The inheritance tax nil rate band has been frozen at its current level of £325,000 since 6th April 2009. The nil rate band is the amount of your estate that is exempt from inheritance tax.

It will remain at its current level of £325,000 until 5th April 2026 – a 17-year freeze! However, since 6th April 2017, a new additional nil rate band has been available for the ‘family home’.

Click here to read our guide on income tax and National Insurance.

Generally speaking, effective inheritance tax planning should be carried out on a long-term basis. However, it is worth remembering the following points, which should be considered on an annual basis.

Annual exemption

The first £3,000 of gifts made by any individual during each tax year is completely exempt for inheritance tax. In addition to this, if the previous year’s annual exemption was not fully utilised, it can be carried forward into the following (current) tax year.

This means, in one tax year you are able to have up to £6000 of gifts that will be exempt from any tax only if you have not made any gifts during the previous tax year.

This exemption is specific to a per person basis, so married couples can also make gifts of £3,000 each.

Small Gifts Exemption

Gifts of up to £250 per tax year made to any one individual are also exempt from any inheritance tax and do not count towards the annual exemption. These types of small gifts are an exemption for you as you can make as many of these gifts as you like to different people.

However, the annual exemption cannot be used for further gifts to the same recipient in the same tax year.

Habitual Gifts Out of Income

Habitual gifts out of income are an exemption from inheritance tax, in order for these gifts to be classed as ‘habitual’, they need to be made consistently for a number of years. Which is why it is important to remember to keep these up every tax year.

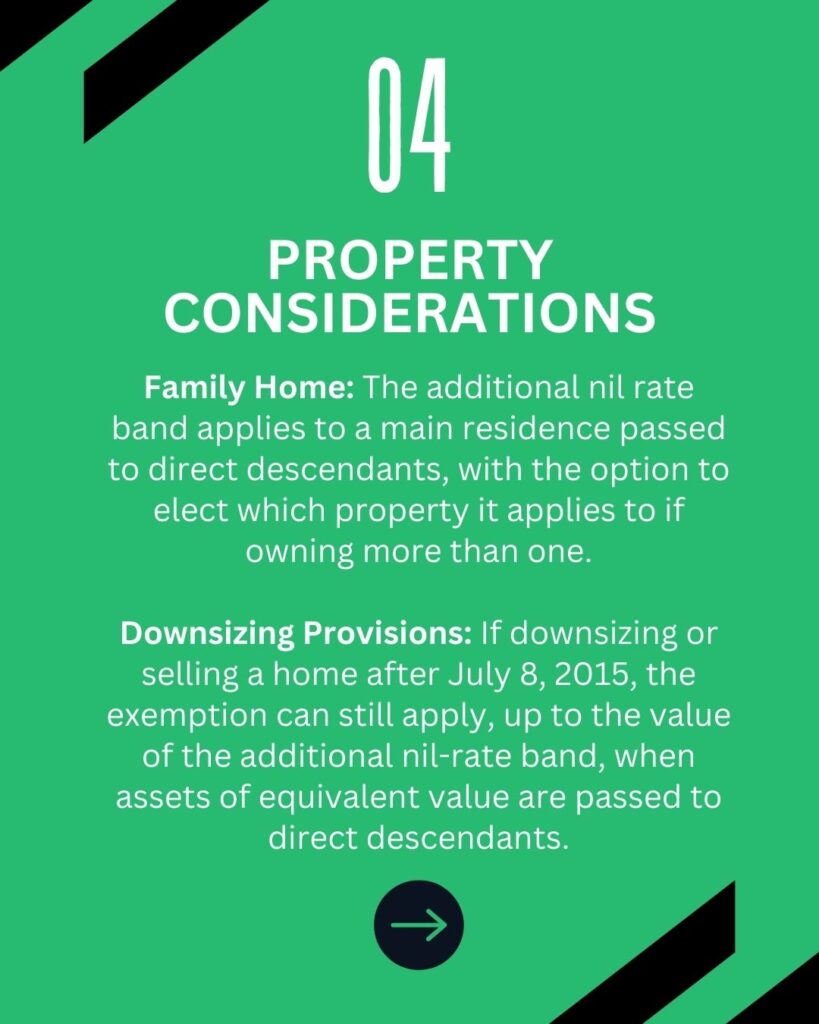

The Family Home

An additional nil rate band is available for the ‘family home’ for any deaths occurring after 6 April 2017. This exemption is only available on a property which has been the deceased residence at some point during their life. If the deceased has passed while owning more than one or multiple qualifying properties, the personal electives can elect which property this exemption should apply to.

