In this webinar we will discuss tax saving strategies for your practice, simple and complex tax planning opportunities.

Tax Saving Strategies Webinar

Tax Saving Tips For Dentists

The last few tax years saw many new changes in tax legislation. Planning ahead is more important than ever to ensure you work within the rules to not miss out on a tax saving opportunity. Tax for dentists is a complex area that requires specialist tax knowledge about dentistry. Our team has this specialist tax knowledge.

Action Point

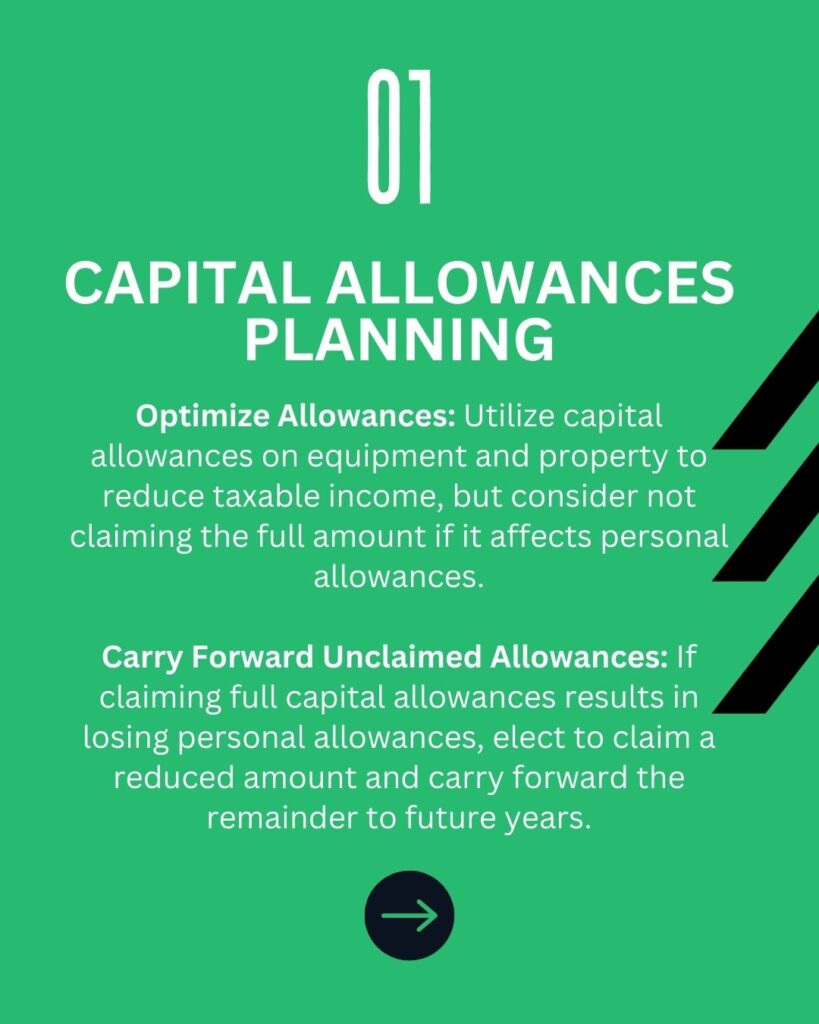

Optimize tax benefits by strategically claiming capital allowances. If claiming full capital allowances would result in losing personal allowances due to high profits, elect to claim a reduced amount. This preserves personal allowances and carries forward unclaimed allowances to future years.

Click here to read our article about financial tips for dentists.

Selective Capital Allowances Planning

Even though you may have spent money on capital items in a tax year, there is no requirement to claim capital allowances at all.

This matters when your circumstances in a tax year mean that if you claimed all of the capital allowances you are eligible for, you would lose your personal allowance.

E.g. Dentist ABC has profits of £100k and losses of £50k brought forward which can be used to reduce the taxable profits.

They also spent £50k on capital items in the year, upon which capital allowances can be claimed. However, an election can be made to reduce the claim to £38.5k instead, leaving £11.5k as the taxable profits. (I.e. £100k -£50k -£38.5k = £11.5k).

