It is still a surprise to me that many borrowers are not aware of how much they can raise when seeking finance for a project.

In most cases, potential borrowers underestimate what they can raise and, therefore, what they can purchase.

When looking at buying a dental practice, the amount you can borrow is often linked to several things and lenders (Banks) all have different policies, limits and requirements.

Who am I dealing with when I borrow finance?

It is very important to ensure that you are dealing with a lender who has experience and knowledge of the dental market. Many bankers are “generalists” and deal with many types of businesses.

Several lenders have set up specialist healthcare teams, staffed with knowledgeable staff who can assess your application in the correct way.

These specialist teams are rarely located in local branches and their experience (as you would expect) varies with how long they have been with the team.

Action Point

When seeking finance for a project, borrowers often underestimate their borrowing potential. It’s crucial to work with lenders experienced in the dental market, as they can accurately assess your application. Specialist healthcare teams within certain lenders can provide valuable insights and tailored financing solutions for dental practice acquisitions.

Loans must be affordable. The EBITDA of a business (Earnings before interest, tax, depreciation and amortisation) will demonstrate whether a business can afford to support a borrowing. You will need to have cash available for a deposit, solicitor’s costs and fees that lenders charge.

You may need to look at how the business will perform in the future with you as the owner. Will you keep on the seller and the existing associates? What new services will you introduce? What will you change?

Lenders may require projections as evidence of how you intend to grow the value of the business.

Action Point

Your borrowing capacity is determined by various factors outlined in bank policies, such as lending amount per dentist, percentage of goodwill valuation, professional experience, and location. Typically, loans can range from 70% to 80% of the practice’s value, with up to 95% available with security. However, affordability is paramount, considering the business’s EBITDA and your ability to cover costs like deposits and fees. Lenders may also require projections demonstrating how you plan to enhance the business’s value under your ownership.

How to navigate the maze when applying for finance

You could contact your own bank and see if they can assist. However, considering all the differences would that be the right structure and cost for you?

Could you get a better deal elsewhere? Remember this is going to be for 15 years!

With all the differences in pricing, fees, loan terms, commitment periods and early repayment penalties it is best to shop around.

As brokers, we are independent. We are not tied to any lender and will look at the market for you, we act solely for you.

We will assess your own situation as an individual case, we will approach several lenders who we believe can help you, using our own experience and knowledge of the industry.

We will obtain offers of finance for you from several sources so that you can compare the offers and decide which is best for you and your business.

We will negotiate on your behalf to get the best price for you and liaise with the lender through the process of due diligence, valuation, taking of security and any other requirements they may have.

You will have us by your side throughout the process, utilising 200 years of banking experience across the team and the knowledge of us having completed so many deals in that time.

Action Points

Independence: Brokers are not tied to any specific lender, allowing them to impartially assess the market and find the best fit for your needs.

Personalized approach: Brokers evaluate your unique situation and approach multiple lenders they believe can offer suitable solutions based on their industry expertise.

Access to multiple offers: Brokers obtain finance offers from various sources, enabling you to compare terms and select the most favorable option for your business.

Negotiation support: Brokers advocate on your behalf, negotiating with lenders to secure competitive pricing and favorable terms.

Expert guidance: With years of banking experience and numerous deals completed, brokers provide invaluable support and guidance throughout the entire process.

We will make sure that you see what is available across the market.

How much capital can I raise for my dental practice?

The amount of capital you can raise for your dental practice depends on several factors, including the practice’s profitability, creditworthiness, and the type of financing sought. Lenders typically consider your financial history, loan-to-value ratios, and the purpose of the funding, whether it’s for expansion, purchasing equipment, or acquiring a practice. With proper financial projections and a solid business plan, dental practices can secure significant funding through loans, equity, or other financing options.

What factors affect the amount of funding I can raise for my practice?

The amount of funding you can raise for your dental practice is influenced by factors such as the practice’s profitability, cash flow, and financial stability. Lenders also consider your credit history, the loan-to-value ratio, and the purpose of the funding, whether it’s for expansion, acquiring new equipment, or purchasing a practice. A strong business plan, solid financial projections, and collateral can further improve your chances of securing a higher amount of capital.

What types of financing options are available for dental practices?

Dental practices can explore several financing options, including:

Traditional Bank Loans: For equipment purchases or practice expansion.

Small Business Loans: Government-backed loans offering favorable terms.

Equipment Financing: Specifically for purchasing dental machinery.

Private Investors: Equity-based funding from investors.

Lines of Credit: Flexible funding for ongoing operational costs.

Each option offers varying interest rates, repayment terms, and eligibility criteria, depending on the practice’s financial health and funding needs

Can I raise capital to expand my dental practice?

Yes, you can raise capital to expand your dental practice through various financing options. These include traditional bank loans, small business loans, and private investors. Lenders typically evaluate your practice’s financial health, profitability, and growth potential when determining the amount of capital you can raise. Expanding into new locations, upgrading equipment, or increasing services are common reasons for seeking expansion funding.

How do lenders assess dental practice loan applications?

Lenders assess dental practice loan applications by evaluating several key factors, including the financial health of the practice, its profitability, and cash flow. They also consider the applicant’s credit history, collateral, and business plan. Lenders look at the purpose of the loan (e.g., for expansion, equipment, or practice acquisition) and assess whether the practice has a solid growth potential. Strong financial projections and past performance improve the chances of securing a loan.

How does practice profitability influence the capital I can raise?

Practice profitability plays a crucial role in the amount of capital you can raise. Lenders and investors assess profitability to determine the financial stability and growth potential of the practice. Higher profitability indicates lower risk, which can result in better loan terms, higher loan amounts, or more favorable interest rates. A profitable practice also demonstrates strong cash flow, making it more attractive to lenders when seeking funds for expansion, equipment purchases, or other needs.

Can I raise funds to buy an existing dental practice?

Yes, you can raise funds to buy an existing dental practice. Financing options include traditional bank loans, small business loans, and specialized healthcare financing. Lenders will evaluate the practice’s current profitability, assets, and cash flow, as well as your personal credit history and business plan. The purchase price and projected return on investment are key factors in determining the loan amount and terms.

What is the loan-to-value ratio for dental practice loans?

The loan-to-value (LTV) ratio for dental practice loans typically ranges from 70% to 85%, depending on the lender and the specific financial situation of the borrower. This means lenders may provide loans covering up to 85% of the practice’s value, while the buyer is expected to contribute the remaining percentage as a down payment. A higher LTV ratio may require stronger creditworthiness or financial guarantees to secure favorable terms.

What documents are needed to secure dental practice funding?

To secure dental practice funding, you’ll typically need the following documents:

Business plan: Detailing the purpose of the loan and projected financial growth.

Financial statements: Recent profit and loss statements, balance sheets, and cash flow reports.

Tax returns: Both personal and business tax returns for the last 2-3 years.

Practice valuation: If purchasing or expanding a practice.

Credit report: Personal and business credit history.

Legal documents: Any relevant agreements or licenses.

How does my credit history impact my ability to raise capital?

Your credit history significantly impacts your ability to raise capital, as lenders use it to assess your financial reliability. A strong credit score demonstrates responsible debt management and reduces the risk for lenders, leading to better loan terms and higher borrowing limits. Poor credit history, on the other hand, may result in loan rejections, higher interest rates, or the need for additional collateral. Improving your credit score before applying can enhance your chances of securing funding.

Are there government loans for dental practices?

Yes, there are government-backed loans available for dental practices, such as those offered through the British Business Bank and other small business loan schemes. These loans often come with favorable terms, lower interest rates, and extended repayment periods, making them an attractive option for financing. Programs like the Startup Loan Scheme and the Coronavirus Business Interruption Loan Scheme (CBILS) also provide funding opportunities for healthcare businesses, including dental practices.

What role do financial projections play in raising capital?