The exemption is only applied once the property is passed. This is usually done to a direct descendant of the deceased and in this case, any stepchildren, foster children or adopted children are all accorded the same status as one another for this sole purpose.

Similar to the £325,000 nil rate band, any unused proportion of the exemption will pass to the deceased’s partner or spouse.

When a person downsizes or ceases to own a home after 8 July 2015, the residence nil rate band is available to them as well as assets of an equivalent value, up to the value of the additional nil-rate band, are passed to direct descendants.

The residence nil-rate band that was introduced in 2017/18 and increased from £100,000 to its current value to £175,000. This level is set to remain until 5 April 2026.

Click here to read more about inheritance tax.

Inheritance Tax: Example

Margaret divorced her husband many years before her death in June 2021.

She leaves her estate, worth £600,000, to her daughter.

Margaret’s estate includes her former home, which is worth £250,000 at the time of her death. The residence nil rate band available for 2021/22 exempts £175,000 of the value of Margaret’s former home. This reduces her taxable estate to £425,000 before deduction of her main nil rate band of £325,000, which reduces it to £100,000.

The IHT payable on Margaret’s estate at 40% is thus £40,000. The residence nil rate band is withdrawn from estates worth in excess of £2 million (this threshold is also frozen until 5th April 2026).

This withdrawal is at the rate of £1 for every £2 by which the estate exceeds £2 million. Any mortgages or other loans secured over a property will have to be taken into account when allocating the exemption. For example, where the deceased held a property worth £250,000 which was subject to a mortgage of £180,000, the exemption will be limited to just £70,000.

A Guide to Inheritance Tax FAQ

What is inheritance tax in the UK?

Inheritance tax in the UK is a tax on the estate of someone who has passed away. The estate includes assets such as property, money, and personal possessions. The tax is applied to the portion of the estate that exceeds the tax-free threshold, which is currently £325,000. Anything above this amount may be taxed at a rate of 40%. However, there are exemptions and reliefs available, such as passing assets to a spouse or civil partner, which can reduce or eliminate the tax liability.

How much is the inheritance tax rate in the UK?

The inheritance tax rate in the UK is 40% on the value of an estate that exceeds the tax-free threshold, which is currently set at £325,000. However, if 10% or more of the estate is left to charity, the rate can be reduced to 36%. Additionally, some exemptions and allowances, such as the residence nil-rate band, can further reduce the taxable amount.

Who pays inheritance tax on an estate?

Inheritance tax on an estate is typically paid by the executor of the will or the administrator if there is no will. The tax is paid using funds from the estate before assets are distributed to the beneficiaries. Beneficiaries usually do not pay inheritance tax directly, unless they receive certain types of gifts or trusts that may have specific tax implications. If the tax isn’t paid on time, interest may be charged on the amount owed.

What is the current inheritance tax threshold?

The current inheritance tax threshold in the UK is £325,000. This is known as the nil-rate band, meaning no inheritance tax is due on estates valued up to this amount. Any part of the estate exceeding this threshold is typically taxed at a rate of 40%. However, the threshold can be increased with the residence nil-rate band, allowing an additional £175,000 if the deceased passes their home to direct descendants, such as children or grandchildren.

Can you avoid paying inheritance tax legally?

Yes, there are several legal ways to reduce or avoid paying inheritance tax in the UK:

- Gifting Assets: You can give away assets during your lifetime. Gifts made more than 7 years before your death are typically exempt from inheritance tax under the “7-year rule.”

- Spouse or Civil Partner Exemption: Anything left to your spouse or civil partner is exempt from inheritance tax.

- Charitable Donations: Gifts to charities are inheritance tax-free, and if you leave 10% or more of your estate to charity, the tax rate on the remaining estate can be reduced from 40% to 36%.

- Trusts: Placing assets in a trust can reduce the inheritance tax liability by removing them from your estate.

- Residence Nil-Rate Band: Passing your home to children or grandchildren can increase your tax-free threshold by an additional £175,000.

- Life Insurance: A life insurance policy can be set up to cover the inheritance tax liability, ensuring that beneficiaries don’t have to sell assets to pay the tax.