By restricting the amount of capital allowances claimed you can still make use of your personal allowances (Which is £11,500 in 2017/18) and carry forward the unclaimed capital allowances into the next year instead of losing them.

Action Point

Strategically plan capital allowances to optimize personal allowance benefits. Consider electing to claim less than the total available to carry forward unclaimed allowances, maintaining personal allowance eligibility.

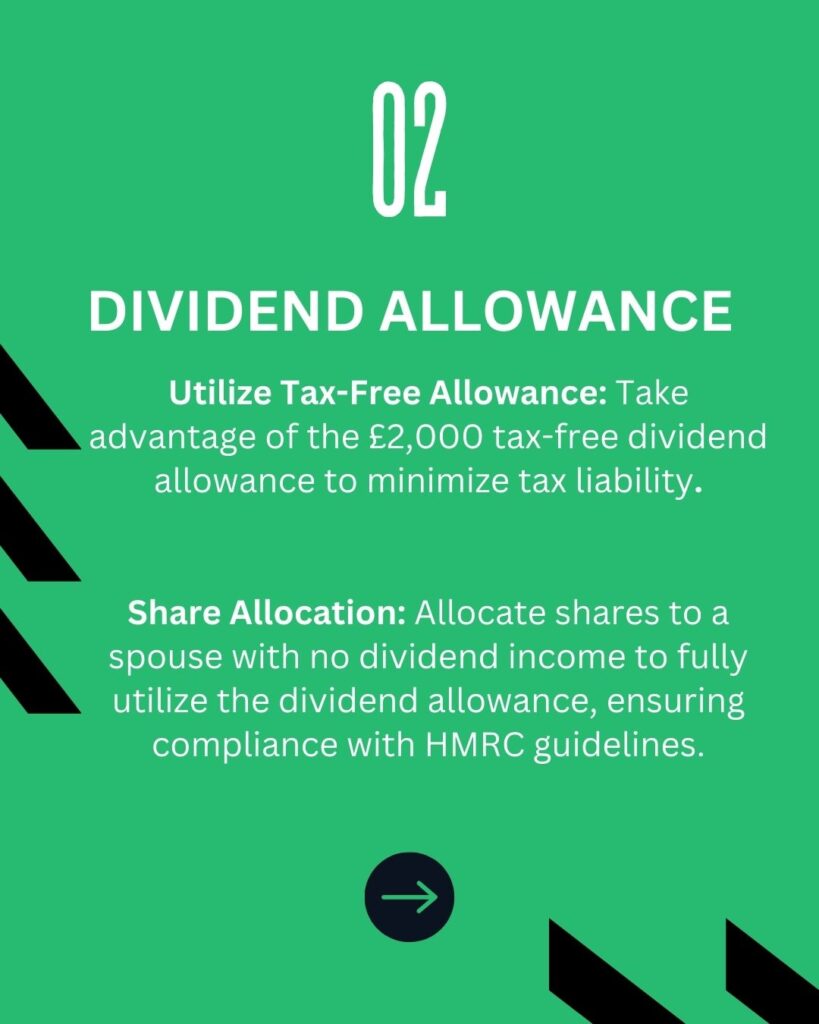

Dividend Allowance

With the new rates of dividends that came in on the 6th April 2021, dividend income is now taxed at 7.5%, 32.5% and 38.1%, depending on whether your total income (including the dividend itself) puts you into the basic rate, higher rate or top rate bracket.

Along with the new rates the Chancellor has now given every UK taxpayer a new £2,000 tax-free “dividend allowance” which means the first £2,000 of dividend income is tax-free. To minimise your tax position, it is possible to allocate some shares to a spouse who doesn’t have dividend income to make sure this dividend allowance isn’t lost. This must be done carefully and within the accepted boundaries to be acceptable to HMRC.

