Cyber security is an essential part of keeping your patients, data and business protected online.

With Samera Cyber Security, you get the tools you need, the know-how to use them and digital copies of all your data. This three-pronged approach means you can keep your business safe and your data safe.

Contact us today to find out more about how our cyber security training, digital protection products and back-up contingencies can help you.

Cyber security is an essential part of keeping your patients, data and business protected online.

With Samera Cyber Security, you get the tools you need, the know-how to use them and digital copies of all your data. This three-pronged approach means you can keep your business safe and your data safe.

Contact us today to find out more about how our cyber security training, digital protection products and back-up contingencies can help you.

Parents are busier than ever, and childcare has become a necessity for many working parents, this has seen a growth in the need for more daycare nurseries in the UK.

As you would imagine daycare nurseries are very highly regulated as they are responsible for the well-being of the children that attend. All nurseries in England are regulated by Ofsted (The Office for Standards in Education). They are expected to adhere to all the rules and regulations set out by Ofsted and they will also undertake inspections to make sure that a satisfactory level of care is being given and that appropriate records of the children’s developments are being kept.

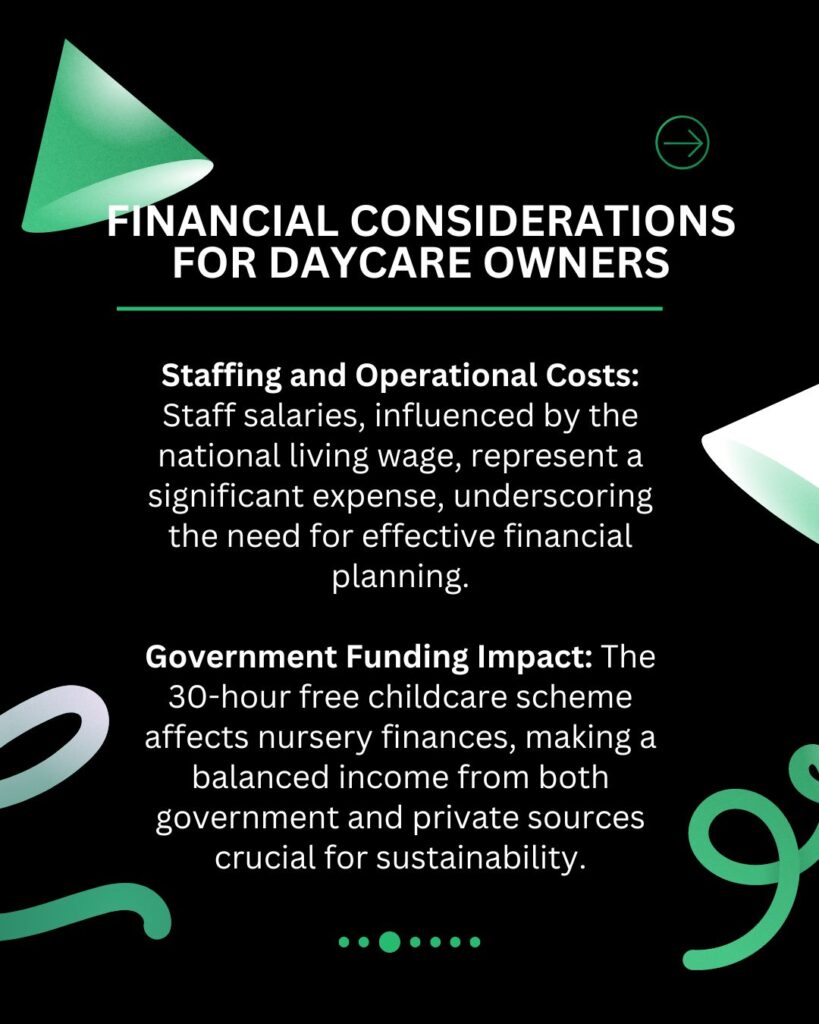

Staffing will be one of the biggest costs to the business, the increases in national living wage have had an impact on the sector. Staff will also be one of the biggest assets and making sure they stay with the company will be important for future business growth.

Having a clear plan for training, promotion, retention, and recruitment will help the nursery maintain the correct number of staff needed to operate a successful nursery.

The government scheme that offers 30 hours of free childcare has impacted the sector and as many nurseries believe that the funds they receive from the government for these hours are not enough to cover their costs, this means that having an income split biased to private income is important to the overall business performance.

Finance for Day Care Owners

We believe that all aspiring daycare and nursery owners should have access to all the necessary information, finance options and support they need in order to successfully open and start their business.

You are one of many in the UK who would like to start their own day nursery. It has slowly become a very popular business venture, as a report by the Department of Education shows that there were 24,00 group-based early years providers in 2019 alone. This figure equates to 8,600 voluntary nurseries and 14,700 private nurseries. This report also states that daycares are in high demand.

We will guide you through the process of starting a successful day care centre. Your next steps will include:

Purchasing a property

Refurbishment funding

Specialist regulations

Equity purchase

Tax funding

Mortgages

Your Business Plan

There are many things you need to consider before you can even start planning your daycare business. If you are ready to enter the sector and make your business as successful as it can be, you need to begin with creating an in-depth, accurate, realistic business plan.

A Business plan is a road map for your business, it will help plan a strategy for marketing, and recruitment and set priorities. The plan is important for existing and start-up businesses and if the business requires finance, lenders will want to see a business plan which sets out the businesses goals, the experience of the management team, and a cash-flow forecast setting out the profitability of the business over the next 2-3 years.

A daycare’s business plan must take into account the unique features that are included in operating in the childcare sector. New entrants should have a clear understanding of the market, the vision for your business and the regulatory environment in which you will be operating. It is very easy to get misled by assumptions based on limited experiences and headlines within a limited division of the sector.

Your business plan will aid you in getting the necessary financing you will need to begin your business and it will also help you stay on track, remain within your budget and, most importantly, it will secure all that important funding.

It is definitely worth spending time on a long, in-depth business plan – a few pages of notes will not suffice. Your business plan needs to prove that you have thought through every single aspect, every angle, and every cost of what will come with starting your daycare business.

Here are a few things you need to consider while you are you are constructing your business plan:

Local environment

A day-care nursery’s business plan should take local demand into account. or be evidently prepared with a strategy to disrupt it. This could include offering services or incentives that your competition doesn’t, such as payment plans or offers that are strong enough to attract local parents who aren’t fully prepared to pay privately.

Fees and extra charges

Not only will you have to carefully plan what you will be charging your clients, but also what your costs to set up will be first. They are both as important as each other. These details, which you may think are minor irrelevant aspects of your business you can decide later, are what is really important. It will show your lender that you are a candidate who is well prepared and ready for a loan.

You need to explore whether the parents will be willing to pay for nappies or would be paying for food, if so, how much? Small details like this that will essentially outline how much income you will receive will set you apart from lenders.

Finance and funding

Based on your needs as a business you need to consider what kind of financing you will need. You may want to consider private-equity funding. Investors are getting increasingly keen on the childcare sector as a strong long-term prospect. There are multiple sources of finance that will be available to you.

Future planning

Consider the size of your location and the feasibility of scaling and expansion. It is important to bear in mind that most regulators set minimum requirements for space per child which may limit your growth.

Government subsidies

Government grants are playing a greater role in childcare now than ever before however, they do vary from area to area. It is worth it for you to research what could be available to you.

Market Research

The day care and nursery sector is a very unique commercial environment, one that has many rules in place before you can even set up and one that can change very quickly as latest trends in provision take off. Not only is the success of your daycare business highly dependent on how you cater to both parental and children’s needs but is also highly dependent on whether your daycare business must meet the specific needs of its catchment area. Here are a few places to start:

Other businesses in the area

You need to download a list of all local registered providers from the relevant regulator. These are Ofsted in England, the Care Inspectorate in Wales, your local authority in Ireland and the Care Inspectorate in Scotland.

Local Needs, Demand and Demographics

Opening a daycare in an area where you have a lot of competition means that it is likely that you may struggle to get your business off the ground. Depending on how affluent the local area is will reflect the needs and expectations of your future clients. Looking at parenting groups on social media will give you an insight into what local parents are looking for.

Business structure

Most nurseries in the UK operate as limited companies.

If the nursery owns the trading/operating business and the freehold then they may decide to own these two entities in separate limited companies. This is normally referred to as Opco/Propco by lenders and they will tie in both businesses by way of security for any lending that they undertake to the nursery.

Here are a few matters that you need to be aware of before you enter the childcare sector:

Liability

Liability is important when deciding any business structure. Incorporation is usually the route most business owners take to minimise any personal risks. However, it is still important to have Directors and Officers cover, as this will enable you to still incur some liabilities.

Franchising Options

You may want to include in your business plan whether franchising will be an option for you. There are many nursery franchises available currently in the UK, which can be a great option for new entrants in the market. However, franchising your current established day care business can be a cost-effective way to build your business.

Unincorporated associations

If you choose to remain unincorporated it is important to ensure that your trustees and officers are protected by an appropriate insurance policy.

Charity Status

There is also an option for your daycare business to be a charitable nursery therefore, if you are considering this option you also need to consider the structure you would like to adopt.

Access to outdoor space is an integral part of your daycare business. If the space you are looking at does not have its own grounds you need to be realistic about the walking distance to local playgrounds and parks.

Potential hazards

In this childcare industry providing a safe environment is paramount and should be always kept as a priority. Are there multiple floors? Are your staircases child-friendly?