Financial projections play a crucial role in raising capital by providing lenders or investors with a clear picture of your dental practice’s future revenue, profitability, and cash flow. Accurate projections demonstrate your ability to repay loans, manage expenses, and achieve growth. They help assess the financial viability of the practice and can influence the loan amount and terms. Strong financial forecasts increase investor confidence and improve your chances of securing the necessary funding.

What are typical interest rates for dental practice loans?

Typical interest rates for dental practice loans can vary based on factors like the lender, the borrower’s creditworthiness, loan term, and the amount borrowed. Rates typically range from 4% to 12%, with lower rates for highly qualified borrowers or government-backed loans. Secured loans generally offer better rates, while unsecured loans may come with higher interest. It’s essential to compare lenders and loan options to secure the most favorable terms for your dental practice.

Can I use personal savings to fund my dental practice?

Yes, you can use personal savings to fund your dental practice. This is a common method for many business owners looking to avoid debt or interest payments. Using personal savings offers full control over the practice without needing to rely on outside lenders or investors. However, it’s important to assess your financial situation carefully, ensuring that tapping into your savings won’t impact your personal financial security. It may also be helpful to combine personal savings with external funding sources for flexibility.

What strategies can improve my chances of securing a loan?

To improve your chances of securing a loan for your dental practice:

Prepare a strong business plan detailing your growth strategy and loan purpose.

Maintain a good credit score by managing personal and business debt responsibly.

Ensure accurate financial records including profit, cash flow, and tax returns.

Offer collateral or a down payment to reduce risk for lenders.

Show profitability and positive cash flow to prove the practice’s financial stability.

How much equity can I raise for a dental practice?

The amount of equity you can raise for a dental practice depends on the value of the practice and the percentage of ownership you’re willing to sell to investors. Typically, practices with strong profitability and growth potential can attract higher equity investment. Valuations will factor in assets, revenue, patient base, and market conditions. Engaging with investors or private equity firms specialized in healthcare can maximize the amount of equity you raise.

How does practice size affect the amount of funding available?

The size of your dental practice affects the amount of funding available by influencing profitability, cash flow, and overall financial stability. Larger practices with higher revenues and established patient bases are typically seen as lower risk by lenders, making it easier to secure larger loans or investments. Smaller practices may need to provide more robust financial projections and demonstrate strong growth potential to secure similar funding levels. Practice size also impacts the amount of collateral and equity available for securing loans.

Can private investors fund my dental practice?

Yes, private investors can fund your dental practice by providing equity or debt financing. In exchange for equity, investors may take ownership shares, while in debt financing, they provide loans with agreed repayment terms. Attracting private investors often requires a solid business plan and a proven track record of profitability or growth potential. Private investors can offer more flexible terms than traditional lenders and may also provide strategic support to help grow the practice.

What risks should I consider when raising capital?

When raising capital for your dental practice, consider risks such as:

Debt burden: High loan amounts can strain cash flow if revenues fall short. Dilution of ownership: In equity financing, selling shares may reduce your control over the practice. Interest rates: Loans with high-interest rates increase long-term costs. Repayment terms: Inflexible terms can lead to financial strain during slower periods. Risk to personal assets: Collateral-backed loans could put your personal assets at risk if the practice underperforms.

What common mistakes should I avoid when seeking funding for my dental practice?

When seeking funding for your dental practice, avoid common mistakes such as:

Failing to prepare a detailed business plan. Not understanding the terms of loans or equity agreements. Overestimating revenue and underestimating expenses. Relying on a single funding source. Ignoring cash flow management post-funding. Taking on too much debt strains the practice. Not considering the impact on ownership and control when seeking investors.

Business Loans for Healthcare Businesses

We’ve been helping to fund the future of British healthcare businesses for over 20 years and our team are made up of former bankers with decades of experience in the UK’s healthcare lending sector.

You can find out more about working with Samera and the financial services we offer by booking a free consultation with one of the Samera team at a time that suits you (including evenings) or by reading more about our financial services at the links below.

Make sure you never miss any of our articles, webinars, videos or events by following us on Facebook, LinkedIn, YouTube and Instagram.

Reviewed By:

Nigel Crossman

Head of Commercial Finance

Nigel is a former banker and head of commercial finance at Samera. He specialises in raising finance, negotiating deals and structuring finance applications for healthcare businesses.

Dan Fearon

Finance Manager

Dan is a former banker and the head of our dental practice sales team. He specialises in asset finance for healthcare businesses and dental practice sales.

Arun Mehra

Samera CEO

Arun, CEO of Samera, is an experienced accountant and dental practice owner. He specialises in accountancy, financial directorship, squat practices and practice management.

Starting and growing a business costs a lot of money. For most business owners, getting money and managing it can be really hard. That’s where business finance brokers come in to help. In the UK, a business finance broker can help you understand the complicated world of money. They can connect you with many ways to get money and give you advice that’s right for your business. In this blog post, we’ll talk about why it’s a good idea to work with a business finance broker in the UK. They can help you get money, give you expert advice, and make deals with banks that are better for you. We’ll also explain what makes business finance brokers different from other money advisors and how they can open up money opportunities for your business.

Introduction to commercial finance and its importance

Money plays a big role in making businesses successful. Whether you’re a small startup or a well-established company trying to get bigger, having the right financial help is really important to reach your goals.

Business finance means special money services and products made just for businesses. These can be things like loans, credit lines, using your assets to get money, factoring your invoices, leasing equipment, and more. Unlike regular personal money stuff, business finance focuses on giving companies the money they need for things like starting new projects, growing, buying equipment, managing money coming in and going out, and paying bills.

Business finance is super important because it helps businesses bridge the gap between the money they have right now and what they need to grow. So, whether you need money to launch a new product, buy another business, or invest in research and development, business finance is there to help.

One great thing about business finance is that it’s flexible. Unlike personal money options that can be strict, business finance can be customized to fit the specific needs of each business. This means that businesses can get the right funding that matches what they need, which keeps them financially stable and helps them grow.

But, dealing with the world of business finance can be tricky for companies. This is where business finance brokers come in.

A business finance broker acts as a middleman between companies looking for money and the banks or financial institutions that provide it. They really know the business finance market and have a big network of lenders, so they can find the best financial options for their clients.

By choosing a business finance broker in the UK, companies can open up lots of financial opportunities they might not find on their own. These brokers can help figure out how much money a business needs, show options from different lenders, negotiate deals, and ultimately get the best funding deals.

In short, business finance is super important for companies that want to grow and succeed in today’s competitive world. With the help of a reliable business finance broker in the UK, companies can discover a world of financial opportunities and make sure they have the money they need to achieve their goals.

The role of a commercial finance broker

When it comes to understanding the complicated world of business finance, having a knowledgeable and experienced professional by your side can make a big difference. That’s where a business finance broker comes in.

A business finance broker acts as a middleman between companies looking for funding and the banks or financial institutions that provide funding options. Their job is to understand the unique financial needs and goals of their clients and then connect them with the most suitable banks and financial products available in the market.

One of the main advantages of working with a business finance broker is their extensive network of lenders. These brokers have established relationships with various banks, credit unions, private lenders, and other financial institutions, giving them access to a wide range of funding sources. This means they can help you explore multiple funding options and find the best fit for your business.

Additionally, business finance brokers are well-versed in the different types of funding available, such as business mortgages, business loans, asset finance, invoice financing, and more. They have in-depth knowledge of the lending rules, terms, and conditions for each option, allowing them to provide expert guidance and advice tailored to your specific situation.

Another important aspect of working with a business finance broker is their ability to negotiate on your behalf. They understand the intricacies of the lending process and can use their expertise to secure favorable agreements, potentially saving you money in the long run. Moreover, brokers can help streamline the application and approval process, ensuring that all necessary documentation is in order and increasing the likelihood of a successful funding outcome.

In summary, the role of a business finance broker is to simplify the complex world of business finance and provide businesses with access to a wider range of funding options. By leveraging their expertise, industry connections, and negotiation skills, they can help you unlock financial opportunities and make informed decisions that align with your business goals.