Action Point

Maximize tax efficiency by using the £2,000 tax-free dividend allowance. Allocate shares to a spouse with no dividend income to fully utilize this allowance. Ensure compliance with HMRC guidelines for share allocation.

Contact us to find out more

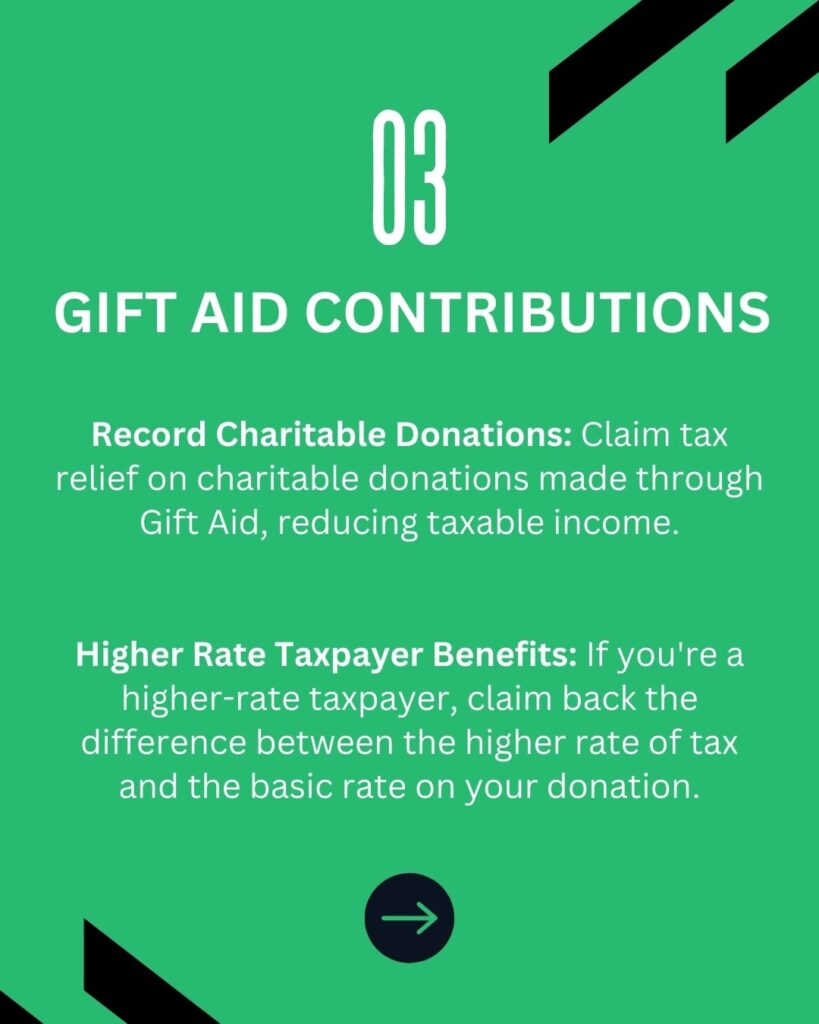

Gift Aid

Remember to record all the charity donations you’ve made. These reduce your taxable income.

If you’re a higher rate taxpayer, you can personally claim back tax.

Example: You donate £100 to charity, they claim Gift Aid to make your donation £125. You pay 40% tax so you can personally claim back £25.00 (£125 x 20%).

Care needs to be taken here though. It can sometimes cost you tax. If you’re close to the personal allowance, this could be the case. Speak to a dental accountant to check what tax you are due back!

Action Point

Maximize tax benefits by recording all charitable donations for tax reduction. Higher-rate taxpayers can reclaim tax on Gift Aid donations. Consult a dental accountant to optimize tax returns and avoid potential costs.

Pension Contributions

When paying into your pension, you receive tax relief on any contributions that you make. This is at the highest rate of income tax that you pay, provided that the total gross pension contributions paid into your pension scheme, by you and anyone else don’t exceed the lower of your annual earnings and the annual allowance.

This could mean that, if you’re a higher rate taxpayer, £10,000 worth of contributions could get you £4,000 tax relief. Meaning you’re receiving at least a £10,000 benefit for only £6,000.