Road Safety and Convenience

You need to understand that parents will be evaluating all these different aspects of your business. Examine the nearby street crossings and the amount of nearby parking available. What are the transport links like nearby?

Relationships

Build a strong relationship with the local authority, most areas will have a service/need that they are lacking and if you can offer these services, they will hopefully refer parents to your business. Having good contacts with the schools closest to the nursery will help with attracting new children and ultimately help with the business’s occupancy levels.

Valuation

If you choose to buy your premises, ensure that you have your premises properly valued to help avoid being under-insured.

Raising Finance for Daycare Nurseries

How do lenders view the premises within the Daycare Nursery sector? If the nursery is based in a converted residential property then generally the loan to value (LTV) will be around the 65% mark, however, is based within a purpose-built/limited alternative use property then 55% LTV would be more realistic.

Loan to values (LTV) – these can be based on the bricks and mortar valuation of the freehold or the business trading valuation, lenders will normally decide which matrix that they would want to use, the valuation of the freehold/business will need to be undertaken by an independent valuer. Loans are normally termed over 10-15 years. Some banks will allow you to make lump sum repayments with no charge which can help reduce the term and allow you to repay the loan earlier if that fits within your business model.

The most common ownership structure for a nursery will be as a limited company, this is partly due to tax. A limited company owner must pay corporation and dividend tax, whereas a sole trader will have to pay tax on all business profits. Your accountant will advise you on the most suitable ownership vehicle for your business.

Security – banks will take security for lending in this sector, normally a 1st legal charge over the nursery freehold, limited company debenture (legal charge over the companies’ assets) and a personal guarantee. In the case of Opco/Propco lending, the banks will normally cross guarantee the operating and property company to tie in both the property asset and the trading income.

Finance for Daycare Nurseries with Samera

So how can we at Samera help you achieve your goal of owning a Day Care Nursery? Firstly, we have 30 years collective experience within the banking sector and for the last 10 years specialising within the healthcare sector. Samera Finance can help with an initial assessment, deal structure, business plans and help negotiate a competitive interest rate for your acquisition financing. We have contacts in all the major banks, contacts who have experience of this type of lending to ensure that you get the correct deal especially in respect of the fees and rates of interest. Deal with the wrong lender and they may not give you the favourable rates that healthcare professionals benefit from.

We will obtain for you several offers of finance enabling you to select the deal that suits your own circumstances we will guide you through the lending process and be the point of contact for the lender when they are unable to talk to you while you are working. This enables you to carry on working and if we need to talk through any points with you, we are available in the early evening to do so.

We’ve been helping to fund the future of British healthcare businesses for over 20 years and our team are made up of former bankers with decades of experience in the UK’s healthcare lending sector.

You can find out more about working with Samera and the financial services we offer by booking a free consultation with one of the Samera team at a time that suits you (including evenings) or by reading more about our financial services at the links below.

Make sure you never miss any of our articles, webinars, videos or events by following us on Facebook, LinkedIn, YouTube and Instagram.

Reviewed By:

Nigel Crossman

Head of Commercial Finance

Nigel is a former banker and head of commercial finance at Samera. He specialises in raising finance, negotiating deals and structuring finance applications for healthcare businesses.

Dan Fearon

Finance Manager

Dan is a former banker and the head of our dental practice sales team. He specialises in asset finance for healthcare businesses and dental practice sales.

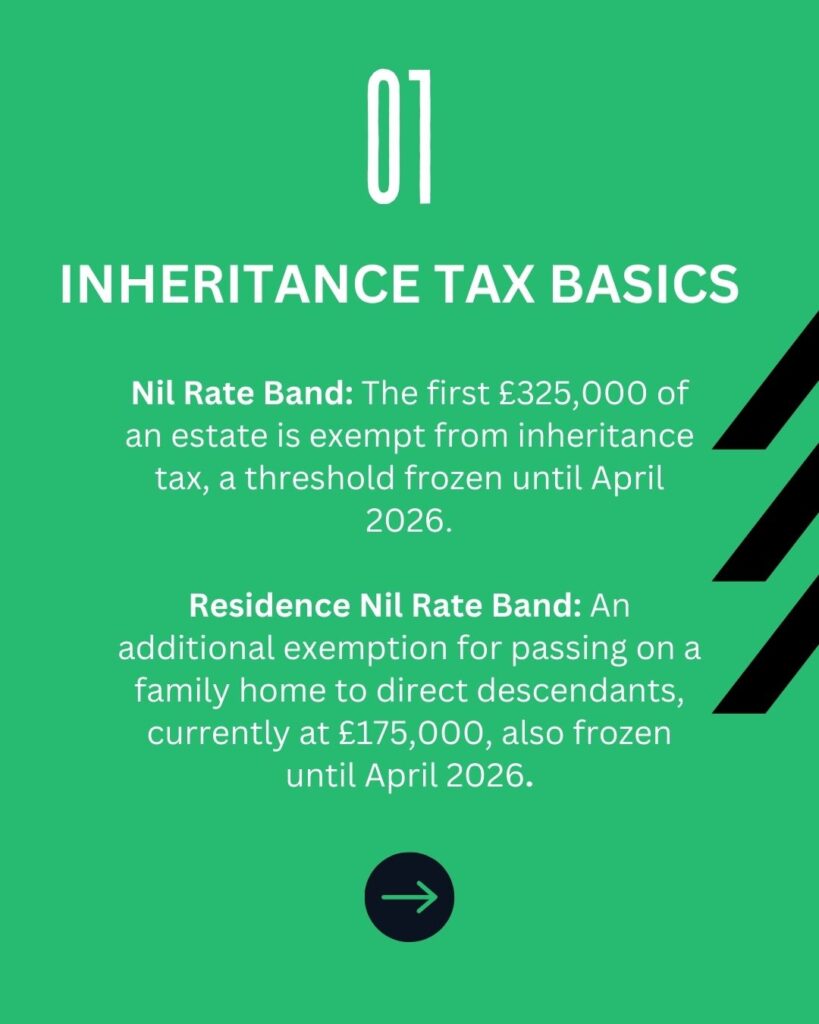

The inheritance tax nil rate band has been frozen at its current level of £325,000 since 6th April 2009. The nil rate band is the amount of your estate that is exempt from inheritance tax.

It will remain at its current level of £325,000 until 5th April 2026 – a 17-year freeze! However, since 6th April 2017, a new additional nil rate band has been available for the ‘family home’.

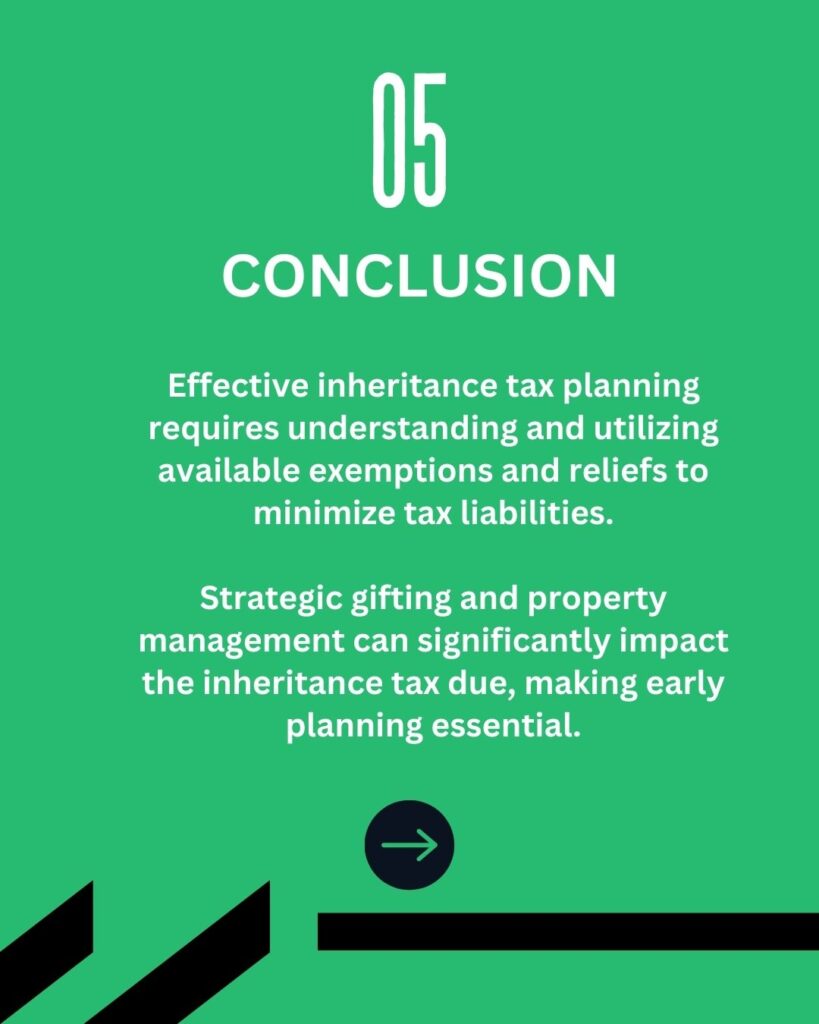

Generally speaking, effective inheritance tax planning should be carried out on a long-term basis. However, it is worth remembering the following points, which should be considered on an annual basis.

Annual exemption

The first £3,000 of gifts made by any individual during each tax year is completely exempt for inheritance tax. In addition to this, if the previous year’s annual exemption was not fully utilised, it can be carried forward into the following (current) tax year.