Benefits of using a commercial finance broker in the UK

Using a business finance broker in the UK can bring many advantages that can greatly improve your financial opportunities. Whether you are a business owner seeking funding for expansion or a property developer looking for support for your next project, a business finance expert can be a valuable partner in dealing with the complex world of money.

One of the big benefits of working with a business finance expert is their knowledge and experience in the field. They specialize in understanding the complexities of the financial market and have extensive networks and connections in the industry. This means they are well-equipped to find the best funding options for your specific needs. They can analyze what’s available, evaluate different loan products and lenders, and provide you with personalized recommendations that align with your goals.

Another advantage of using a business finance broker is the time and effort they can save you. Researching and comparing various loan options can be a time-consuming and overwhelming task. A broker, on the other hand, can handle all the hard work for you. They will gather the necessary information, complete the paperwork, and negotiate with lenders on your behalf. This allows you to focus on running your business or managing your investments, while the broker takes care of the funding process.

Additionally, business finance brokers often have access to exclusive deals and rates that may not be readily available to individuals or businesses. Their connections with banks and financial institutions can provide you with access to better agreements, potentially saving you money in the long run. They can also provide valuable insights into the current market trends and help you make informed decisions about your financial strategy.

Moreover, using a business finance broker can improve your chances of getting approved for a loan. These experts have a deep understanding of the lending criteria and requirements of different lenders. They can help you prepare a competitive application that highlights your strengths and addresses any potential weaknesses. By presenting your case in the best possible light, a broker can increase your chances of securing the funding you need.

In summary, choosing to work with a business finance broker in the UK can bring a range of benefits to individuals and businesses seeking financial opportunities. From their expertise and industry connections to the time and effort they can save you, partnering with a broker can simplify the funding process and enhance your chances of success. If you’re looking to unlock financial opportunities and navigate the complex world of money, teaming up with a business finance expert is a wise choice.

Regulatory Oversight: In the UK, financial brokers are typically regulated by the Financial Conduct Authority (FCA). Make sure the broker you choose is authorized and regulated by the FCA. You can verify this information on the FCA’s official website.

Independence vs. Tied Brokers: Some brokers are independent, meaning they can recommend products from a wide range of providers, while others are tied to specific financial institutions or companies. Consider whether you prefer an independent broker who can offer a broader selection of options or a tied broker who specializes in a particular area. Samera is an independent broker.

Access to a wide range of financial products and lenders

When it comes to understanding the complex world of business finance and finding the right financial solutions, it’s crucial to have access to a wide range of financial products and lenders. This is where a business finance expert in the UK can be incredibly valuable.

Unlike traditional banks or lenders that often have limited options, a business finance broker has a vast network of lenders and financial institutions at their disposal. This means they can provide you with access to a diverse range of financial products tailored to meet your specific needs and requirements.

Whether you’re seeking a business mortgage, business loan, asset finance, or any other form of funding, a broker can help you explore multiple options and find the most competitive rates and terms available in the market. They have established relationships with various lenders, including mainstream banks, specialized lenders, private investors, and alternative finance providers.

By working with a business finance broker, you can save time and effort that you would otherwise spend searching for suitable lenders on your own. They will do the hard work for you, using their expertise and industry connections to present you with a well-organized list of options that align with your financial goals.

Additionally, a broker can provide valuable insights and guidance throughout the funding process. They possess a deep understanding of the lending landscape and can assist you in selecting the most appropriate financial product for your specific business needs. Their expertise can also improve your chances of securing funding, as they can help you prepare and present strong aspects of your business to lenders.

In summary, choosing to work with a business finance broker in the UK gives you access to a wide array of financial products and lenders. This enables you to explore a broader range of options, secure better terms, and ultimately unlock the financial opportunities that are best suited for your business.

When it comes to finding financial opportunities, having the right knowledge and industry expertise can make a big difference. This is where a business finance expert in the UK can really help. These professionals understand the complexities of the financial world and keep up with the constantly changing market.

By choosing a business finance broker, you gain access to a wealth of knowledge and experience that can be valuable in dealing with the complex world of money. These experts have a deep understanding of various industries and can offer valuable insights tailored to your specific needs and goals.

Whether you need funding to start a new business, expand your current operations, or invest in new ventures, a business finance broker can provide expert advice and guidance. They can help you identify the most suitable funding options available, whether it’s a traditional bank loan, alternative lending solutions, or government-backed programs.

Moreover, business finance brokers have established connections with a wide network of banks and financial institutions. This means they can leverage their relationships and negotiate on your behalf to secure the best possible terms and rates for your funding needs. Their industry knowledge allows them to understand the subtle details of different lenders and their specific requirements, ensuring a smooth and efficient funding process.

In addition to their expertise, business finance brokers also stay up-to-date with the latest market trends and regulations. This ensures that you receive accurate and timely information that can impact your financial decisions. They can advise you on any changes in lending rules, interest rates, or government schemes that could affect your funding choices.

In summary, choosing a business finance broker in the UK gives you access to a wealth of expertise and industry knowledge. Their ability to navigate the financial landscape, connections with lenders, and capacity to navigate complex funding options make them a valuable partners in unlocking financial opportunities for your business.

When it comes to finding money opportunities for your business, time is precious. As a business owner or entrepreneur, your time is really valuable, and spending it on figuring out the complicated world of business finance can be overwhelming and take up a lot of time.

That’s where a business finance broker in the UK can be a game-changer. By choosing to work with a professional broker, you can save valuable time and enjoy unmatched convenience throughout the whole process.

A business finance broker acts as your trusted advisor, guiding you through the complexities of various financial products and lenders. They have extensive knowledge of the market, access to a large network of lenders, and the expertise to match your specific business needs with the right financial solutions.

Instead of spending countless hours researching different banks, comparing interest rates, and filling out numerous applications, a business finance broker streamlines the entire process for you. They do the hard work, conduct thorough research, and provide you with personalized options that align with your financial goals.

Moreover, a broker can often expedite the approval process, as they understand the requirements and preferences of different lenders. This means you can access the funds you need more quickly, enabling you to seize time-sensitive business opportunities and drive your growth.

The convenience provided by a business finance broker goes beyond saving time. They can also handle negotiations on your behalf, ensuring that you secure the most favorable agreements. With their expertise and industry connections, they can often secure better interest rates, flexible repayment options, and higher loan amounts than you could obtain on your own.

Furthermore, a business finance broker can offer personalized guidance and support throughout the entire funding journey. They can help you navigate complex paperwork, decipher financial jargon, and provide valuable insights into the best strategies for managing your business finances.

In summary, choosing a business finance broker in the UK offers significant time-saving benefits and unmatched convenience. By entrusting the task of securing financial opportunities to a professional, you can focus on what matters most – running and growing your business – while having confidence that you are making informed financial decisions.

When it comes to handling the money side of your business, one solution doesn’t fit all. Every business has its own unique financial needs and challenges, and finding the right solutions can be a daunting task. That’s where a business finance expert can make a big difference.

A business finance broker in the UK specializes in understanding the financial landscape and the specific requirements of businesses in various industries. They have the expertise and knowledge to assess your situation and goals, and then create financial solutions that are specifically designed to meet your needs.

Whether you need funding to start a new business, expand your operations, invest in new equipment, or manage cash flow, a business finance broker can guide you through the available options and help you make informed decisions. They have access to a wide network of lenders and financial institutions, allowing them to find the best possible deals for your business.

By working with a business finance broker, you can save valuable time and effort that would otherwise be spent researching and comparing various financial products and services. They will do the research for you, presenting you with a range of options that align with your business objectives. This personalized approach ensures that you receive the most suitable financial solutions that address your specific challenges and help you unlock new opportunities for growth.