Action Points

Maximize tax relief on pension contributions, especially for higher rate taxpayers, ensuring contributions do not exceed the lower of annual earnings or the annual allowance for optimum benefits.

Limited Company Research & Development

Are you doing something that has never been done before, in advance of current technologies and sciences? This could be something as simple as a website or an app.

Millions worth of tax relief is missed by SME’s, due to people not knowing about this extremely generous tax relief for qualifying expenditure.

For each £10,000 spent on R&D, you could receive £22,500 worth of corporation tax relief. That means that the expense only really cost you just over half of what you spent at £5,500.

The tax rules surrounding this are very complex and therefore require a professional dental accountant to ensure the expenses qualify.

Action Point

Leverage R&D tax relief for innovative projects, potentially receiving £22,500 in corporation tax relief for every £10,000 spent, effectively reducing the cost to £5,500. Seek professional advice to ensure eligibility and maximize benefits.

Click here to find out how Samera can help with R&D tax relief.

Cash In On Self-Employment Profits Taxed Twice

Again, another relief people know little about.

If your self-employment year-end differs from 5th April, it’s very likely you’ve paid tax twice on your overlap profits and therefore with a little planning, you can get this back!

Many sole traders and businesses have a tax relief just waiting to be used and can ‘cash it in’ at any time they choose.

Utilise Your Tax-Free Personal Savings Allowance

Do you have a credit balance Director’s loan account (amount owing to you from your Ltd company)?

If so, you could be missing out on utilising your tax-free personal savings allowance.

Invest Wisely

There are huge tax breaks for investments in EIS / SEIS and VCT’s. To say they are generous is a huge understatement.

For example, you could invest £10,000 into an SEIS and get £5,000 immediate tax relief. What’s more, due to loss relief, even if your investment folds, your actual loss will only be £2,750. You can even carry back to the previous year.

Contact us to find out more

In addition, every individual has a £20,000 ISA allowance available each year, which is income and capital gains tax free, so if you are not utilising this tax saving wrapper, you should really consider this.

Again, the tax legislation surrounding these different investment schemes are complex and the level of relief depends on the individual person so you should ensure you obtain independent tax advice before proceeding.

Claim All The Allowances You Are Eligible For

Whether it is claiming for use of home as an office, or laundry allowance every little helps and working with a Dental Accountant means they will be able to maximise the items you can claim for.

Tax for dentists is a complicated subject which requires knowledge and expertise.

The above is just a taste of some of the top tips, however, we strongly recommend you seek professional advice on any of the subjects detailed above.

Action Point

- Review overlap profits for potential tax relief if your self-employment year-end differs from April 5th.

- Utilize your tax-free personal savings allowance, especially if you have a credit balance in your Director’s loan account.

- Consider investing in EIS/SEIS and VCTs for significant tax breaks and loss relief.

- Maximize your £20,000 ISA allowance annually for income and capital gains tax benefits.

- Claim all eligible allowances, including use of home as an office or laundry expenses, to reduce taxable income.

- Consult with a professional dental accountant to navigate complex tax rules and maximize your tax-saving opportunities.

Our Expert Opinion

“I have had fewer hot meals than the amount of times dentists have asked me to save tax. The truth is the options available to save tax legitimately are limited. Long gone are the days of some questionable tax planning, however, there are reliefs and planning opportunities that are well with the law. Don’t get swayed by someone they can save you tax, instead focus on the basics right to save tax, this means accounting for everything, getting organised and ensuring you have the right tax structures set up for you.”

Tax Saving Strategies for Dentists FAQs

What are the most effective tax-saving strategies for dentists?

The most effective tax-saving strategies for dentists include incorporating your practice to benefit from lower corporate tax rates, maximizing capital allowances on dental equipment, making pension contributions for tax relief, and strategically timing expenses and income to optimize tax outcomes. Additionally, leveraging tax-efficient investments, income splitting with family members, and claiming all allowable business expenses can significantly reduce your tax liability.