This means, in one tax year you are able to have up to £6000 of gifts that will be exempt from any tax only if you have not made any gifts during the previous tax year.

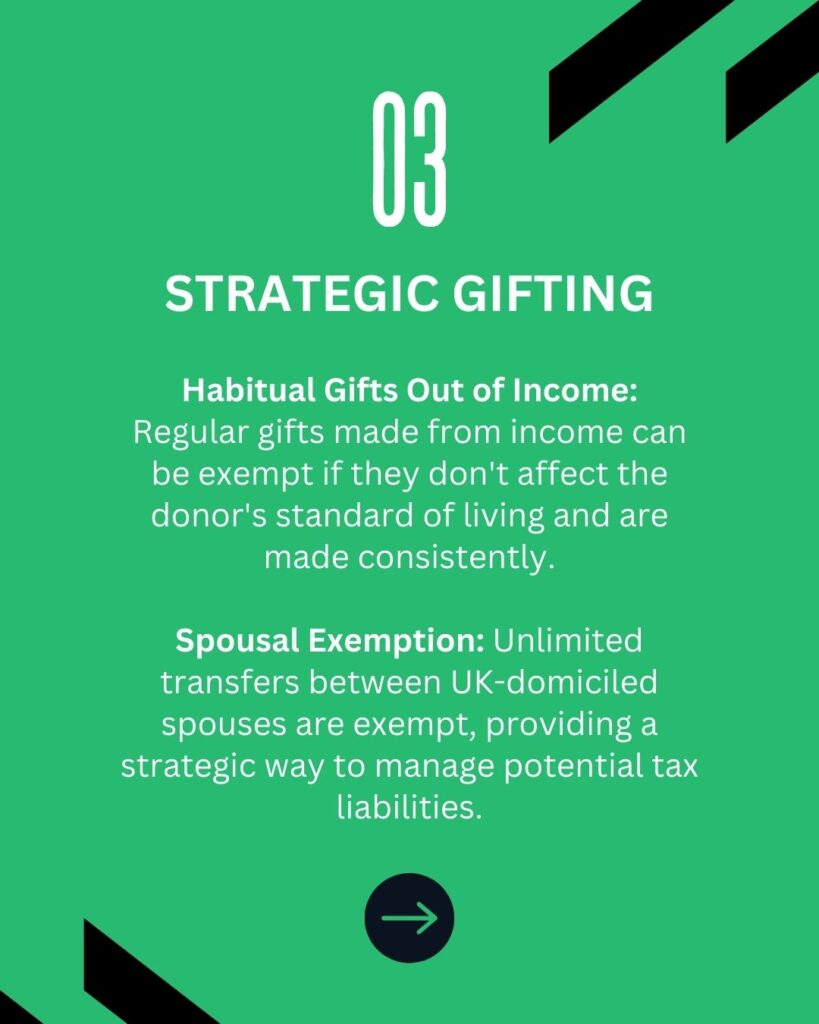

This exemption is specific to a per person basis, so married couples can also make gifts of £3,000 each.

Small Gifts Exemption

Gifts of up to £250 per tax year made to any one individual are also exempt from any inheritance tax and do not count towards the annual exemption. These types of small gifts are an exemption for you as you can make as many of these gifts as you like to different people.

However, the annual exemption cannot be used for further gifts to the same recipient in the same tax year.

Habitual Gifts Out of Income

Habitual gifts out of income are an exemption from inheritance tax, in order for these gifts to be classed as ‘habitual’, they need to be made consistently for a number of years. Which is why it is important to remember to keep these up every tax year.

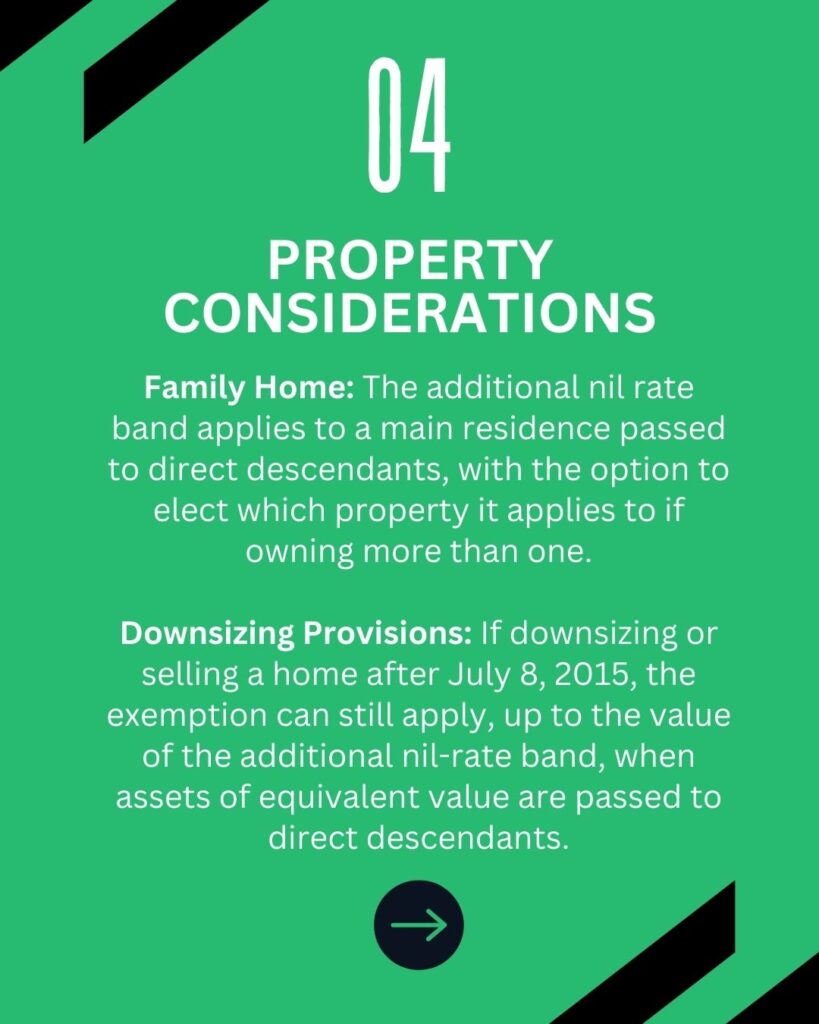

The Family Home

An additional nil rate band is available for the ‘family home’ for any deaths occurring after 6 April 2017. This exemption is only available on a property which has been the deceased residence at some point during their life. If the deceased has passed while owning more than one or multiple qualifying properties, the personal electives can elect which property this exemption should apply to.

The exemption is only applied once the property is passed. This is usually done to a direct descendant of the deceased and in this case, any stepchildren, foster children or adopted children are all accorded the same status as one another for this sole purpose.

Similar to the £325,000 nil rate band, any unused proportion of the exemption will pass to the deceased’s partner or spouse.

When a person downsizes or ceases to own a home after 8 July 2015, the residence nil rate band is available to them as well as assets of an equivalent value, up to the value of the additional nil-rate band, are passed to direct descendants.

The residence nil-rate band that was introduced in 2017/18 and increased from £100,000 to its current value to £175,000. This level is set to remain until 5 April 2026.

Margaret divorced her husband many years before her death in June 2021.

She leaves her estate, worth £600,000, to her daughter.

Margaret’s estate includes her former home, which is worth £250,000 at the time of her death. The residence nil rate band available for 2021/22 exempts £175,000 of the value of Margaret’s former home. This reduces her taxable estate to £425,000 before deduction of her main nil rate band of £325,000, which reduces it to £100,000.

The IHT payable on Margaret’s estate at 40% is thus £40,000. The residence nil rate band is withdrawn from estates worth in excess of £2 million (this threshold is also frozen until 5th April 2026).

This withdrawal is at the rate of £1 for every £2 by which the estate exceeds £2 million. Any mortgages or other loans secured over a property will have to be taken into account when allocating the exemption. For example, where the deceased held a property worth £250,000 which was subject to a mortgage of £180,000, the exemption will be limited to just £70,000.

Further Information on Accounts & Tax

Our team of specialist accountants and tax experts can help manage, process and structure your business’s finances. From management accounts and payroll & pensions to tax planning and cash flow management, we can take care of the full back-office function of your business.

Book a free, no-obligation consultation with one of the team to find out how we can make your accounts & tax easier, quicker and cheaper.

Make sure you never miss any of our articles, webinars, videos or events by following us on Facebook, LinkedIn, YouTube and Instagram.

Reviewed By:

Arun Mehra

Samera CEO

Arun, CEO of Samera, is an experienced accountant and dental practice owner. He specialises in accountancy, financial directorship, squat practices and practice management.