Moreover, a business finance broker can also provide valuable support and guidance throughout the application and approval process. They understand the complexities of financial paperwork and can help you prepare the necessary documentation to improve your chances of securing funding. Their experience and industry connections can also expedite the approval process, allowing you to access the funds you need more quickly.

In summary, choosing a business finance expert in the UK offers your business the advantage of tailored financial solutions. With their expertise and access to a vast network of lenders, they can help you navigate the complex financial landscape and find the best possible options for your unique needs. By partnering with a business finance broker, you can unlock financial opportunities that will drive your business forward and ensure its long-term success.

Navigating complex financial processes and requirements

Understanding complex financial processes and needs can be a challenging task, especially for businesses in the UK seeking financial opportunities. This is where the expertise of a business finance broker becomes crucial.

Business finance brokers are specialists who focus on helping businesses with their financial needs. They have a deep understanding of the intricate processes and requirements involved in securing funding or managing financial transactions. From securing loans and mortgages to negotiating lease agreements and restructuring debt, a business finance broker is well-versed in the complexities of the financial landscape.

One of the main advantages of working with a business finance broker is their ability to navigate the maze of regulations and paperwork that often accompany financial transactions. They stay up-to-date with the latest industry trends and regulations, ensuring that businesses are compliant and well-informed at the same time. This expertise can save businesses significant time and effort, allowing them to focus on their core operations.

Moreover, business finance brokers have access to a vast network of lenders and financial institutions. This network enables them to identify the most suitable financial opportunities for each business’s unique needs and circumstances. Whether it’s securing competitive interest rates, finding flexible repayment terms, or exploring alternative funding options, a business finance broker has the connections and experience to negotiate favorable deals on behalf of their clients.

Additionally, the financial landscape is constantly evolving, with new products and opportunities emerging regularly. A business finance broker stays up-to-date with these changes, ensuring that businesses are aware of the latest financial options available to them. By providing tailored advice and guidance, they help businesses make informed decisions that align with their long-term financial goals.

In conclusion, navigating complex financial processes and requirements is a daunting task for businesses. By choosing a business finance broker in the UK, businesses can benefit from their expertise, industry knowledge, and extensive network of lenders. With their guidance, businesses can unlock financial opportunities and pursue sound financial decisions that contribute to their growth and success.

How to choose the right commercial finance broker in the UK

Choosing the right business finance broker in the UK is crucial to unlock the financial opportunities your business needs. With so many options available, it can be overwhelming to figure out which broker is the best fit for your specific needs. However, by considering a few key factors, you can make an informed decision and secure the expertise and support necessary for your financial success.

First and foremost, when selecting a business finance broker, assessing their experience and expertise in the industry is important. Look for a broker with a proven track record of successfully helping businesses obtain suitable financial solutions. A broker with deep knowledge and understanding of the UK business finance market will be better equipped to navigate the complexities and find tailored solutions that align with your unique requirements.

Moreover, consider the broker’s network and connections within the industry. An established broker will have strong relationships with lenders, financial institutions, and other key players in the market. This network can provide you with access to a wider range of funding options and increase your chances of securing favorable terms and rates.

Transparency and trust are also important considerations when choosing a business finance broker. Ensure that the broker is transparent in their communication, providing clear and comprehensive information regarding fees, terms, and conditions. A reputable broker will prioritize your best interests and maintain open communication throughout the entire process.

Furthermore, it is essential to evaluate the level of personalized service and attention you will receive from the broker. A reputable broker will take the time to understand your business goals, financial situation, and specific needs. They will then tailor their approach, offering customized solutions that align with your objectives and help you achieve long-term financial success.

In conclusion, seek testimonials and reviews from previous clients to gain insight into the broker’s reputation and customer satisfaction. Positive feedback and recommendations can provide confidence and trust in your decision-making process.

By carefully considering these factors, you can choose the right business finance broker in the UK, ensuring you have a trusted partner who will help you unlock the financial opportunities your business deserves.

So, why should you be using a commercial finance broker to help you raise finance for your business? Because they give you the best chance of getting the best deal on the market.

Commercial finance brokers have the contacts and know-how to ensure that your application is as likely to succeed as possible. Hey know exactly how banks want applications to be formatted and what they want them to include. They know a good business plan when they see one and they know a viable investment opportunity when they see one and they know a bad loan deal when they see one. A commercial finance broker can help make sure your loan application is more successful than if you had applied on your own.

If you need help with your loan application, or if you want to make sure you are getting the best possible price on the market for your loan, contact us today! Our brokers have a network of contacts throughout the UK’s financial institutions to make sure your business is getting the best funding at the right price.

What is a commercial finance broker, and how can they benefit my business?

A commercial finance broker acts as an intermediary between businesses and lenders, helping you find the most suitable financing options for your specific needs. They benefit your business by leveraging their network of lenders, negotiating better loan terms, and saving you time by comparing various financing options. Brokers can also provide expert advice tailored to your industry, such as dental practices, and assist with long-term financial planning to ensure you secure the best funding at competitive rates.

Why should dental practices use a commercial finance broker?

Dental practices should use a commercial finance broker to access tailored financing options suited to their unique needs. Brokers can help secure competitive loan terms, compare multiple lenders efficiently, and save time in navigating complex financial products. They also provide expert advice and can assist with both short-term capital needs and long-term financial planning, ensuring that dental practices secure funding that aligns with their growth and operational goals.

How do finance brokers compare different loan options for businesses?

Finance brokers compare different loan options for businesses by evaluating key factors such as interest rates, repayment terms, loan amounts, and fees. They assess the financial health and goals of the business to identify the best loan structure. Brokers use their network of lenders to find tailored solutions, ensuring competitive terms and minimizing costs. By analyzing the total cost of borrowing and the suitability of various loan products, brokers help businesses make informed decisions.

Can a broker help improve my chances of securing business funding?

Yes, a commercial finance broker can improve your chances of securing business funding by presenting your application to lenders in the most favorable light. Brokers understand lender requirements and can help ensure your financial documents, business plan, and credit history meet those criteria. They also have access to a wide network of lenders, giving you more options and potentially better terms. Their expertise and negotiation skills increase the likelihood of a successful loan application.

What fees do commercial finance brokers charge?

Commercial finance brokers typically charge a fee based on a percentage of the loan amount secured or a fixed fee for their services. These fees vary depending on the complexity of the financing deal and the size of the loan. Some brokers may charge upfront fees, while others are compensated once the loan is successfully secured. It’s important to clarify the fee structure with your broker before engaging their services to ensure transparency.

How does a broker save time in securing financing?

A broker saves time in securing financing by leveraging their expertise and network of lenders to quickly identify the best loan options for your business. They handle much of the legwork, from comparing loan products to preparing the necessary paperwork, which simplifies the process for you. Brokers also streamline communication between you and lenders, speeding up the approval process and reducing the administrative burden.

Can a broker negotiate better loan terms for my business?

Yes, a broker can negotiate better loan terms for your business by leveraging their relationships with multiple lenders and understanding market rates. Brokers know how to present your financials to lenders in a way that minimizes risk and maximizes favorable terms such as lower interest rates, longer repayment periods, or reduced fees. Their expertise allows them to secure terms that are often better than what you might achieve negotiating on your own.

How can finance brokers assist with long-term business growth?

Finance brokers assist with long-term business growth by securing financing options that align with your expansion goals, such as loans for new equipment, practice expansion, or mergers. They help businesses plan for future financial needs by identifying funding sources that offer flexibility, manageable repayment terms, and competitive rates. Brokers can also provide ongoing financial advice, ensuring that businesses have access to capital when needed, without overextending themselves financially.

What types of business loans can a commercial finance broker find?

A commercial finance broker can help secure various types of business loans, including:

Term loans: For large purchases or expansion.

Working capital loans: To cover day-to-day expenses.

Equipment financing: Specifically for purchasing or leasing equipment.

Business lines of credit: Providing flexible access to capital.