How can incorporating my practice reduce my tax burden?

Incorporating your dental practice can reduce your tax burden by allowing you to pay corporation tax on profits, which is often lower than personal income tax rates. You can also take advantage of paying yourself a combination of salary and dividends, which can be more tax-efficient than drawing all income as a sole trader. Additionally, incorporation provides opportunities for tax planning, such as pension contributions and other allowable expenses, further minimizing tax liability.

What deductions are often overlooked by dental professionals?

Commonly overlooked deductions by dental professionals include costs related to continuing education, professional memberships, and subscriptions to industry journals. Additionally, expenses for home office use, travel between practices, marketing, and certain insurance premiums may be missed. Deductions for uniforms, protective clothing, and even some meals while traveling for work are also often not fully utilized. Ensuring these expenses are properly recorded and claimed can lead to significant tax savings.

How do pension contributions contribute to tax savings?

Pension contributions reduce your taxable income, allowing you to pay less tax. Contributions to a registered pension scheme are eligible for tax relief, meaning the amount you contribute is deducted from your income before tax is calculated. For higher-rate taxpayers, this can result in significant savings, as contributions are taxed at your highest marginal rate. Additionally, pension growth is tax-free, providing long-term benefits for retirement planning.

What role does tax-efficient investment play in reducing taxes?

Tax-efficient investments play a crucial role in reducing taxes by allowing you to grow your wealth while minimizing tax liabilities. Investments in ISAs (Individual Savings Accounts) or pensions, for instance, offer tax-free growth on returns. Additionally, schemes like the Enterprise Investment Scheme (EIS) or Seed Enterprise Investment Scheme (SEIS) provide tax reliefs on investments in qualifying companies, reducing your taxable income or deferring capital gains tax. These strategies help in long-term financial planning while optimizing tax savings.

How can I leverage capital allowances for dental equipment?

You can leverage capital allowances for dental equipment by claiming deductions on the cost of assets used in your practice. The Annual Investment Allowance (AIA) allows you to deduct the full cost of qualifying equipment from your taxable profits in the year of purchase, up to a certain limit. If your expenditure exceeds the AIA limit, you can claim writing-down allowances to spread the tax relief over several years. This strategy helps reduce your overall tax liability.

What are the benefits of income splitting in a dental practice?

Income splitting in a dental practice involves distributing income between family members, such as a spouse or children, who are involved in the business. By paying family members a reasonable salary for their work, you can reduce the overall tax burden, as the income is taxed at their lower tax rates rather than your higher rate. This strategy can lead to significant tax savings, especially if the family members are in lower tax brackets.

How can I maximize tax reliefs on business expenses?

To maximize tax reliefs on business expenses, ensure you claim all allowable deductions, such as dental supplies, equipment, and professional fees. Keep detailed records and receipts for every expense. Regularly review your expenditures to identify additional deductible items like training costs, travel, and office supplies. Consider using accounting software to track and categorize expenses efficiently. Consulting with a tax advisor can also help you identify less obvious deductions and optimize your tax relief strategy.

What is the impact of charitable donations on my tax liability?

Charitable donations can reduce your tax liability by allowing you to claim tax relief on qualifying donations. In the UK, donations made under the Gift Aid scheme enable charities to reclaim 25% of the donation amount from HMRC, and higher-rate taxpayers can claim additional relief, reducing their taxable income. This strategy not only supports charitable causes but also provides a tax-efficient way to lower your overall tax bill.

How does timing purchases and expenses affect tax savings?

Timing purchases and expenses strategically can significantly impact tax savings by allowing you to maximize deductions in the current tax year. For instance, making large purchases or paying for services before the end of the tax year can reduce taxable income, lowering your tax bill. Conversely, delaying income or deferring expenses to the following year can help manage cash flow and prevent pushing your income into a higher tax bracket. This careful timing ensures you optimize your tax position.

What are the tax benefits of using a home office for dental practice tasks?