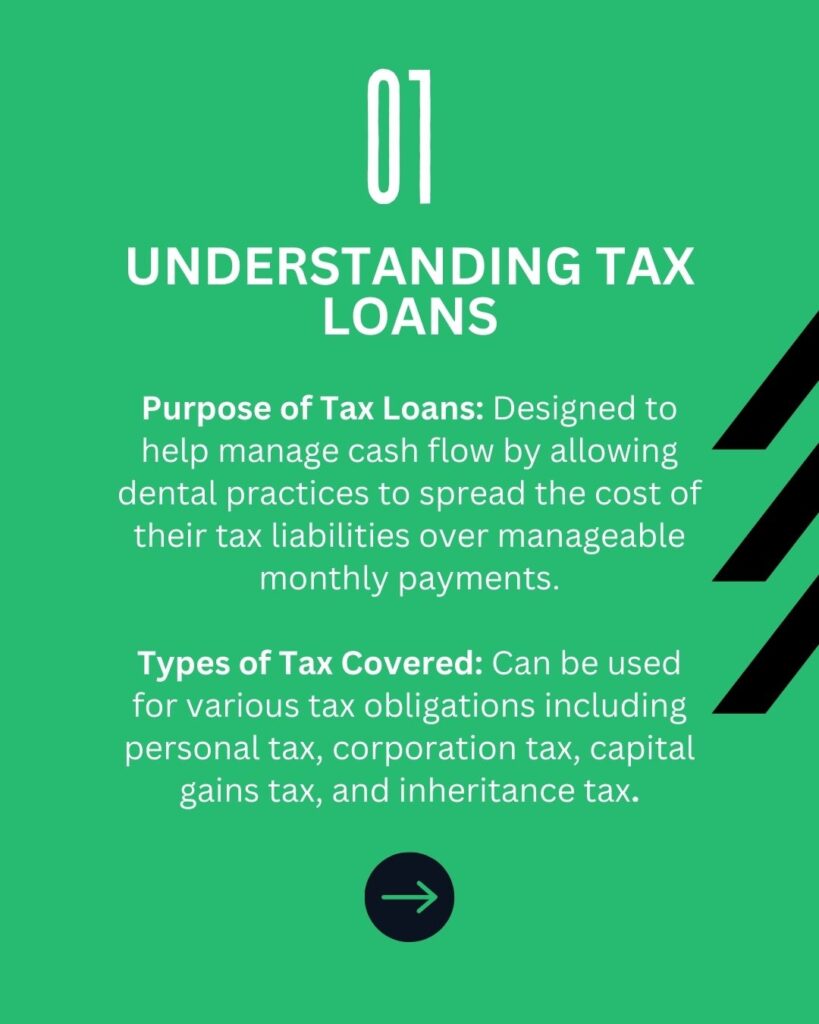

Tax bills are a recurring expense for all businesses including dental practices that can often take their toll. This is where tax loans come in and help manage this overbearing expense by helping you take control of your cash flow. They also help ease the costs of taxes by spreading the costs of your tax bill into manageable monthly payments.

The amount of taxation that a business incurs is based on current tax laws that determines their tax liability. Tax liability is the amount of tax debt owed by an individual, business, corporation or any other entity. Tax liabilities are therefore incurred from earning any income from a business, a gain on the sale of an asset, estate or other taxable events.

When a business’s tax liability is due, as a dental practice, they have to ensure that they have enough cash flow at hand to meet the demand of the tax laws in place. Unfortunately owing tax isn’t an easy debt to get out of. A tax bill cannot be put off until the business itself pays the bill. HMRC do not hesitate in issuing penalties for late or non payments. The tax rules are very strict and failure to adhere to them can become very costly for you and your business.

In some instances, late penalties are one of the more tranquil consequences that the HMRC gives out. Penalties for late payment or non payment can have very bad consequences on your business. If you default on your payments for a very long time, the interest of your tax bill increases and so does your fines. This could lead to you having to liquidate a company in its entirety or its assets in order to fully pay HMRC what is owed through your tax liabilities.

It is normal for a business’s cash flow to fluctuate over the different seasons, however, it is imperative that funds are put aside in order to meet tax obligations. However, this is often not always the case. The cash flow may not always be there and unforeseen circumstances do occur to hinder you from being able to pay your taxes. This is where tax loans come in handy for businesses.

VAT and corporation tax payments come around regularly but they can still be a problem if your business does not have sufficient funds. Tax loans are designed to help manage your cash flow. Tax loans can fund personal tax, corporation, capital gains, inheritance tax amongst other overbearing tax bills you may incur. Tax loans allow you to spread the cost of your tax demand into more affordable monthly payments, allowing you to pay your tax bill comfortably.

When quarterly VAT payments are looming for your dental practice and there is limited cash in the business to secure paying this bill, access to additional finance is very useful.

VAT funding enables businesses to pay your quarterly VAT payments over the course of an agreed term (usually 12 months). This will be paid back over a series of monthly payments. This loan provides the liquid funds needed for businesses to settle their VAT bill without provoking any consequences from HMRC. Obtaining this loan will boost the company’s overall cash flow position as well as pay your VAT bills smoothly.

As a business owner, there are a few things that may be worrisome for you. Owing the government funds can unfortunately often be part of that worry. A lot of business owners are not aware of the options that are available to them when they do not have enough working capital to pay the necessary bills.

Businesses try to optimise their profits and strive to have working capital to reinvest and take advantage of business opportunities. For this reason, tax loans are becoming increasingly popular. These loans allow businesses to free up cash flow while meeting the demands of HMRC on time.

Forfeiting a tax payment or paying late is something you must try to avoid at all costs. Owing a debt to the HMRC is not something to be taken lightly. Often those who default on their tax payments are dealt with enforcement actions being taken against them.

Regardless of what your business is, taking out a tax loan can be the financial solution that you need as it will enable you to spread out the cost of your tax bill over the course of a 6-12 month term helping businesses navigate through the costs of tax while avoiding the wrath of HMRC and racking up late payment charges.

Why are tax loans useful?

Tax loans are incredibly helpful and convenient to help pay your tax bill on time. On the one hand, it is in your best interest to stay within HMRC’s good graces by paying all your tax bills on time while on the other, you also want to leave yourself available cash for the essential day to day running of your business. Tax loans help you do both, very comfortably.

Many lenders design your loan specific to your needs, there are loans that are specifically designed to pay tax bills. In some cases, funding a VAT bill can have tax benefits. This is because interest payments are often offset against corporation tax later in the financial year.

Benefits of tax loans

Improved cash flow as well as control of cash flow

Easy, fixed monthly repayments

Flexible repayment terms

Easy quick and simple to arrange

HMRC receive payments directly and on time

Protects existing bank facilities

Keeps your bank funding lines open

Fixed rates

Fast decisions and fast funding

Personal service and dedicated account manager

Many tax loan facilities operate in ways to enable you to receive the funds you need in a simple and timely manner. The main benefits tax loans have to businesses is that this loan will allow their cash flow to remain in their control, lift the weight of their tax bills by spreading out the costs into manageable monthly payments and avoiding any late payment consequences.

How do I apply for tax bill funding?

As a dental business owner, VAT or tax payments can be detrimental to your business profits. Time constraints are very common, especially when it comes closer to the time to pay your tax bills. This is why the process of applying for funding is quite quick and simple.

Unlike many other loans, detailed business plans and security assets are not needed, nor is it necessary to make long winded appointments to discuss the security of your loan. Many processes are flexible and quick with great affordability and transparency.

Tax refund

Loan against tax refund

Taking out a loan against your tax refund is also known as a refund-advance loan. It is a type of secured loan. This means that you need to put up something in this loan to use as collateral. Usually this would mean an asset or an estate but in this case collateral refers to your anticipated tax refund.

Tax refund loans are short term loans that must be repaid when you receive your tax refund. You will often receive this loan as a deposit into your bank account . When you get your tax refunded, it will be deposited into that same bank account and the loan amount will be deducted from the amount given. Interest and other fees will also be deducted from the amount of tax refund given to you.

Pros and cons of tax refunded loans

Here are a few things to consider before you take out a tax-refund loan.

Pros of tax-refunded loans

Fast funding

When you apply and are approved for a ta-refund loan, the funds are available to you as little as 24 hours after you are approved. Usually the time it takes from your tax to actually be refunded to you is a minimum 21 days.

Cons of tax-refunded loans

Fees

Unfortunately getting a tax refund loan may often involve paying interest on said loan. This is not the case with all tax refund loans, there are some lenders that are able to give you an interest free loan. However, even with an interest free loan, there still may be fees you will need to pay, for example, administrative fees that are associated with transferring your refund.

High risk

There are potential risks with this kind of refund loan. The key risk being that the amount of the loan is based on how much you anticipate getting back in the refund. This may not accurately represent how much your tax refund will actually be. There are several factors that could impact that amount you are expected to receive and the actual amount you are given.

An example of this is that if you owe a state debt such as a student loan or back taxes. These debts will be taken from your tax, therefore, your tax refund will be reduced. This will result in you receiving less funds than you had anticipated when taking out the loan.

Tax refund loans

While tax refund advance loans can be a helpful and timely option to get the quick cash flow you need, there are many factors you must keep in mind before you decide to apply for this type of loan.

If you do decide to apply for a tax-refund advance here are a few things we advise:

Proceed with caution:

These loans can often come with a high interest rate and hidden fees.

Read the terms and conditions carefully:

To allow yourself to make the most out of this loan, you must ensure that you fully understand the terms and conditions of the loan and all the costs in their entirety. This includes any contractually included late fees or any prepaid card costs associated with the loan.

Corporation tax is the one of the most important taxes your business, however large or small, will pay. If you are unable to pay your corporation tax bill, you will be hit with penalty charges which will increase the longer you default on your payment and will exceed the overall amount you originally owed, fundamentally resulting in you being in a worse financial situation.

Charges begin from the day your payment is late, the interest of the lay payment will also continue to rack up over time so it is important to meet your payment deadlines.

If you are unable to pay your tax bill because the time for paying your taxes has come at a very inconvenient time for you, then a corporation tax loan would be ideal for your situation. It is an effective way to spread your tax demands across monthly repayments that are affordable for you.

What is corporation tax?