Commercial property loans: For buying or renovating business premises.

Brokers can also assist with specialized loans, such as practice acquisition loans for dentists or other healthcare professionals.

How do brokers tailor financing solutions for dental practices?

Brokers tailor financing solutions for dental practices by understanding the specific needs of the practice, such as equipment purchases, practice expansion, or working capital. They assess the practice’s financial health, revenue streams, and growth potential to match the most suitable loan products. Additionally, brokers can negotiate favorable terms like lower interest rates and flexible repayment options, ensuring the financing aligns with both short-term operational needs and long-term growth goals of the dental practice.

What should I look for when choosing a commercial finance broker?

When choosing a commercial finance broker, look for:

Industry experience: Ensure they have experience in securing loans for dental practices.

Wide lender network: A strong network provides more financing options.

Transparent fees: Clarify the fee structure upfront.

Reputation and reviews: Check client testimonials or case studies.

Tailored solutions: The broker should offer customized financing options based on your specific business needs.

Can brokers access lenders not available directly to business owners?

Yes, brokers often have access to lenders that are not directly available to business owners. They work with specialized lenders, private investors, and institutions that may not market their services to the general public. This wider network allows brokers to present financing options that business owners might not find on their own, often with more favorable terms or tailored solutions for specific industries, such as dental practices.

Which industries benefit most from using finance brokers?

Industries that benefit most from using finance brokers include:

Healthcare and Dental Practices: For equipment financing, practice expansion, and acquisition loans.

Construction: To secure project financing and equipment loans.

Retail and Hospitality: For working capital and property loans.

Manufacturing: To fund machinery purchases and operations.

Real Estate: For commercial property loans and development financing. Finance brokers offer specialized knowledge and access to lenders tailored to these industries, providing more competitive terms and financing solutions.

Can a broker help with both short-term and long-term financing needs?

Yes, a broker can help with both short-term and long-term financing needs. For short-term needs, they can secure working capital loans, lines of credit, or bridge financing to cover immediate expenses. For long-term goals, brokers assist with loans for practice expansion, equipment financing, or commercial property acquisitions. Their expertise ensures the financing options are tailored to the practice’s timeline and financial strategy, helping manage both immediate cash flow needs and future growth.

How do brokers simplify the loan application process?

Brokers simplify the loan application process by handling much of the paperwork and coordination with lenders. They gather the necessary financial documents, prepare the application, and present your business in the most favorable way to lenders. Brokers also streamline communication between you and potential lenders, reducing back-and-forth and ensuring that the application process moves smoothly and quickly. Their experience helps avoid common mistakes that can delay or complicate approvals.

Do brokers help businesses understand loan terms and conditions?

Yes, brokers help businesses understand loan terms and conditions by explaining the details of interest rates, repayment schedules, fees, and any other contractual obligations. They ensure that you fully grasp the implications of the loan, helping you make informed decisions about the financing option. Brokers also clarify any complex terms and advise on the long-term financial impact, allowing you to choose the most beneficial and affordable loan for your business.

How do finance brokers assess the best financing options for a business?

Finance brokers assess the best financing options for a business by evaluating the company’s financial health, including cash flow, creditworthiness, and growth potential. They analyze the specific needs of the business—whether it’s for short-term working capital or long-term expansion—and compare loan options across various lenders. Brokers also consider factors like interest rates, repayment terms, and loan conditions to tailor solutions that align with the business’s financial goals and operational requirements.

What’s the difference between using a broker and going directly to a lender?

The main difference between using a broker and going directly to a lender is that brokers offer access to multiple lenders, providing a wider range of financing options and potentially better loan terms. Brokers handle the legwork, comparing loan products and negotiating on your behalf, whereas going directly to a lender limits you to their specific products. Additionally, brokers can tailor solutions to your needs, simplifying the process and saving time.

Can using a commercial broker lower the cost of business financing?

Yes, using a commercial broker can lower the cost of business financing by helping you secure better interest rates, more favorable repayment terms, and reduced fees. Brokers have access to a wide network of lenders and can negotiate on your behalf to get competitive deals. Additionally, they help you avoid costly mistakes and identify the most suitable financing options for your specific needs, ultimately reducing the overall cost of borrowing.

How do brokers ensure that dental practices get the best loan deals?

Brokers ensure that dental practices get the best loan deals by leveraging their extensive network of lenders to compare multiple financing options. They tailor loan solutions based on the specific needs and financial health of the practice, such as expansion, equipment purchases, or working capital. Brokers also negotiate favorable terms, including lower interest rates, flexible repayment schedules, and reduced fees, ensuring the loan aligns with both short-term and long-term business goals.

Our Expert Opinion

“I cannot stress how important it is to have a commercial finance broker to help you. But not all brokers are equal, you need someone who understands you, your industry, your financial situation. A good broker will find you a deal, a great broker will get you many deals and then help you evaluate the best option available to you.”

We’ve been helping to fund the future of British healthcare businesses for over 20 years and our team are made up of former bankers with decades of experience in the UK’s healthcare lending sector.

You can find out more about working with Samera and the financial services we offer by booking a free consultation with one of the Samera team at a time that suits you (including evenings) or by reading more about our financial services at the links below.

Make sure you never miss any of our articles, webinars, videos or events by following us on Facebook, LinkedIn, YouTube and Instagram.

Reviewed By:

Dan Fearon

Finance Manager

Dan is a former banker and the head of our dental practice sales team. He specialises in asset finance for healthcare businesses and dental practice sales.

Nigel Crossman

Head of Commercial Finance

Nigel is a former banker and head of commercial finance at Samera. He specialises in raising finance, negotiating deals and structuring finance applications for healthcare businesses.

Arun Mehra

Samera CEO

Arun, CEO of Samera, is an experienced accountant and dental practice owner. He specialises in accountancy, financial directorship, squat practices and practice management.

How to make sure a business loan application is successful

Why was your business loan application denied?

If you have recently applied for a business loan and your application was declined, it may feel insulting or demeaning, but the first thing you need to understand is that it is nothing personal. There are several potential reasons for having a business loan denied.

It is important to note that there are many lenders out there with different lending conditions which means that if you get rejected for a certain reason by one lender, you may get accepted elsewhere because a different lender has different loaning options. There are various options that are available to you in order to improve your chances of getting approved the next time you apply.

There are many reasons as to why you may have had a business loan denied, the good part is that it is not at a lender’s discretion to explain why. Usually, you will receive what’s called an adverse action letter from the lender explaining the reasons why you were rejected for a business loan.

There are usually two main factors that lead to lenders denying business loan applications, these are predominantly problems with credit and problems with income.

Here are some of the reasons you might have had a business loan denied.

Poor credit history

Lenders primarily look at your borrowing history which is reflected through your credit scores. This is because lenders want to know if you are able to pay back the loan, seeing a solid history of borrowing and repaying will put the lenders at ease to know that their loan will be repaid back to them.

However, if you have not borrowed much in the past, your lack of credit history may lead to your loan being declined or if you have experienced complications with repaying loans in the past.

Brief credit history

The length of your credit history is important to show your creditworthiness to lenders. They need to be able to see that you have an established history with credit products. No history does not reflect a good history. No history means nothing to base the fact that you will be a responsible borrower.

If you keep up responsible habits such as consistently paying off your bills with a credit card or any other form of credit, in time your score will reach its full potential. This can help reduce the chances of having a business loan denied.

Bankruptcy

Bankruptcy will affect your credit rating therefore making it quite difficult for you to get a loan from many lenders. It is also against the law to borrow more than £500 from any lender without telling them that you are bankrupt until you are discharged from your bankruptcy.

Insufficient/unverified income

Lenders look at your work, investments, and other sources of income in order to assure them that you will be able to repay the loan. With some loans, lenders are required by law to calculate your ability to repay the loan through your income.

Even if you have a good credit history, if the numbers do not add up in the end, lenders may decline your loan for that reason. Either because you don’t earn enough to repay the loan or your income cannot be verified with the information you have provided.