Effective estate planning with these methods can significantly reduce or eliminate the inheritance tax burden.

Are there any exemptions from inheritance tax?

Yes, several exemptions from inheritance tax exist in the UK, including:

- Spouse or Civil Partner Exemption: Any assets passed to a surviving spouse or civil partner are exempt from inheritance tax, regardless of the estate’s value.

- Charitable Donations: Gifts left to registered charities are exempt from inheritance tax. Additionally, if 10% or more of your estate is donated to charity, the inheritance tax rate on the remaining estate is reduced to 36%.

- Annual Gift Exemptions: Each year, you can give away up to £3,000 in gifts without it being counted towards inheritance tax. Unused allowances can be carried forward for one year.

- Small Gifts Exemption: Gifts of up to £250 per person per year are exempt, provided the recipient hasn’t benefited from your £3,000 annual allowance.

- Gifts Between 7 Years of Death: Gifts made more than 7 years before death are typically exempt under the “7-year rule.”

- Residence Nil-Rate Band: An additional £175,000 tax-free allowance is available if you pass your home to direct descendants like children or grandchildren.

These exemptions can significantly reduce or eliminate inheritance tax liability.

What is the 7-year rule for inheritance tax on gifts?

The 7-year rule for inheritance tax in the UK applies to gifts you make during your lifetime. According to this rule, if you gift assets and survive for 7 years after making the gift, the gift will be exempt from inheritance tax.

If you pass away within 7 years of making the gift, the gift may still be subject to inheritance tax. However, the tax rate can decrease on a sliding scale, known as taper relief, depending on how many years have passed since the gift was made:

Less than 3 years: 40% (full inheritance tax rate)

3 to 4 years: 32%

4 to 5 years: 24%

5 to 6 years: 16%

6 to 7 years: 8%

After 7 years: 0% (no inheritance tax)

This rule allows you to reduce inheritance tax by gifting assets early in life.

How does the residence nil-rate band affect inheritance tax?

The residence nil-rate band (RNRB) is an additional tax-free allowance that can reduce inheritance tax when you pass your home to direct descendants, such as children or grandchildren. It works alongside the standard inheritance tax threshold and can significantly increase the amount of your estate that is exempt from tax.

- Key Points:

- Additional Allowance: As of now, the RNRB provides an extra £175,000 on top of the standard inheritance tax threshold of £325,000. This means your estate could potentially pass on up to £500,000 tax-free, if the home is included.

- Married Couples and Civil Partners: If you’re married or in a civil partnership, any unused allowance can be transferred to your partner, allowing a combined tax-free threshold of up to £1 million.

- Eligibility: The RNRB applies only if you leave your primary residence to direct descendants (children, stepchildren, grandchildren, etc.). It doesn’t apply if you leave your home to other relatives or friends.

- Estates Over £2 Million: For estates valued over £2 million, the RNRB is reduced by £1 for every £2 over the threshold. This is known as the tapering effect, which can eventually eliminate the RNRB for very large estates.

The residence nil-rate band can help reduce or even eliminate inheritance tax on the value of your home when passed to your heirs.

Do gifts reduce inheritance tax liability?

Yes, gifts can reduce inheritance tax liability if structured correctly. Several rules and exemptions apply to gifts that can help minimize the amount of inheritance tax due:

- Key Ways Gifts Reduce Inheritance Tax:

- The 7-Year Rule: Gifts made more than 7 years before your death are exempt from inheritance tax. If you survive for 7 years after making the gift, it will not count towards the value of your estate.

- Annual Exemptions: You can give away up to £3,000 per tax year without it being counted towards inheritance tax. If unused, this allowance can be carried over for one year, allowing up to £6,000 in tax-free gifts.

- Small Gifts Exemption: You can give gifts of up to £250 to any number of individuals each tax year, as long as these gifts don’t exceed £250 per recipient.

- Gifts for Weddings or Civil Partnerships: Gifts to a child for their wedding or civil partnership are exempt up to £5,000; for a grandchild or great-grandchild, the limit is £2,500, and for others, it’s £1,000.

- Regular Gifts from Income: If you can prove that you regularly give gifts from your surplus income and it doesn’t reduce your standard of living, these gifts may be exempt from inheritance tax. This is called “normal expenditure out of income.”