Corporation tax is a tax that all limited companies must pay. It is a tax that is payable against the profits the company makes. A corporation tax bill is based on the level of income a business has earnt through trading. It is the income derived from taxable events throughout the tax year such as asset sales. You are liable to pay corporation tax if your business is a member’s only club, a trade association, a limited company, a trade or housing association, or a group of individuals outside a partnership operating as a business.

The current rate in the UK for corporation tax is 20%. This also applies to any companies you may have overseas but have an office or branch residing in the UK. HMRC usually calculates your corporation tax bill roughly 9 months after the business accounting year comes to an end.

If your tax liabilities are not paid on time, similar to your business tax expenses, there will be penalties issued by HMRC. If your tax bill is quite high, the business itself could be forced to liquidate completely in order to pay your tax bill. The real truth for many businesses is that they sometimes simply are not in a position to be able to pay their bill which is why corporation tax bills can be very useful. It is important to note that HMRC will not send reminders about your tax bill until you are overdue.

This is a difficult situation to be in, especially if your current available capital does not allow you to meet the demanded amount of the corporation tax bill. Ideally, the best option is to set aside funds during the year to meet your tax bill however, It is normal for cash flow to fluctuate over the year based on different activities. This makes it hard to put a large amount of money aside especially when you have unexpected costs to pay. This is why corporation loans are becoming increasingly popular to help regulate cash flow and pay for a business’s tax bill.

Who pays corporation tax?

All limited companies are liable for corporation tax. The tax is also aligned to the financial year of the business. However, there are a few exceptions such as when a new business changes its year end accounting date.

Businesses are bound to pay taxes on any profits the business makes in its financial year. Corporation tax is also due on any money the business makes from investments and any chargeable gains.

Benefits of a corporation tax loan

Corporation tax loans improve a businesses cash flow which is why they are increasing immensely in popularity amongst many different types of businesses. This added stable cash flow allows businesses to take advantage of this added capital to their business to fund unexpected costs or any drops in income.

A major benefit of a corporation taking a loan is the added cash flow to your business. The loan also helps avoid the risk of high and very costly charges for late or non payment of your taxes. The loan itself will improve the flow of your capital, this means that when your next corporation tax loan is due, you will be in a much better position to comfortably pay the bill.

Regardless of the type of business you operate, it is possible for you to qualify to apply and receive a corporation tax loan. The loans have various options that are flexible for you and they will enable you to spread your tax bill over the course of several months. You will have fixed monthly or quarterly payments to repay your loan.

There are a variety of lenders who specialise in commercial finance loans. They are able to design a plan that is flexible and suited to your specific repayment abilities to ensure that you will be able to pay your tax bill comfortably with monthly installments.

Using corporation tax funding allows businesses to avoid the potentially costly HMRC penalties for late or non payments. You can usually get a decision on your corporation tax loan inquiry within as little as 24 hours in most cases.

Where to apply for a corporation tax loan

There are a number of lenders who specialise in finance loans specific to paying tax such as corporation tax loans, which gives you many options to choose from. There are various online comparison tools that will be perfectly aligned to the needs of your business. These comparison tools and websites will also help you filter through different loans that are best suited to you with the lowest interest rates.

We’ve been helping to fund the future of British healthcare businesses for over 20 years and our team are made up of former bankers with decades of experience in the UK’s healthcare lending sector.

You can find out more about working with Samera and the financial services we offer by booking a free consultation with one of the Samera team at a time that suits you (including evenings) or by reading more about our financial services at the links below.

Make sure you never miss any of our articles, webinars, videos or events by following us on Facebook, LinkedIn, YouTube and Instagram.

Reviewed By:

Nigel Crossman

Head of Commercial Finance

Nigel is a former banker and head of commercial finance at Samera. He specialises in raising finance, negotiating deals and structuring finance applications for healthcare businesses.

Dan Fearon

Finance Manager

Dan is a former banker and the head of our dental practice sales team. He specialises in asset finance for healthcare businesses and dental practice sales.

Bridging loans are a short term financing option that are quite different from a standard bank loan. They are often used by property buyers to essentially ‘bridge’ the financial gap between the sale of their current home and the final sale of their next property investment. However, these loans can be very helpful in many ways for businesses to use immediate funds to obtain quick capital for their dental practice, integrate cash flow or make necessary refurbishments. They are one of the most useful and viable options when you need to move quickly to buy a property.

Bridging loans are usually offered between 1-18 months, with the loan repayable in full at the end of the term. An open bridging loan does not have a repayment date, but will still be a short term loan. For example, a 12 month bridging loan must be repaid on the 12th month or before the 12 month period ends. It is in your interest to repay the loan as early as possible in order to save on interest payments.

Bridging loans are very easily accessible and immediate financing which means that they typically have high interest rates and fees.

What is Bridging Finance?

Bridging finance is a kind of commercial property finance which is usually used by companies and sole traders to quickly fund the purchase of a property. Traditional commercial mortgages often take months to arrange. Bridging finance companies can lend money much faster. This type of funding allows clients to obtain immediate funds to complete the purchase of a property or to bridge the gap between selling and buying a new estate. The loan will usually be secured against a charge of the property you are purchasing.

How Much Can I borrow with a Bridging Loan?

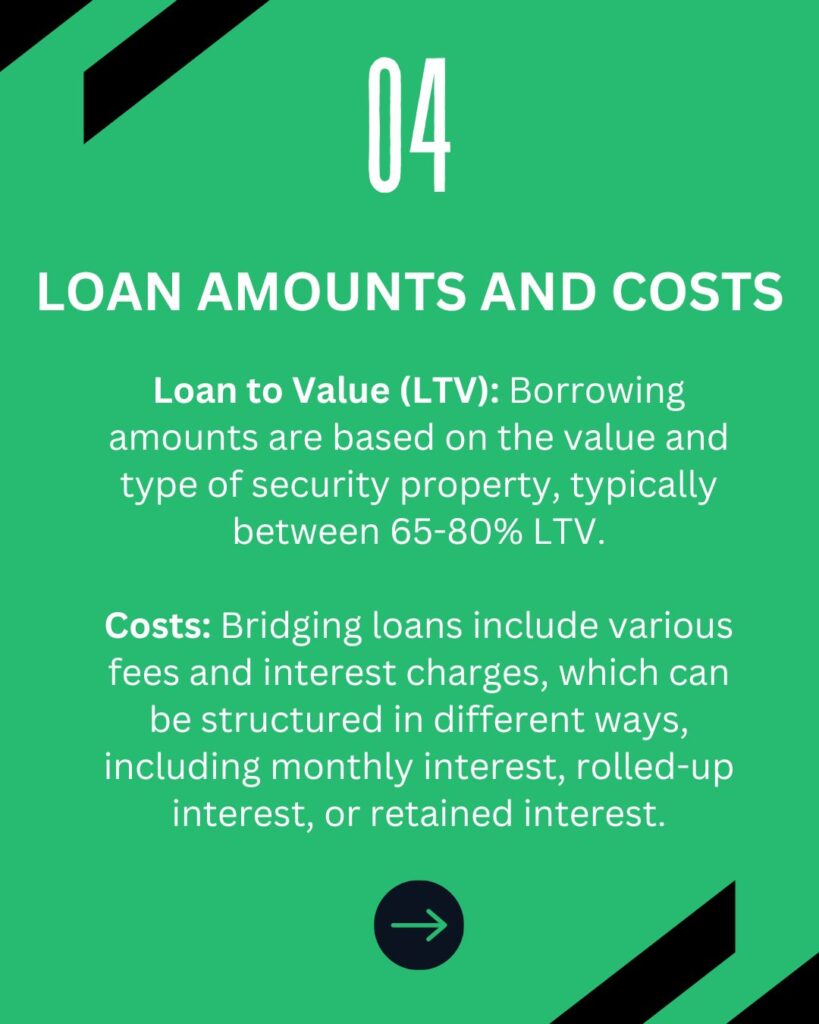

The amount that you can borrow is solely dependent on the value and the type of security property that you use. Bridging lenders will quote a maximum loan to value (LTV), this is usually between 65-80%. You are able to get a bigger loan depending on your exit strategy.

Bridging loans are only meant for short term periods, so attempting to get a very large amount of money through a bridging loan without an adequate exit strategy is quite unlikely.

Why is Bridging Finance Useful?

Bridging finance is useful for dental practice businesses because it is a loan option that is fast and flexible. This short term property loan option can be approved and released so quickly that it could be done in a matter of days. In many cases, this is a very valuable asset to obtain in the property industry.

These loans are a highly useful tool for businesses to bridge the gap between two property transactions. Bridging loans are a practical solution for those who need extra time to sustain suitable long term finance.

Bridge capital is temporary funding that helps businesses cover its costs until it can get permanent capital. The repayment terms for bridge capital vary on the individual, but usually payment is made in full when the loan reaches the end of the term. Usually, by this time, the company receives the necessary capital from their investment or a longer term loan. Bridging loans are typically secured on any real estate asset a borrower can offer. This can include commercial or mixed-use properties.

How do I get a Bridging Loan?

Bridging loans are not widely available and are not offered by a lot of high street banks. Bridging loans are usually highly available from mortgage brokers and advisers.

Although bridging loans are generally quicker to arrange than a mortgage, do not make the mistake that they are easier because lenders are less thorough. Lenders still make thorough checks of your current finances, the value or your perspective property and your current home.

How Much do Bridging Loans Cost?

Bridging loans can end up being very expensive because they charge you a range of fees as well as interest. You will be charged monthly interest on your loan. Your lender will not quote the annual percentage rate (APR) as most bridging loans do not even last a whole year.