Debt-to-income ratio

This ratio is the comparison of how much you owe each month to how much you earn. Most lenders use your own debt-to-income ratio in order to determine whether you will be able to handle the repayments after the approval of your loan. You may see your business loan denied if the numbers add up and it looks like your business will not be able to handle any new debts.

Collateral

With some loans, you are able to personally guarantee the loan with your lender by essentially pledging a personal asset as collateral that is valued at the same amount of the loan. If you have a poor or brief credit history as well as no collateral, the chances of getting approved for a loan are much lower.

You may think that applying for several loans at once with different companies may increase your chances of getting approved, but think again. When you apply for more than one loan or credit within a short period of time, it negatively impacts your credit rating. There is no limit or rule to determine how much credit you can apply for or the number of applications you wish to make however, there are consequences to your credit rating if you are making multiple applications for credit.

Making multiple loan applications also makes it seem like you are desperate for money which does not sit right with a lot of lenders, the argument is that, if you look like you need the loan so badly, you may struggle to repay it. As this will also reflect badly on your credit rating, it will make it difficult for you to receive credit or loans in the future as with any loan that you apply for, the lender will complete a credit check.

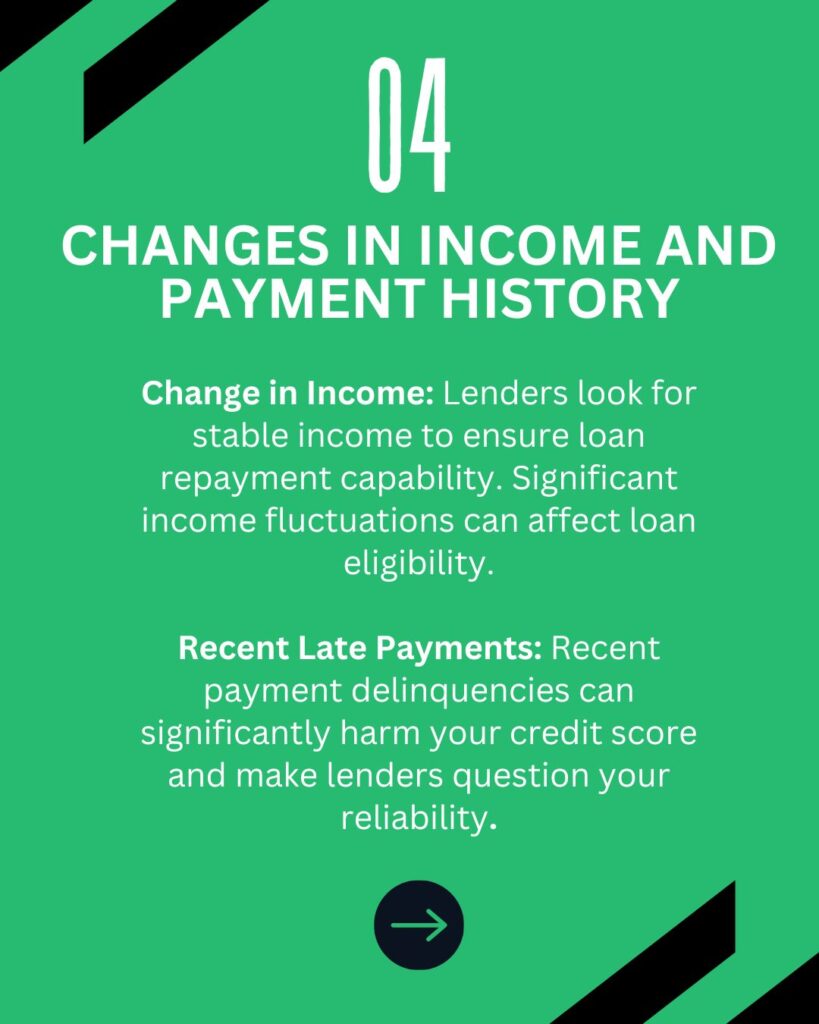

Change in income

The figure on your pay check every month does not affect your credit score. But lenders look at your income to determine whether that income will be sufficient enough to repay the loan. Therefore, affecting your eligibility for certain new credit accounts.

Recent late payments

You may be very responsible when it comes to paying your monthly credit card bills and you may have done it for years, slowly building up your credit score, but you had an off month and out of nowhere you accidentally miss a few payments. Unfortunately this can affect you pretty badly. The higher the score, the harder it falls when something occurs to hurt your credit rating. This, in some cases, can hurt your loan application more than consumers who had poor credit to begin with.

Foreclosure

Usually, for conventional borrowers, there is a waiting period of typically seven years after a foreclosure for the borrower to be eligible for another loan. For mortgage loans, the waiting period is a minimum of three years until you will be able to apply for a mortgage, this is three years from the time that the foreclosure case has completely ended.

Other issues

In some instances, you can have a business loan denied for less obvious reasons. This could include mistakes such as submitting an incomplete application, or perhaps a problem with your business model.

Action Points

Credit Challenges: Issues with poor credit history, brief credit history, or bankruptcy can lead to loan application denial. Lenders assess your borrowing and repayment history to gauge reliability.

Income Verification Problems: Insufficient or unverifiable income may result in loan rejection. Lenders need to ensure your income is adequate for loan repayment.

High Debt-to-Income Ratio: If your monthly debt obligations compared to your income are too high, lenders may doubt your ability to manage additional loan payments.

Lack of Collateral: For loans requiring collateral, not having sufficient assets to secure the loan can lead to denial.

Excessive Credit Inquiries: Applying for multiple loans in a short period can negatively impact your credit rating and make you appear desperate for credit, which is a red flag for lenders.

Income Stability Concerns: Any recent changes in income or employment can affect loan eligibility, as lenders look for stable income for repayment assurance.

Recent Payment Delinquencies: Late payments, especially recent ones, can significantly impact your credit score and loan application, regardless of a previously good credit standing.

Foreclosure History: A recent foreclosure can impose a waiting period before you’re eligible for certain types of loans, affecting your loan application.

Application Errors or Business Model Concerns: Incomplete applications or issues with your business plan can also be reasons for loan denial.

I’ve had a business loan denied – What do I do next?

Having a business loan denied can be disappointing and frustrating but the good news is there are some steps that you can take to get your application reconsidered.

