and helpful customer support to make the transition to using the software smooth.

Integration capabilities are also worth considering when selecting accounting software. Look for software that can seamlessly work with other systems you use in your dental practice, such as appointment scheduling or patient management software. This will save you time and effort by eliminating the need for manual data entry and ensuring that all your systems work together smoothly.

Security should be a top priority when choosing accounting software. As a healthcare professional, you handle sensitive patient information, so it’s crucial to pick software that prioritizes data security and confidentiality. Look for software that offers encryption, regular data backups, and strong access controls to protect your financial and patient data.

Finally, consider your budget when selecting accounting software. There are both free and paid options available, so it’s important to weigh the features and benefits against the cost. While free software may be tempting, keep in mind that paid options often offer more robust features and better customer support.

By carefully considering these factors and choosing the right accounting software, dentists can streamline their accounting and payroll processes, saving time and ensuring accurate financial records for their practices.

Action points

Consider your dental practice’s specific needs, such as features like invoicing, expense tracking, payroll management, and integration with other systems.

Choose software that is easy to use and navigate, with a simple interface, clear instructions, and helpful customer support.

Prioritize data security by choosing software that offers encryption, regular data backups, and strong access controls.

Consider your budget when weighing the features and benefits against the cost.

Free software may be tempting, but keep in mind that paid options often offer more robust features and better customer support. We recommend looking into Xero and Sage.

Did You Know?

Dentists in the UK must keep accurate financial records for all business transactions. This requirement is set out in the General Dental Council (GDC) Standards for Dental Professionals (2019), which state that dentists must “keep accurate and up-to-date records of all your financial transactions, including income and expenditure.”

Dentists in the UK must deduct tax and National Insurance contributions from their employees’ salaries. This is required by the Income Tax (Earnings and Pensions) Act 2003 and the National Insurance Contributions Act 2010.

Dentists in the UK must submit VAT returns to HMRC quarterly. This requirement is set out in the Value Added Tax Act 1994.

Dentists in the UK must submit payroll information to HMRC monthly. This requirement is set out in the Pay-as-You-Earn (PAYE) Regulations 2003.

Dentists in the UK must also submit an annual tax return to HMRC. This requirement is set out in the Income Tax (Self Assessment) Act 1996.

Organizing and Categorizing Expenses for Easy Tracking and Tax Purposes

When it comes to handling the money side of your dental practice, organizing and sorting your expenses is important for easy tracking and tax purposes. Keeping your expenses clear and properly categorized helps you stay organized and ensures you’re taking advantage of all eligible tax deductions.

To make this process easier, start by setting up a system to record and categorize your expenses. This can be as simple as using a spreadsheet or investing in accounting software designed for small businesses. Make sure to create categories that match the tax rules in the UK, such as office supplies, equipment, professional services, and marketing expenses.

To stay on top of your expenses, establish a regular schedule for recording and categorizing them. Allocate dedicated time each week or month to review your receipts, invoices, and financial documents. This will help you identify any missing or undocumented expenses and ensure that everything is accurately categorized.

In addition to organizing and categorizing expenses, it’s essential to keep all relevant documents in a reliable and easily accessible place. This includes receipts, invoices, bank statements, and any other financial records. Having these documents readily available will make it easier for you to provide accurate information during tax season and any potential audits.

By focusing on the organization and categorization of expenses, you’ll simplify your accounting and payroll processes and ensure compliance with tax regulations. This will give you peace of mind and allow you to focus on providing quality dental care to your patients.

Action points

Set up a system to record and categorize your expenses, such as using a spreadsheet or accounting software.

Create categories that match the tax rules in the UK, such as office supplies, equipment, professional services, and marketing expenses.

Establish a regular schedule for recording and categorizing expenses, such as each week or month.

Keep all relevant documents in a reliable and easily accessible place, such as receipts, invoices, bank statements, and other financial records.

As a dentist, managing the payroll for your dental staff can be a time-consuming task. However, streamlining your payroll processes can help you save time and ensure accuracy in your financial records. Here are some basic tips to improve your dental staff payroll:

Use payroll software: Invest in reliable payroll software designed specifically for small businesses. This software can automate various payroll tasks like calculating wages, deductions, and tax payments. It will also generate pay stubs for your dental staff, making the process more efficient and error-free.

Create a consistent payroll schedule: Establish a consistent payroll schedule, such as bi-weekly or monthly, and clearly communicate it to your dental staff. This will help them know when they will be paid, reducing any confusion or inquiries.

Implement direct deposit: Encourage your dental staff to sign up for direct deposit, where their wages are electronically transferred directly into their bank accounts. This eliminates the need for physical checks, reduces the risk of loss or theft, and saves time on manual check distribution.

Maintain accurate employee records: Keep detailed records for each dental staff member, including personal details, tax information, and employment contracts. This ensures that you have all the necessary information readily available for payroll calculations and reporting.