You will be charged interest on your loan in 1 of 3 ways:

Monthly interest: This is the most common way interest will be added to your loan. You will pay the interest each month, and it will not be added to the balance of your loan. You will pay off the full balance at the end of the term.

Rolled up interest: This is when you pay all of the interest including your original loan, at the end of the term. The interest will be added each month and accumulated this way, however you will just pay the full amount when your term comes to an end.

Retained interest: Your lender will calculate the amount of interest you will have to pay over the time-frame of your term when you first take out your loan. You will borrow the interest amount from the bridging lender when you apply for your loan including your initial figure. This will cover the monthly interest payments for a set period. You will then pay the loan back and the end of the term including the extra money borrowed for interest payments.

Exit Strategies for Bridging Loans

An exit strategy is the term used to explain how the bridging loan will be repaid at the end of the term. A strong exit strategy is a vital part of any bridging loan application. It is having a strong exit strategy that makes the process of the loan application faster and lenders to be more flexible with your requests.

Why is an Exit Strategy Important?

Having a preplanned and strong exit strategy is very important on a bridging finance provider’s checklist. These loans are based on an interest only basis. How you plan to settle the end of your loan at the end of its term is the most crucial part of your loan.

When your term has come to an end, your lender will expect your loan to be paid back in full as agreed. In the case that you are unable to do this, your account will then be put into default. If this happens it could affect your credit record. In order to avoid this situation you will need to resolve the situation as quickly as possible.

Here are a few options for you:

Extend your loan with your lender. This may mean that you will continue to add interest on your current loan if you are near your maximum loan to value. It is also important to note that your lender may not agree to renew the loan. If they do agree, they may charge a higher interest rate in exchange for the renewal.

Refinance to a new lender. This option could get very expensive for you as you will have to restart the process and pay all setup costs again.

Remember that if you do refinance your loan, you still need to consider what your exit plan is for your new loan. Refinancing blindly is a temporary solution, you will just be delaying the inevitable unless you plan a way to properly pay back the loan.

What if I can’t Pay Back the Loan by the End of the Agreed Term?

Bridge loans in their nature are arranged for short term requirements and the lender expects all clients to contractually abide by the terms of repayment within the set time frame agreed.

Bridge loans, like many other loans, are set up with a set plan to arrange how the loan will be repaid. Usually, the lender will not allow the loan to proceed if there are any hesitations about your ability to repay the loan.

When you hit the end of your term, you are expected to repay the loan in full. Acceptable exit methods are usually sale of property or refinance. There are a range of different exit strategies that may work for you.

Loans are a contractual agreement, however, it is inevitable that some loans will overrun the agreed term. The lender will often contact you (the borrower) at least 3 months prior to the end of the agreed term to examine how things are going for you and determine whether you will be able to pay back the loan in time of the agreed term. If the lender believes that it is not likely, they will usually recommend other steps that you can take to ensure that you can get back on track and eventually, you will be able to fully repay your loan.

The lender will obviously want the loan repaid as and when agreed but they will normally work with borrowers who have over run their term only if the borrower is open about their situation and is in continuous regular contact with the lender. This way you and your lender are able to work out a plan to get you back on track together.

We always recommend that when taking out a bridging loan, you opt for the longest term available as many plans can over run the expected timeframe.

How Long Can I Take Out a Bridging Loan for?

The average term for a bridging loan is approximately 6-7 months. In different circumstances, longer terms can be discussed and arranged. It is often dependent on how much your loan is for that your term can be extended.

Are Bridging Loans Regulated?

A bridging loan becomes ‘regulated’ when the loan is secured against a property that is or will be occupied by the borrower. A regulated loan can be secured by a first or second charge, the bridging loan will be regulated by the FCA.

Bridging loans that are unregulated are usually associated with commercial buy-to-let properties.

Can I Get a Bridging Loan Without a Credit Check?

No. Like most other loans, bridging finance involves a thorough check into the finances of the borrower.

Applicants with clean credit history are often more attractive to lenders which results in these applicants receiving favourable rates. However, good credit is not only what lenders look for. There are other aspects and details of your loan that will help you get approved by your lender even though you may have a bad credit history.

Can I Still Get a Bridging Loan if I Have Credit Issues?

Although thorough checks into your credit history will be taken before you take out your loan, bridging loans can still be available to you even if you have a poor credit rating. Your bridging finance is often determined by the security of the property being offered as well as the exit route. Your lender will also take into account the size of your deposit and the assets you put up as security.

A lender’s biggest concern is that having poor credit history will prevent you from repaying the loan at the end of the term. It is highly dependent on what you put up as security and what your exit strategy is. If you have a strong exit strategy such as, to sell the property or another estate, then there is a lesser chance to have an impact on you taking out the loan.

Closed-Bridge and Open-Bridge Loans

What is a closed bridging loan?

A closed bridge loan is for people who have set a fixed date to repay the loan. A closed bridging loan includes a feasible exit strategy as part of the lender’s application. If you are able to produce proof to your lender that you are able to repay the debt as soon as your transaction is completed, then a closed bridging loan is the most effective and sensible option for you. They are defined by the set repayment date and are the most common type of bridging finance option available. Closed loans are usually offered with lower interest rates and have the highest rates of approval.

What is an Open Bridging Loan?

An open-bridging loan differs from a closed bridging loan as an open loan does not require a clearly defined exit route in place to provide to the lender.

Due to the unpredictable nature of repaying an open bridging loan, they are a lot harder to arrange. However, if this is your preferred loan type, it would be in your best interest to be able to provide enough security, so that it is more likely that you are able to be approved for this type of finance.

What is the Interest Rate on a Bridge Loan?

The interest rate on a bridge loan is generally between 1% and 1.5% per month. That being said, there are some lenders who have better rates than others. Because of this, it is always useful to shop around or use the services of brokers in order to get the best possible deal for your loan.

How Much Can I Borrow for a Bridging Loan?

You are usually able to borrow from 80% – 100% of the property value purchase price with bridging loans. It is important to understand that all lenders are different and have different terms. If you are looking to borrow more, you may need to offer additional security in the form of an additional property or several other properties.

There are four main factors that will impact the cost of your loan and they are:

The term of your loan

The amount borrowed

The lenders agreed interest rate

Start up fees

The general trend with bridging loans is that your costs will generally increase the longer your term is. This is also the case the larger your loan is.

To minimise the cost of your loan, it will help your expenses if you compare the total cost of borrowing the funds, not simply the interest rate and arrangement fees on their own.

There are many fees that are charged in addition to the interest and arrangement fee. Different lenders include their own fees. Here are some common fees charged in addition to your interest rates.

Exit fees These exit fees are payable on repayment of the loan. There are some lenders that do not charge an exit fee where some others charge from 1 to -1% month’s interest.

Valuation fees These fees are payable for surveyor’s costs in order to ensure your property is suitable security. Some lenders do not require a valuation.

Legal fees These fees are to pay lenders own legal costs while they are setting up the loan.

Admin fees These can also be labelled as asset management fees. These are costs that are payable to the lender as they handle the setup of your loan.

Pros and cons of Bridging loans

Pros of Bridging Loans:

Bridging finance is quick to arrange. Applications can be completed and authorised quickly allowing you to obtain the funds you need quicker than you could with any other type of loan. Many property deals are highly dependent on factors that are rapidly changing within the business. Being able to obtain funds quickly can be a major attraction.

Bridging loans allow you to complete a property transaction that would otherwise not be possible.

You are able to get funds up to 100%. Usually the most you are able to borrow is 80%, however, provided the security put in place is sufficient, lenders will allow you to borrow up to 100%.

Often with bridging loans there are no monthly repayments, this allows the loan to raise capital for your business where cash flow is tight, while you have assets that can pay back the loan.

Cons of Bridging Loans

Your home / property you put up as security is at risk if you do not keep up repayments on a bridging loan.

There are usually several fees which you will have to pay which makes bridging loans more expensive than traditional mortgages. These fees include an arrangement fee, broker fees, valuations fees and sometimes even legal fees, before you are able to take out your loan. If you are borrowing for a long period of time, the interest charges are a lot more expensive than a standard loan.

As most loans are short term, if you have issues with your repayment method, you could potentially face major issues. Failure to repay your loan at the end of the term could have major repercussions. It could lead to your property being repossessed.

When Would you Need a Bridging Loan?

When a buyer pulls out on an investment into your property, your finances on the offer of your next home and potential deposits could be put in jeopardy. A bridging loan will be able to tide you over until your home is back on the market and is under offer again.

Bridging finance allows you to buy a second property before selling the first.

As long as you can provide your lender a valid exit strategy, the money you obtain for a bridging loan can be used for a variety of business reasons from providing your business with working capital to covering cash flow issues.

Auctions: Bridging loans allow you immediate funds when you are bidding for properties at an auction.

Bridging loans could also be used if you wanted to buy a property with a short lease. You could use the loan to buy the property, then add value by extending the lease. This would also provide a valid exit strategy.

Refurbishment projects: You can use residential bridging loans for cash flow to refurbish a property before full capital is available.

What is a Commercial Bridging Loan?

Commercial bridging loans are similar to residential bridging loans, they are used when there is a gap in financing that needs to be filled quickly.

For a commercial bridging loan, the overall use of the property has to be more than 40% commercial. This means that retail units with residential flats on top or at the back have to occupy more than 40% commercial space of the property.

The exit strategy for residential bridging loans usually include landlord or landlord companies to refinance the loan into a buy-to-let mortgage. This is usually done after the loan is used for renovations to make the property more attractive or suitable for rental.