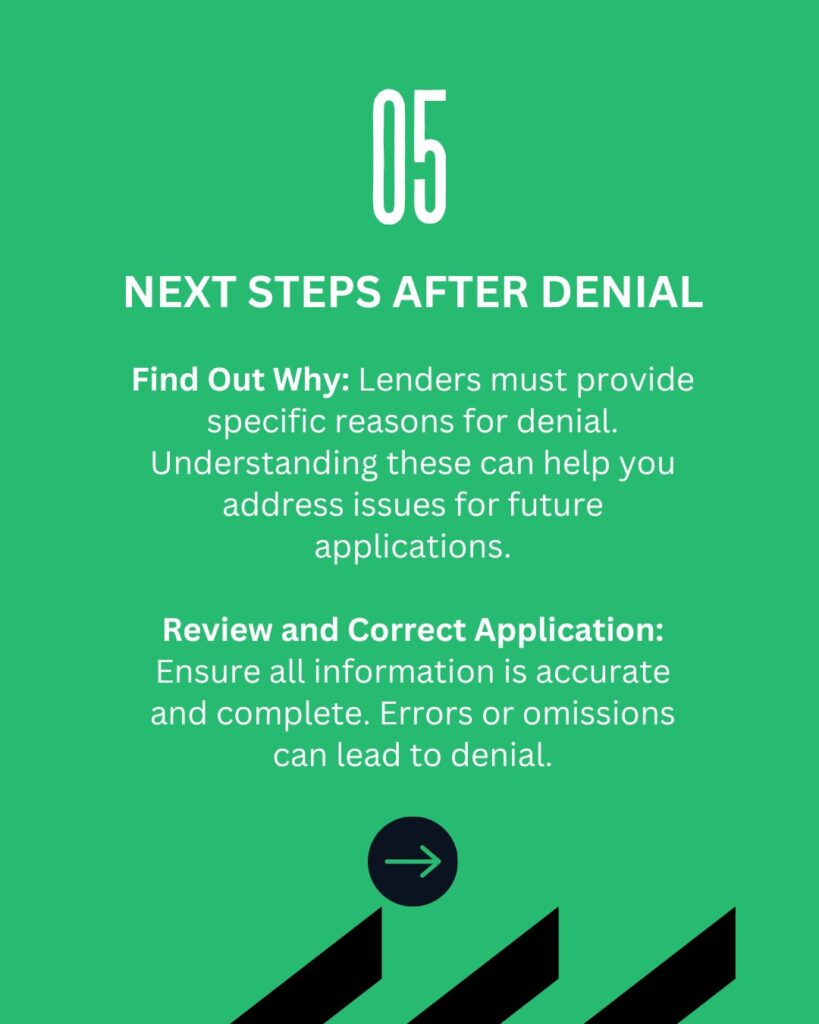

Find out why you were rejected

You need to find out why you were rejected in the first place and also have a lawful right to know. Most lenders will be more than happy to explain why you were rejected and what is required from you to be reconsidered. You have the right to ask the reason behind the rejection within 30-60 days and the lender will be required to inform you the reasons. It is important to note that failure to meet “minimum standards” is not an accepted reason, it has to be a more specific, concrete reason.

It may be a bit soul-crushing reading through a list of why you did not meet a lender’s requirements, but more often than not, it is all about the numbers. The rejection is not personal. You can view the specifics and amend them or change aspects of your lifestyle or business to ensure that next time you will get approved.

Look for errors in your application

You need to thoroughly check through your application, double-check that you have not forgotten to report any source of income or accidentally embellished an additional zero to any numbers.

Review your own credit score

It does not harm your credit score for you to check your own credit. It is a good idea to check in periodically on your credit score to see what is affecting it in a positive or negative way. You are entitled by law to get a free credit report, that way you can see what the banks can see.

Request reconsideration

If you have noticed an error in your application that can be corrected or suspect that you just barely missed the mark to qualify for the loan, it is worth calling the lender to discuss your case. This conversation should be a formal discussion, not you begging to be approved for the loan. How you act affects your image with lenders, go through all the points clearly that you have to get your loan reconsidered and accept whatever their response may be.

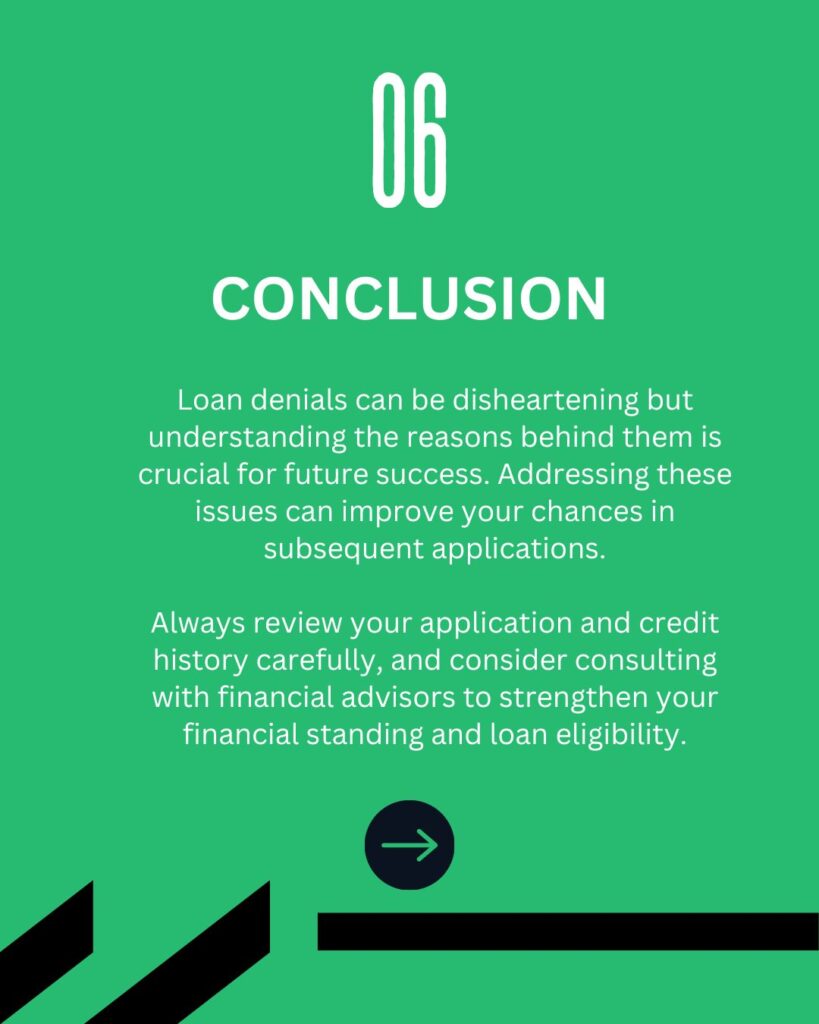

In conclusion, these steps might help you convince a lender to reverse their decision as well as improve your application. Unfortunately there is no guarantee however, there are other options out there for you.

If you have had your business loan denied or you have concerns over your application, contact us today, Our team can help make sure your loan application has the greatest chance of success. We can also advise you on the best alternative funding options for your business if you cannot secure a bank loan.

Action Plan

Identify Rejection Reason: Request the specific reason for your loan denial from the lender, as understanding this can guide improvements.

Review and Correct Application: Double-check your application for accuracy and completeness.

Assess Your Credit: Check your credit report for errors or areas of improvement.

Seek Reconsideration: If an error is found or circumstances have changed, formally request a loan reconsideration with the lender.

Consider Alternatives: If still unsuccessful, explore other funding options suitable for your business needs.

What are the most common reasons for business loan denial?

Business loans are commonly denied due to several factors, including:

Poor credit history: A low credit score signals financial risk.

Insufficient collateral: Lack of assets to back the loan.

Weak cash flow: Inability to demonstrate consistent revenue to repay the loan.

Incomplete documentation: Missing or incorrect financial records.

New business status: Startups often face rejection without a proven track record. Strengthening these areas can improve approval chances.

How does poor credit history affect loan approval?

Poor credit history negatively impacts loan approval as it signals financial instability to lenders. A low credit score indicates a higher risk of default, making lenders hesitant to approve loans or offering them at higher interest rates. Lenders prioritize applicants with strong credit histories, as it reflects responsible debt management and timely payments. Improving your credit score before applying for a loan can significantly boost your chances of approval and help secure better loan terms.

Can weak cash flow lead to loan rejection?

Yes, weak cash flow can lead to loan rejection. Lenders rely on cash flow to assess your ability to repay the loan. If your business cannot demonstrate consistent, strong cash flow, it signals higher financial risk, making lenders reluctant to approve the loan. Improving cash flow by managing expenses and increasing revenue is key to strengthening your application and improving your chances of loan approval.

What role does insufficient collateral play in loan denial?

Insufficient collateral can lead to loan denial because lenders use collateral as security in case the borrower defaults on the loan. Without adequate assets to back the loan, lenders perceive a higher risk, making them less likely to approve the application. Collateral reassures lenders that they can recover their funds, even if the business struggles to meet its repayment obligations. Increasing your collateral or opting for unsecured loans may help in such cases.

How does an incomplete business plan impact loan approval?

An incomplete business plan can significantly impact loan approval because lenders rely on it to assess your business’s viability and potential for growth. A strong business plan outlines your goals, financial projections, and how you plan to use the loan. Without detailed information, lenders may see your business as risky, which can lead to loan denial. Ensuring your plan is thorough and clear can improve your chances of securing funding.