- Charitable Donations: Any gifts left to charity are completely free from inheritance tax. Additionally, leaving 10% or more of your estate to charity can reduce the overall inheritance tax rate from 40% to 36%.

Using these gift exemptions effectively can help reduce the overall size of your taxable estate, lowering or even eliminating the inheritance tax liability.

How do trusts help with inheritance tax planning?

Trusts are a valuable tool for inheritance tax planning because they allow individuals to control how their assets are distributed while potentially reducing the amount of inheritance tax (IHT) due. Here’s how trusts can help with inheritance tax planning:

- Life Interest Trusts:

- These trusts allow a beneficiary (often a spouse) to benefit from income generated by the trust during their lifetime, while the assets themselves are passed to other beneficiaries (like children) after their death. The trust can provide for a spouse while reducing the taxable value of the estate for IHT purposes.

- Removing Assets from the Estate:

- When you place assets in a trust, they are no longer considered part of your estate for inheritance tax purposes, provided you survive for 7 years after transferring the assets. This can significantly reduce the value of your taxable estate.

- Controlling Asset Distribution:

- Trusts allow you to set specific conditions on how and when beneficiaries receive the assets. This helps protect wealth for future generations and ensures assets are not taxed multiple times as they pass from one generation to the next.

- Potential IHT Relief on Business Assets:

- Certain types of trusts, such as business property relief trusts, allow business assets to be transferred while reducing or eliminating inheritance tax liability, particularly if the assets qualify for business relief or agricultural relief.

- Gifting with Trusts:

- Trusts can facilitate tax-efficient gifting. For example, bare trusts allow gifts to minors, and provided the donor survives for 7 years, the assets in the trust won’t be subject to IHT.

- Protection from the 40% IHT Rate:

- Trusts like discretionary trusts allow assets to be held for future beneficiaries without giving them direct access. While discretionary trusts may have their own tax rules, they can offer greater protection and flexibility compared to leaving assets directly, which are taxed at 40%.

- Avoiding Double Taxation:

- Trusts can help avoid double taxation. For example, instead of passing assets directly to children (who may also be liable for IHT later), assets can be placed in a generation-skipping trust, which can reduce IHT when passed on to grandchildren.

By using trusts, individuals can manage their estate more effectively, potentially minimizing inheritance tax liabilities and ensuring assets are distributed according to their wishes. Trusts should be set up with professional advice to ensure they are structured in compliance with tax laws and estate planning goals.

- Trusts can help avoid double taxation. For example, instead of passing assets directly to children (who may also be liable for IHT later), assets can be placed in a generation-skipping trust, which can reduce IHT when passed on to grandchildren.

Do pensions count towards inheritance tax?

In most cases, pensions do not count towards inheritance tax (IHT) in the UK. Here’s a breakdown:

- Defined Contribution Pensions:

- Not subject to IHT.

- If you die before age 75, beneficiaries inherit tax-free.

- If you die after age 75, beneficiaries pay income tax on withdrawals.

- Defined Benefit Pensions:

- Typically, it is not part of your estate for IHT. Survivor pensions are also IHT-exempt.

- Lifetime Annuities:

- Usually die with you unless death benefits are included, which may also be exempt from IHT.

- Drawdown Pensions:

- Remaining funds are not subject to IHT; withdrawals after age 75 are taxed as income.

- Exception:

- Moving pension funds out deliberately to avoid IHT could bring them back into your estate for tax purposes.

In summary, pensions are generally exempt from IHT, making them a tax-efficient way to pass on wealth. Proper planning ensures beneficiaries receive them with minimal tax implications.

Can life insurance cover inheritance tax costs?

Yes, life insurance can be used to cover inheritance tax (IHT) costs. A life insurance policy can be structured to provide your beneficiaries with funds to pay the inheritance tax due on your estate, ensuring they don’t have to sell assets to cover the tax bill.

How it works:

- Whole-of-Life Policy: A whole-of-life insurance policy can be taken out, which guarantees a payout upon death, providing funds to cover IHT costs.

- Writing the Policy in Trust: For the payout to be exempt from IHT, the life insurance policy should be written in trust. This ensures that the payout does not form part of your taxable estate and goes directly to your beneficiaries or an executor to pay the IHT.

- Covering Tax Liabilities: The insurance payout can match the estimated IHT liability, allowing your beneficiaries to cover the tax without selling property or other assets.

Benefits: - Liquidity: Provides immediate funds to pay IHT, avoiding delays or forced asset sales.