For commercial units that are bought specifically by using a commercial bridging loan, the exit strategy usually involves selling or refinancing the property on to a conventional commercial mortgage after buying or refurbishing the property.

What is a Bridge-to-let Loan?

This type of bridging loan is specifically aimed at the buy-to-let market. The loan is used to secure a property that is fully intended to rent out without having a basic mortgage organised. This loan would be based around your ability to obtain 100% rental income. This means that your potential rental income should equal your payments.

You can use this type of bridge loan for both residential and commercial properties. The exit strategy would be to refinance the property on to a conventila buy-to-let mortgage and gaining capital by renting the property out either in part or fully.

With all bridging finance, you have to put up security therefore, defaulting on your loan will not only affect your credit score, but will also put your asset at serious risk. Even though bridging loans are able to be authorised quickly, all lenders are very thorough with background checks and legal rights.

There are a variety of legal options your lender has at their disposal in order to compel you to pay what is owed to them. This not only includes the right to your security asset but could also include county court judgments, or statutory demand letters which would ultimately force your company into liquidation.

Breaching the Terms of your Bridging Loan

Bridging loans have many terms and conditions that are different to standard mortgage loans. A lot of lenders are at liberty to insert their own terms and conditions which is why it is imperative to read the fine print carefully before signing all contracts to understand the fees, repayments, charges and when they are all due.

We’ve been helping to fund the future of British healthcare businesses for over 20 years and our team are made up of former bankers with decades of experience in the UK’s healthcare lending sector.

You can find out more about working with Samera and the financial services we offer by booking a free consultation with one of the Samera team at a time that suits you (including evenings) or by reading more about our financial services at the links below.

Make sure you never miss any of our articles, webinars, videos or events by following us on Facebook, LinkedIn, YouTube and Instagram.

Reviewed By:

Nigel Crossman

Head of Commercial Finance

Nigel is a former banker and head of commercial finance at Samera. He specialises in raising finance, negotiating deals and structuring finance applications for healthcare businesses.

Dan Fearon

Finance Manager

Dan is a former banker and the head of our dental practice sales team. He specialises in asset finance for healthcare businesses and dental practice sales.

Working capital is the amount of available money a business has at its disposal for its day-to-day operations and expenses. Working capital is not the same as the overall value of your dental practice. It is not calculated by adding up everything the business owns.

Working capital is the cash or cash equivalents your dental practice has, or can raise in a year. Working capital is calculated by subtracting the value of the business’s liabilities from its assets. It is essentially the amount of money left over once a practice pays all its standing debts.

If your dental practice is unable to meet its debts with your existing assets, you may need to apply for working capital finance.

Working capital reflects the short-term financial health of your dental practice, as well as its ability to conduct regular operations. Without adequate working capital, your practice will be unable to meet its everyday obligations.

For instance, staffing costs, rent on the premises, marketing and taxes should all be covered by the business’s available cash – its working capital. Ant given business should not need to sell off long-term assets or borrow money to meet these responsibilities. Its ability to do so is dictated by the amount of working capital.

Working capital represents the liquid cash which isn’t tied up in its long-term assets.

The most common definition is; the difference between the business’s current assets and its current liabilities.

Working capital vs cash flow

Although they are similar, related concepts and are often confused, working capital and cash flow are not quite the same thing.

Your dental practice’s cash flow is the amount of cash that moves through the business over any given period. It is the amount of money that your business can generate. Cash flow does not take into account your liabilities. Working capital, on the other hand, takes into account all your current liabilities, as well as current assets.

A working capital ratio is a representation of the financial health of your dental practice as a business overall. It is a broad picture of your business’s ability to pay off debt in the short-term. Cash flow is more concerned with the cash that can be generated. This means you could have a weak working capital but a strong cash flow. Your business is generating a lot of money, you just owe nearly as much as you make.

Therefore, even with a strong cash flow, low working capital can make it difficult to pay your debts off on time. If this is the case, you may benefit from raising working capital finance.

How to Calculate Working Capital.

Working capital is the amount left over once your dental practice has met all of its financial obligations. Working capital can be calculated with one fairly simple equation.

That equation is: current assets minus current liabilities equals working capital.

The number left over is the amount of ready cash that a business could feasibly spend without having to sell off long-term assets or borrow money from a financial institution. It can often simply be the value of the entire inventory of your dental practice added to the current bank holdings.

For example, lets say your business has £10,000 in a business bank account, a customer owes £1,000 and the business’s inventory totals £10,000. Your business has current assets totalling £21,000.

Let us also assume that the business owes £15,000 in total, spread across suppliers, debts and tax bills.

Once the business has paid off its £15,000 current liabilities from its £21,000 in current assets, there is £6,000 left over as working capital. Although the business could raise more money by selling off more long-term assets, this £6,000 is the amount it can liquidise within a 12 month period. Therefore, the entire dental practice has a working capital worth £6,000.

Current Assets

Current Assets vs Fixed or Long-term Assets

Current assets are not to be confused with the long-term assets of a business. Long-term assets are the assets that your dental practice will expect to keep for longer than 12 months, which could include a lot of necessary dental equipment. They are essential parts of the business that cannot just be sold off to pay the tax bill. They also include assets that cannot be sold off for liquid cash in a year.

They are sometimes known as fixed assets.

Although a piece of heavy machinery or a company car is an asset to the business, it is not included as a current asset in the working capital calculation as it cannot be quickly sold off for cash. It would also disrupt the day-to-day business operations to do so.

Long term assets include items such as land & property, machinery & vehicles and intangible, soft assets such as copyrights and patents. Inventory will usually be included as a current asset, since it can often be expected to be sold in 12 months. However, heavier pieces of inventory may not be included and will have to be judged individually.

Current assets, on the other hand, are the assets which can be, or will be expected to be, sold off or otherwise liquidised within a 12 month period.

Examples of current assets include:

Cash and bank balance

Most businesses have some form of account with a bank or similar financial institution. Most also have some form of ready cash available. This could range from a small petty-cash stash in the office to a locked safe containing thousands of pounds. These are immediate, liquid cash which can be instantly used to fund business operations.

Inventory

Certain pieces of inventory are often considered current assets. Whether inventory items will be listed as a current asset or not depends on whether it can be sold off for liquid cash within a 12 month period (or before the end of the business cycle).

For instance, a warehouse full of food can be reasonably expected to be sold within a 12 month period. Therefore, it is a current asset, since within a year you know that your business will exchange those foodstuffs for liquid cash.

However, the heavy machinery that the business used to process or harvest that food may not be expected to be sold off within that same 12 month period. Therefore, it would usually not be included as a current asset. Likewise, the property your business owns may be its most valuable long-term asset. However, you are not going to sell it off to pay a quick bill. Therefore, it is not considered a current asset.

Accounts receivable are the bills owed to your business (but not yet paid) for goods or services already rendered. For example, if you sell a customer a car and the deal includes them not having to pay any money for the first 6 months, you have an account receivable. This can often include long term dental services that can be billed at the end of a treatment.

Although you do not have the money in your business’s bank account at the moment, it is owed to your business. You may not be able to call it in earlier, but you know that it will be in your bank account in 6 months – unless the customer defaults!

As long as accounts receivable are expected to be paid within a 12 month period, they are considered current assets.

Marketable securities.

Your dental business’s marketable securities are the debts and securities that you can expect to redeem or trade in with a 12 month period. If they are not redeemable within that 12 month period they are considered a fixed asset. They are financial instruments which can be easily liquidated into their market value in cash in one year..

Examples of marketable securities include things such as Government bonds and treasury bills, certificates of deposit and stock.

Prepaid expenses

Prepaid expenses are the expenses paid by the business before a good is received or a service is rendered. For example, leasing a piece of equipment or office space, or even insurance payments are considered prepaid expenses.

Prepaid expenses are considered current assets if they are expected to be completed within 12 months. If your business leases a piece of equipment for less than 12 months, it is considered a current asset. If it is leased for longer than 12 months, it will be considered a fixed asset.

Since the expense has already been paid, this means other working capital can be used for business operations. If you prepay £12,000 for 12 months rent at £1,000 a month, that £1,000 still shows up on the balance sheet. However, since you have already paid it, you essentially have £1,000 extra as working capital.

Current Liabilities

Current liabilities are the financial obligations a business has that it is expected to pay back within a 12 month period. These are the debts that a business needs to pay back within a year, in other words, the business expenses. Debts that you are not expected to repay within that year are not considered current liabilities, they are known as long-term liabilities.

Current liabilities are normally paid off using the current assets. Most businesses will have several current liabilities owed at the same time to suppliers and creditors. Most of the everyday costs of operating a business are paid monthly or as needed, and are therefore considered current liabilities. For instance, utility payments for the offices or warehouses, materials and supplies or business loan repayments.

Examples of Current Liabilities

Accounts payable

Accounts payable are the debts owed by your business for goods or services that have been already received or rendered. They are the outstanding invoices to your suppliers and vendors that are due to be repaid within 12 months.

Any debt that is due within that period is considered a current liability. Debts that are not expected to be repaid in a year will not be listed on your balance sheet as current liabilities.

Accounts payable will cover debts such as supplier invoices, utility bills and invoices from external companies such as legal and marketing services.

Short term debt

Short-term debt, otherwise known as operating debt, are the short-term financial obligations your business has. Operating debt usually takes the form of short-term loans from a high street bank or another financial lender. They can also be issued as commercial paper.