Do new businesses face higher loan rejection rates?

Yes, new businesses often face higher loan rejection rates due to limited financial history and lack of proven revenue. Lenders typically prefer businesses with a track record of profitability and established cash flow, which reduces the perceived risk. New businesses may also struggle with lower credit scores or insufficient collateral, making it harder to meet lending requirements. Strengthening a business plan and improving financial documentation can help improve approval chances.

Why is thorough documentation important for loan approval?

Thorough documentation is crucial for loan approval because it provides lenders with a clear picture of your business’s financial health, stability, and ability to repay the loan. Key documents like financial statements, tax returns, and a detailed business plan help demonstrate transparency and reduce perceived risk for the lender. Missing or incomplete documentation can raise concerns and lead to loan rejection, so it’s important to provide accurate, comprehensive records.

How can I improve my credit score to get a business loan?

To improve your credit score for a business loan, focus on paying off outstanding debts, making payments on time, and keeping your credit utilization low. Regularly review your credit report for errors and correct any inaccuracies. Reducing personal and business debts can also boost your creditworthiness. Building a solid credit history over time will strengthen your financial profile, increasing your chances of loan approval.

What is the impact of outstanding debt on loan approval?

Outstanding debt can negatively impact loan approval because it increases your debt-to-income ratio, signaling to lenders that your business may have difficulty managing additional financial obligations. High levels of debt suggest a higher risk of default, making lenders less likely to approve your application. Paying down existing debts and maintaining a healthy credit utilization ratio can improve your chances of securing a loan.

Can inconsistent financial records result in loan denial?

Yes, inconsistent financial records can lead to loan denial because they raise red flags for lenders, making it difficult to assess the financial stability and reliability of your business. Inaccurate or incomplete financial statements, tax returns, or cash flow reports suggest poor financial management, which increases the risk for lenders. To avoid this, ensure your financial records are accurate, up-to-date, and well-organized before applying for a loan.

How can I strengthen my business’s cash flow for loan approval?

To strengthen your business’s cash flow for loan approval, focus on improving revenue by increasing sales or finding new income streams. Manage expenses effectively by cutting unnecessary costs and renegotiating vendor contracts. Implement efficient invoicing practices to ensure timely payments from clients and maintain adequate cash reserves. Additionally, use financial software to track and optimize cash flow, ensuring stability and reliability in your financial reports, which can reassure lenders of your ability to repay loans.

Does a lack of industry experience affect loan decisions?

Yes, a lack of industry experience can affect loan decisions. Lenders view industry experience as a sign that you understand the market and can effectively manage the business, which reduces the risk of default. Inexperienced business owners may struggle to prove their ability to handle industry challenges, making it harder to secure loans. To improve your chances, you can strengthen your application with a solid business plan, a strong management team, or mentorship from industry experts.

What are the key financial documents required for a business loan?

The key financial documents required for a business loan typically include:

Profit and Loss Statements: To show income and expenses.

Balance Sheets: To demonstrate assets, liabilities, and net worth.

Cash Flow Statements: To highlight your business’s liquidity and ability to repay the loan.

Tax Returns: Business and sometimes personal returns for 2-3 years.

Financial Projections: To show future revenue and growth potential.

Bank Statements: To verify cash flow and account history.

How does a lender assess business risk during the application?

Lenders assess business risk during the loan application process by reviewing key factors like:

Financial Stability: Examining cash flow, profit margins, and debt levels.

Credit History: Checking both personal and business credit scores.

Industry Experience: Evaluating your knowledge and track record in the field.

Collateral: Determining available assets to secure the loan.

Business Plan: Assessing future growth potential and strategy.

These factors help lenders gauge the likelihood of loan repayment.

How can I reapply after being denied a business loan?

To reapply after being denied a business loan, first address the issues that led to the denial, such as improving your credit score, strengthening cash flow, or providing more collateral. Review your financial statements, ensure your business plan is detailed and comprehensive, and gather all required documentation. It’s also beneficial to work with a financial advisor or lender to identify areas for improvement before reapplying.

Can applying for too many loans hurt my approval chances?

Yes, applying for too many loans within a short period can hurt your approval chances. Each loan application triggers a hard inquiry on your credit report, which can lower your credit score. Multiple inquiries also signal to lenders that you may be in financial distress, increasing your perceived risk. To improve your chances, space out applications and focus on strengthening your financial profile before reapplying.

Does personal credit score affect business loan decisions?

Yes, personal credit scores do affect business loan decisions, especially for small businesses or startups. Lenders often evaluate the owner’s personal credit history to assess financial responsibility and gauge the likelihood of loan repayment. A low personal credit score can signal higher risk, leading to potential loan rejection or higher interest rates. To improve your chances, work on building both personal and business credit.

How can I address lender concerns in my reapplication?

To address lender concerns in your reapplication, start by reviewing the reasons for the initial denial and resolving any issues, such as improving your credit score or increasing cash flow. Ensure that your financial documents are accurate and updated. Strengthen your business plan by adding detailed projections and outlining clear strategies for growth. You may also offer additional collateral or a larger down payment to reduce risk for the lender. Working with a financial advisor can further refine your application.

Why is having a strong business plan crucial for loan approval?

A strong business plan is crucial for loan approval because it provides lenders with a clear understanding of your business’s goals, financial projections, and strategies for success. It demonstrates your ability to repay the loan by outlining your revenue streams, growth potential, and risk management plans. A well-prepared plan reduces the perceived risk for lenders, improving your chances of securing the loan with favorable terms.

What are the best ways to prepare before applying for a business loan?

To prepare before applying for a business loan, follow these steps:

Review Credit Scores: Ensure both personal and business credit scores are strong.

Organize Financial Documents: Gather profit and loss statements, tax returns, and cash flow records.

Create a Solid Business Plan: Include financial projections, goals, and strategies.

Improve Cash Flow: Demonstrate consistent revenue and financial stability.

Address Existing Debts: Reduce outstanding liabilities where possible.

Reviewed By:

Nigel Crossman

Head of Commercial Finance

Nigel is a former banker and head of commercial finance at Samera. He specialises in raising finance, negotiating deals and structuring finance applications for healthcare businesses.

Dan Fearon

Finance Manager

Dan is a former banker and the head of our dental practice sales team. He specialises in asset finance for healthcare businesses and dental practice sales.

Arun Mehra

Samera CEO

Arun, CEO of Samera, is an experienced accountant and dental practice owner. He specialises in accountancy, financial directorship, squat practices and practice management.

Business Loans for Dentists

We’ve been helping to fund the future of the UK’s dentists for 20 years and our team are made up of former bankers with decades of experience and contacts in the UK’s healthcare lending sector.

You can find out more about working with Samera Finance and the financial services we offer by booking a free consultation with one of the Samera team at a time that suits you (including evenings) or by reading more about our financial services at the links below.

We’ve been helping to fund the future of British healthcare businesses for over 20 years and our team are made up of former bankers with decades of experience in the UK’s healthcare lending sector.

You can find out more about working with Samera and the financial services we offer by booking a free consultation with one of the Samera team at a time that suits you (including evenings) or by reading more about our financial services at the links below.

We’ve been helping to fund the future of the UK’s dentists for 20 years and our team are made up of former bankers with decades of experience and contacts in the UK’s healthcare lending sector.

You can find out more about working with Samera Finance and the financial services we offer by booking a free consultation with one of the Samera team at a time that suits you (including evenings) or by reading more about our financial services at the links below.

We’ve been helping to fund the future of the UK’s dentists for 20 years and our team are made up of former bankers with decades of experience and contacts in the UK’s healthcare lending sector.

You can find out more about working with Samera Finance and the financial services we offer by booking a free consultation with one of the Samera team at a time that suits you (including evenings) or by reading more about our financial services at the links below.