Using a home office for dental practice tasks can offer several tax benefits. You can claim a portion of your household expenses, such as utilities, rent, mortgage interest, and internet costs, based on the space used for business and the time spent working from home. This deduction reduces your taxable income, leading to lower tax liability. It’s important to maintain accurate records and ensure that the space is used exclusively for business purposes to qualify for these tax benefits.

How can loss relief be utilized to offset future profits?

Loss relief can be utilized to offset future profits by carrying forward trading losses to reduce taxable income in subsequent years. This strategy lowers your tax liability in profitable years by using past losses to offset gains. Additionally, you may be able to carry back losses to previous years or set them against other forms of income, depending on specific tax rules. This approach helps stabilize your practice’s tax obligations over time, especially during periods of fluctuating income.

What are the implications of tax planning on my retirement?

Tax planning has significant implications for your retirement by helping to optimize savings and minimize tax liabilities. Effective strategies include contributing to tax-advantaged pension schemes, like SIPPs or employer pensions, which offer tax relief on contributions and tax-free growth. Proper planning can also ensure that withdrawals during retirement are tax-efficient, helping to preserve more of your wealth. Additionally, managing investments through ISAs or similar tax-efficient vehicles can enhance your financial security in retirement.

How can I use employee benefits to reduce overall tax costs?

You can reduce overall tax costs by offering tax-efficient employee benefits such as salary sacrifice schemes, employer pension contributions, and health insurance. These benefits often come with tax advantages, like reduced National Insurance contributions for both the employer and employee. Additionally, offering non-cash benefits instead of cash bonuses can be more tax-efficient, lowering the practice’s taxable income while providing valuable incentives to employees.

What are the advantages of tax-efficient estate planning?

Tax-efficient estate planning helps minimize the tax burden on your heirs and ensures that more of your wealth is passed on to your beneficiaries. Advantages include reducing inheritance tax through gifting, using trusts to control asset distribution, and leveraging tax-free allowances and reliefs. It also allows for more strategic management of assets, ensuring that your estate is distributed according to your wishes while minimizing potential tax liabilities.

How do I ensure compliance while maximizing tax savings?

To ensure compliance while maximizing tax savings, keep accurate and detailed financial records, stay updated on relevant tax laws, and claim all allowable deductions and reliefs. Regularly review your tax strategies with a professional accountant who understands your industry. Ensure that your tax planning strategies are within legal guidelines to avoid penalties. Use reputable accounting software to track expenses and income accurately, and conduct regular audits to verify compliance with tax regulations.

What strategies can I use to manage tax payments throughout the year?

To manage tax payments throughout the year, consider the following strategies:

- Budget for Taxes: Set aside funds regularly based on estimated tax liabilities.

- Use Payment on Account: Spread tax payments evenly throughout the year.

- Optimize Cash Flow: Time income and expenses to align with tax deadlines.

- Automate Payments: Schedule payments to avoid late fees and penalties.

- Regular Tax Reviews: Monitor your financial situation quarterly to adjust for any changes.

How can I prepare for changes in tax legislation affecting dentists?

To prepare for changes in tax legislation affecting dentists, consider the following strategies:

- Stay Informed on Legislative Changes:

- Subscribe to Updates: Regularly follow updates from HMRC, professional dental associations, and financial news sources to stay aware of new tax laws and regulations.

- Attend Workshops and Seminars: Participate in industry-specific seminars and webinars that focus on recent and upcoming tax changes.

- Consult with a Tax Professional:

- Engage an Accountant: Work with an accountant or tax advisor who specializes in dental practices to understand how legislative changes specifically impact your business.

- Regular Reviews: Schedule periodic consultations to review your tax strategy and ensure it aligns with current laws.

- Adjust Financial Planning and Strategies:

- Reevaluate Tax Strategies: Modify your existing tax strategies to take advantage of new deductions, credits, or allowances introduced by the changes.

- Optimize Expense Timing: Plan the timing of significant purchases or expenses to maximize tax benefits under the new legislation.