These debts are normally taken out to cover short-term operating costs of the business, such as supplies, bills and invoices. If the debt is expected to be paid within 12 months, it will be considered a current liability.

If you have debt with a loan term of 10 years, that is considered a long-term debt. However, in that final year, it will appear on the balance sheet as a current liability since it is due within 12 months.

Dividends payable

If your dental practice has shareholders who are paid dividends, they may be included are current liabilities on your balance sheet. Once it has been decided that a certain amount should be paid in dividends to the shareholders, they are considered current liabilities until they are paid.

Accrued expenses

Accrued expenses are the expenses which the business knows will have to be paid within a year. They are listed as expenses on the balance sheet but have not yet been paid. Therefore, they are considered current liabilities.

Accrued expenses can cover a range of different payments. For instance, accrued expenses could cover interest payments, including interest for long-term debts, payroll and tax.

Working capital ratio

It is common for a dental business’s working capital to be expressed as a ratio, the working capital ratio. This is a numerical expression of the financial health of the business. A healthy working capital ratio would be between 1.2 and 2.0.

Working capital ratios are calculated by dividing your business’s current assets by its current liabilities. For example, let’s say your business has current assets totalling £750,000 and your current liabilities come to £500,000. We divide the two and get a working capital ratio of 1.5.

If the same business’s liabilities raise to £650,000, the working capital ratio changes to about 1.15. This business is approaching negative working capital, i.e. having more in liabilities than it does in assets. This business may need to apply for working capital finance to pay its debts.

However, if the liabilities fall to £250,000, the working capital ratio is 3. Although it may appear at first sight that the higher the ratio the better, this is not necessarily the case. With £500,000 more in assets than it does in liabilities, this business has an excess of working capital that it should be using to grow the business.

What can cause changes to working capital

A dental practice’s working capital is affected by a wide range of different factors. You can expect your working capital number or ratio to change almost daily.

The most obvious are times when you makes large short-term purchases or sales for your practice. Purchasing new inventory or office supplies will cause your working capital to decrease by increasing the current liabilities. Likewise, selling off property or inventory will increase your working capital ratio by increasing current assets.

The ratio will also change due to long-term assets and liabilities changing in status. For example, a 25 year mortgage is a long-term asset until the 24th year. In that final year the remainder is expected to be paid within a 12 month period, therefore making it a current liability.

There are also instances where customers default on their debts and you may not be able to bring in the accounts receivable that you had planned on. Changes to markets may also mean that your inventory is subsequently valued at less than you purchased it for. This reduces its value and creates a discrepancy with the balance sheet.

If your practice is struggling to pay its debts, whether this be due to an increase in the liabilities or a decrease in the asserts, you may need working capital finance.

When you will need Working Capital Finance

Working capital finance loans are those loans taken out by any business including dental practices to cover short-term expenses. They are not taken out to cover purchases of long-term assets or investments such as property. Businesses apply for working capital finance loans when their current assets and cash flow cannot cover necessary short-term payments.

For instance, a business may take out a short-term working capital loan to cover expenses such as payroll, tax payments, interest payments or inventory purchases.

In a perfect world, all businesses and dental practices would use their own liquid cash or cash equivalents to cover these expenses. However, if a business has a weak cash flow or insufficient working capital in the form of current assets, they may choose to borrow the money to make payments in the form of working capital finance.

Alternatively, businesses may not wish to relinquish any of their current assets to pay liabilities and may prefer to borrow money to do so.

Businesses that experience a high degree of seasonality in their operations, for instance hospitality companies or businesses based in a tourist-centric region can often benefit from working capital finance. If they are unable to cover expenses in their off-season, a working capital loan can allow the business to make necessary purchases.

Dental practices looking to grow quickly, or in the process of doing so, may also apply for working capital finance loans.

The term working capital loan is essentially an umbrella term for any short-term business support loan used to cover business expenses like payroll and tax.

As such, there are several different types of loans and methods of financing that can raise the working capital required to make important purchases and payments.

Options for raising working capital finance include:

Commercial Loans

Commercial loans are perhaps the most common form of working capital finance. These are simply commercial loans that have been received from a financial lender such as a high street bank.

Any loan that is intended to be used to make short-term purchases, as opposed to long-term investments, can be considered a working capital finance loan.

Equity Finance

Many dental practices choose to use equity financing to fund short-term payments. Equity finance is when a business sells part ownership of the business itself in the form of shares in exchange for capital.

Although you can raise a lot of quick capital with equity financing, you will lose at least some control over the operations and strategy of the business.

Equity finance can be raised in a number of ways. For instance, venture capital investors or business angels will purchase shares in exchange for capital. Similarly, you can float the business publically and offer shares out to the wider public.

Mezzanine Finance

Mezzanine is a hybrid form of financing that acts as a middle ground between traditional commercial loans and equity finance. Mezzanine finance takes the form of a normal commercial loan that is guaranteed with business equity.

In other words, you receive a loan in return for regular payments with interest. If you are unable to meet these payments, the lender has the right to receive payment in the form of equity. You will give up part ownership of your business to the lender if you are unable to repay in full.

Overdrafts

It can be possible to obtain a business overdraft from certain banks and sources of alternative lending.

Overdrafts of your dental practice are, in effect, a form of unsecured loan. However, being unsecured does limit how much you can borrow. You will need to demonstrate a strong credit history and ability to repay loans on time to be able to secure meaningful funding in this way.

However, should you be able to do so, overdrafts can be a good way to quickly raise short-term capital.

Revolving credit facilities

Revolving credit facilities can be another way to raise short-term working capital finance for business growth and necessary payments and are similar to overdrafts. A revolving credit is essentially a line of credit offered to businesses from banks and other financial lenders.

A certain limit of credit will be agreed upon between the business and the lender. The business in question, i.e. your dental practice can proceed to then borrow anything up to this limit at any time. Interest is charged on the outstanding debt until it is paid.

Revolving credit facilities are ongoing agreements between creditor and debtor, they are not a fixed loan amount like a traditional commercial loan.

Revolving credit facilities can be a great way to regularly and reliably raise short-term capital.

Invoice finance

Invoice financing is a way for dental businesses to free up working capital that is currently tied up as a current asset in the form of outstanding invoices.

When businesses sell to customers, this is often done so on credit. This is especially true for larger businesses who do not expect customers to pay immediately or for big dental treatments that are paid in instalments or after the treatment has been completed to its end. Instead, the customer is issued an invoice and they pay on or by an agreed upon date.

However, since the goods or services have already been purchased, their value is now tied up in that invoice. Until the invoice is paid, that value is absent from the business.

Invoice financing is a way to free up that working capital by selling the invoice to an invoice factoring company. These companies buy the invoice for a charged percentage. The owed business can then be paid the value of the invoice quicker than if they had waited for the customer to pay on the due date.

This frees up working capital that would otherwise be tied up as a current asset.

Asset Refinancing

Asset refinancing is a way for dental businesses to free up working capital that is currently tied up in their long-term assets which many dental practices usually have in spades. Through asset refinancing, your business can gain access to some of the cash value of the asset without having to sell it off.

Refinancing allows you to borrow money against equity in the asset. This means that you can borrow money against assets you do not fully own. Your loan will be valued against the value of your equity.

When you refinance an asset, you transfer ownership of it to the lender. However, you still maintain the use of it and the lender does not take it away. Once the loan has been fully repaid, full ownership of the asset is returned to you or at least your portion of equity is returned to you.

If you are unable to repay the debt, the lender takes full control of the equity you laid against the loan.

Asset refinancing can be a great way to gain access to value currently tied up in your fixed assets, whilst still keeping them in the business.

Merchant cash advances

Merchant cash advances are a relatively new method of accessing working capital finance. Merchant cash advances allow businesses to borrow money valued against their average monthly profits. The loan is then repaid as a percentage of revenue each month.

If a business makes lots of transactions using a credit card, merchant cash advances allow lenders to forward money based on the monthly credit card takings. This makes them a great option for retail businesses that have a good cash flow but not that much in the way of valuable assets.

If your business made £10,000 last month, lenders will usually agree to lend you the same amount. You usually cannot borrow more than you make in an average month as you will be less able to pay the loan.

Once the money has been advanced, the balance is paid back each month as a percentage of revenue.

Government support

In certain cases and in certain healthcare industries (including dentistry), you may be able to apply for government support to help cover working capital finance for your dental practice.

Many local councils offer financial support and advice to local businesses. It is worth contacting your local council to find out what support and signposting services they offer. You may qualify for a grant or loan directly from them. In other cases, they may direct you to external organisation who may be able to help.

The UK Government is also currently offering help with working capital finance to exporting businesses. The Export Working Capital Scheme aims to help businesses who are operating in the UK but exporting goods outside of the nation by assisting access to working capital finance.

The UK Government will guarantee up to 80% of risk to the lender to help fund pre and post shipment costs.

We’ve been helping to fund the future of British healthcare businesses for over 20 years and our team are made up of former bankers with decades of experience in the UK’s healthcare lending sector.

You can find out more about working with Samera and the financial services we offer by booking a free consultation with one of the Samera team at a time that suits you (including evenings) or by reading more about our financial services at the links below.

Make sure you never miss any of our articles, webinars, videos or events by following us on Facebook, LinkedIn, YouTube and Instagram.

Reviewed By:

Nigel Crossman

Head of Commercial Finance

Nigel is a former banker and head of commercial finance at Samera. He specialises in raising finance, negotiating deals and structuring finance applications for healthcare businesses.