Stay updated with payroll regulations: Payroll regulations and tax rules can change frequently. It’s important to stay informed about any updates that may affect your dental staff’s wages and deductions. Consider consulting with a professional payroll service provider or an accountant to ensure compliance with the latest regulations.

Automate tax calculations and filings: Tax calculations can be complex, especially when considering deductions and allowances specific to the dental industry. Use payroll software that can automatically calculate taxes based on the latest tax rates and rules. Additionally, consider automating your tax filing process to ensure timely and accurate submissions.

By implementing these tips, you can streamline your dental staff payroll processes, reduce administrative burdens, and ensure accurate financial records for your dental practice. Simplifying accounting and payroll will not only save you time but also contribute to the overall efficiency and success of your dental business in the UK.

Action points

Invest in payroll software designed specifically for small businesses.

Establish a consistent payroll schedule and communicate it to your staff.

Encourage your staff to sign up for direct deposit.

Keep detailed records for each staff member.

Stay updated with payroll regulations and tax rules.

Implementing Automated Systems for Accurate and Timely Payments

Using automated systems for accurate and timely payments can be a great benefit for dentists. Managing finances and payroll can often be time-consuming and prone to mistakes, leading to unnecessary stress and financial difficulties.

By using automated systems, dentists can streamline their payment processes and ensure that employees and suppliers are paid correctly and on time. This not only saves valuable time but also helps maintain positive relationships with staff and vendors.

One effective way to implement automated systems is by using accounting software specifically designed for dentists or small businesses. These software solutions are tailored to the unique needs of dental practices, offering features like automated payroll calculations, invoice generation, and expense tracking.

With the help of such software, dentists can easily input employee hours, track leave entitlements, and calculate deductions for taxes and benefits. This eliminates the need for manual calculations and reduces the risk of errors in payroll processing.

Moreover, automated systems can integrate with online payment platforms, allowing dentists to electronically pay suppliers and contractors. This ensures prompt payments and provides a convenient and secure method for financial transactions.

Additionally, automated systems can generate detailed reports and summaries, providing dentists with valuable insights into their practice’s financial health. These reports can help identify areas for cost savings, track revenue streams, and monitor overall efficiency.

In summary, implementing automated systems for accurate and timely payments is a crucial step in simplifying accounting and payroll for dentists. By embracing technology and streamlining financial processes, dentists can focus more on providing quality dental care while ensuring the financial stability of their practice.

Action points

Use accounting software specifically designed for dentists.

Input employee hours and track leave entitlements to automate payroll calculations.

Integrate with online payment platforms to electronically pay suppliers and contractors.

Generate detailed reports and summaries to monitor financial health and identify areas for improvement.

Staying Compliant with HMRC Regulations and Reporting Requirements

Staying in line with HMRC (His Majesty’s Revenue and Customs) rules and reporting requirements is important for dentists in the UK. As the owner of a dental practice, it’s your responsibility to make sure that your financial and payroll processes follow the specific rules set by HMRC.

One of the first steps to stay compliant is to register your dental practice with HMRC. This will allow you to get a Unique Taxpayer Reference (UTR) number, which is essential for all tax-related communication.

Next, you need to establish a strong accounting system that accurately records all financial transactions and keeps the necessary documents. This includes keeping track of income, expenses, invoices, receipts, and any other important financial records.

Staying updated with payroll regulations is also crucial. This involves correctly categorizing your dental staff as employees or self-employed contractors and ensuring that their wages are calculated accurately, including any deductions for taxes and national insurance contributions.

In addition to accurate record-keeping, you must also meet reporting requirements set by HMRC. This includes submitting timely and accurate VAT returns, payroll information, and annual tax returns. Failure to meet these obligations can result in penalties and potential legal issues.

To simplify the process, consider using advanced accounting and payroll software designed specifically for dentists. These tools often come with features that automate calculations, generate detailed reports, and remind you of important deadlines.

Staying compliant with HMRC rules might seem overwhelming, but with proper organization and the right tools, you can streamline your financial and payroll processes, ensuring that you meet all requirements and avoid any unnecessary penalties.

Action points

Register your dental practice with HMRC and get a Unique Taxpayer Reference (UTR) number.

Establish a strong accounting system that accurately records all financial transactions and keeps the necessary documents.

Stay updated with payroll regulations and correctly categorize your dental staff as employees or self-employed contractors.

Ensure that your dental staff’s wages are calculated accurately, including any deductions for taxes and national insurance contributions.

Meet reporting requirements set by HMRC by submitting timely and accurate VAT returns, payroll information, and annual tax returns.

Consider using advanced accounting and payroll software designed specifically for dentists to automate calculations, generate detailed reports, and remind you of important deadlines.

Outsourcing Bookkeeping and Payroll Tasks to Professionals