- Exempt from IHT: When written in trust, the payout is not subject to inheritance tax.

- Peace of Mind: Ensures your estate passes to your beneficiaries without financial burden.

In summary, life insurance is a practical solution to cover inheritance tax costs, ensuring your assets are passed on as intended without the risk of liquidation.

What is taper relief for inheritance tax on gifts?

Taper relief reduces the amount of inheritance tax (IHT) on gifts made between 3 and 7 years before your death. It applies to gifts that exceed the £325,000 inheritance tax threshold and are subject to tax if you pass away within 7 years of making the gift. The longer you live after making the gift, the lower the tax rate on that gift.

Taper Relief Breakdown:

- Less than 3 years: 40% (full inheritance tax rate)

- 3 to 4 years: 32%

- 4 to 5 years: 24%

- 5 to 6 years: 16%

- 6 to 7 years: 8%

- After 7 years: 0% (no inheritance tax)

Key Points: - Taper relief only reduces the tax on the gift, not the value of the gift itself.

- It applies only if the total value of gifts in the 7 years before death exceeds the IHT threshold.

In summary, taper relief can significantly reduce the tax on large gifts, making gifting an effective estate planning tool if done early.

When does inheritance tax need to be paid?

Inheritance tax (IHT) needs to be paid by the end of the sixth month after the person’s death. If not paid by this deadline, interest will be charged on the amount owed.

Key Points:

- Deadline: IHT must be settled within 6 months of the individual’s death.

- Who Pays: The executor or administrator of the estate is responsible for ensuring the tax is paid.

- Payment in Instalments: If the estate includes assets like property, the tax can be paid in instalments over 10 years, although interest will still accrue on unpaid amounts.

- Advance Payments: Some tax can be paid before the final valuation of the estate is complete to reduce interest charges.

Paying IHT on time is crucial to avoid additional interest costs.

How can I plan effectively to reduce inheritance tax on my estate?

To effectively reduce inheritance tax (IHT) on your estate, consider these strategies:

- Business Property Relief (BPR):

- Invest in qualifying businesses to potentially reduce the IHT on those assets by up to 100%.

- Utilize Gift Allowances:

- Use your annual gift allowance of £3,000 per year (or £6,000 if you didn’t use the previous year’s allowance) to reduce the size of your estate.

- Give small gifts of up to £250 per person, which are exempt from IHT.

- Use your annual gift allowance of £3,000 per year (or £6,000 if you didn’t use the previous year’s allowance) to reduce the size of your estate.

- Make Gifts Early:

- Gifts made more than 7 years before your death are IHT-free, so consider gifting assets early to take advantage of the 7-year rule.

- Use Trusts:

- Place assets in trusts to reduce the value of your estate for IHT purposes. Trusts allow you to pass wealth to beneficiaries while controlling how and when they receive it.

- Maximize Exemptions:

- Leave assets to a spouse or civil partner, as they are exempt from IHT. Additionally, leave assets to charity to avoid IHT and reduce the tax rate to 36% if 10% or more of your estate is donated.

- Residence Nil-Rate Band:

- Pass your home to direct descendants (children or grandchildren) to benefit from the additional £175,000 residence nil-rate band, increasing your tax-free threshold to £500,000 (or £1 million for couples).

- Take Out Life Insurance:

- A life insurance policy, written in trust, can cover the IHT liability, ensuring your beneficiaries do not have to sell assets to pay the tax.

- Pensions:

- Keep funds in your pension, as pensions are usually exempt from IHT and can be passed on to beneficiaries tax-efficiently.

Effective planning with professional advice ensures that your estate is structured to minimize IHT and preserve wealth for your beneficiaries.

Further Information on Accounts & Tax

Our team of specialist accountants and tax experts can help manage, process and structure your business’s finances. From management accounts and payroll & pensions to tax planning and cash flow management, we can take care of the full back-office function of your business.

Book a free, no-obligation consultation with one of the team to find out how we can make your accounts & tax easier, quicker and cheaper.

Make sure you never miss any of our articles, webinars, videos or events by following us on Facebook, LinkedIn, YouTube and Instagram.

Reviewed By:

Arun Mehra

Samera CEO

Arun, CEO of Samera, is an experienced accountant and dental practice owner. He specialises in accountancy, financial directorship, squat practices and practice management.