- Enhance Record-Keeping Practices:

- Maintain Detailed Records: Keep comprehensive and organized financial records to ensure compliance and make it easier to implement changes.

- Use Accounting Software: Utilize up-to-date accounting software that can adapt to new tax rules and help automate compliance tasks.

- Implement Flexible Business Structures:

- Review Business Structure: Assess whether your current business structure (e.g., sole proprietorship, limited company) remains the most tax-efficient under the new laws.

- Consider Incorporation Benefits: If beneficial, consider incorporating your practice to take advantage of potential tax savings offered to corporations.

- Adjust Retirement and Investment Plans:

- Pension Contributions: Reevaluate your pension contributions to ensure you are maximizing tax relief opportunities.

- Tax-Efficient Investments: Explore new tax-efficient investment options that may become available or more advantageous under the revised legislation.

- Prepare for Increased Compliance Requirements:

- Understand New Obligations: Identify any additional compliance requirements introduced by the tax changes and implement necessary processes to meet them.

- Training and Education: Ensure that you and your staff are knowledgeable about new compliance procedures through training sessions.

- Develop a Contingency Plan:

- Financial Buffer: Create a financial buffer to manage potential increases in tax liabilities or unexpected compliance costs.

- Scenario Planning: Conduct scenario planning to anticipate various outcomes based on different legislative changes and prepare appropriate responses.

- Leverage Professional Networks:

- Join Professional Groups: Engage with dental and business networks to share insights and strategies for adapting to tax changes.

- Advocate for Your Interests: Participate in advocacy efforts through professional associations to influence favorable tax policies.

- Regularly Review and Update Your Tax Strategy:

- Annual Assessments: Conduct annual assessments of your tax strategy to ensure it remains effective and compliant with the latest laws.

- Adapt to Feedback: Use feedback from your accountant and financial performance data to continuously refine your approach

What are the benefits of working with a tax advisor specialized in dental practices?

Working with a tax advisor specialized in dental practices offers several benefits, including expert knowledge of industry-specific tax deductions and credits, personalized tax planning strategies, and ensuring compliance with ever-changing tax regulations. They can help you maximize tax savings, manage cash flow more effectively, and provide guidance on complex tax issues like incorporation, capital allowances, and pension contributions. Their expertise can lead to significant financial savings and peace of mind, allowing you to focus on running your practice.

How can I optimize cash flow while implementing tax-saving strategies?

To optimize cash flow while implementing tax-saving strategies, focus on timing your expenses and income to align with tax deadlines, which helps manage liquidity. Utilize capital allowances and claim all allowable deductions to reduce tax liabilities and retain more cash in the practice. Consider spreading tax payments throughout the year with payment on account, and regularly review your financial situation to adjust strategies as needed. Collaborate with a tax advisor to balance cash flow needs with effective tax planning.

About the Author

Arun Mehra

With almost twenty years of commercial experience and knowledge in Dentistry, Arun’s expertise is valued by hundreds of businesses across the UK. His financial acumen and know-how, along with his hands-on commercial expertise have helped clients, large and small, new and established to achieve great things.

Arun is the founder of the Samera Group, starting the business with just one client sitting at his father’s dining table. Fifteen years on, Team Samera now service hundreds of Dental clients, run exciting events, help clients raise finance, and are very active in helping clients buy or sell Dental practices.

Dental Accounts & Tax Specialists

As dental practice owners ourselves, we know what makes a clinic tick. We have been working with dentists for over 20 years to help manage their accounts and tax.

Whether you’re a dental associate, run your own practice or own a dental group and are looking to save time, money and effort on your accounts and tax then we want to hear from you. Our digital platform takes the hassle and the paperwork out of accounts.

To find out more about how you can save time, money and effort on your accounts and tax when you automate your finances with Samera, book a free consultation with one of our accounting team today.

Contact Information

Fill in the form and our team will get back to you as soon as possible.

or

or

Dental Accounts & Tax: Further Information

Make sure you never miss any of our articles, webinars, videos or events by following us on Facebook, LinkedIn, YouTube and Instagram.