Income Tax

The 2021/2022 tax year begins 6 April 2021 and ends 5 April 2022 and the following will explain how most individuals will have to pay their income tax:

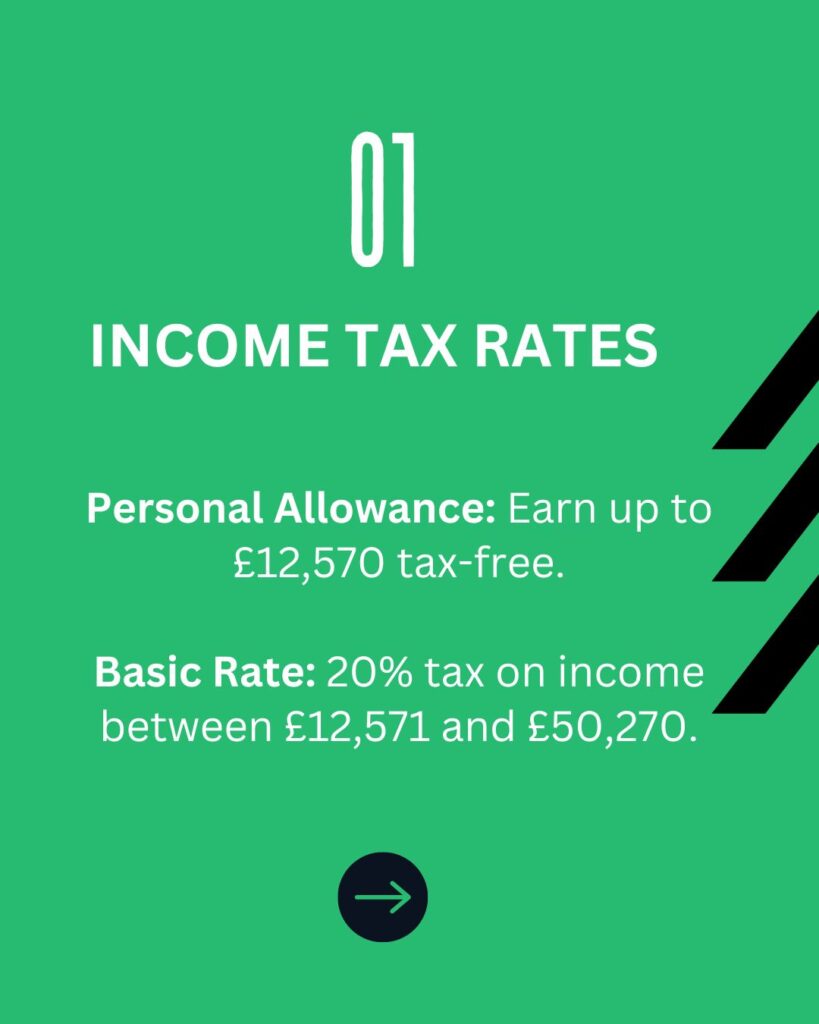

- 0% on the first £12,570 (personal allowance)

- 20% on the next £37,700 (basic-rate band)

- 40% above £50,270 (Higher-rate threshold)

Basic-rate taxpayer explained

Arun earns a salary of £30,000. This is how his income for 2021/2022 can be calculated:

- 0% on first 12,570 = £0

- 20% on the next £17,430 = £3,486

- Total income tax bill = £3,486

Higher-rate taxpayer explained

Arun is a sole trader and had profits of £60,000. This is how his income tax for 2021/22 can be calculated:

0% on first £12,570 = £0

20% on next £37,700 = £7,540

40% on final £9,730 = £3,892

Total income tax bill = £11,432

Read our top 10 tax-saving tips here.

Marriage Allowance

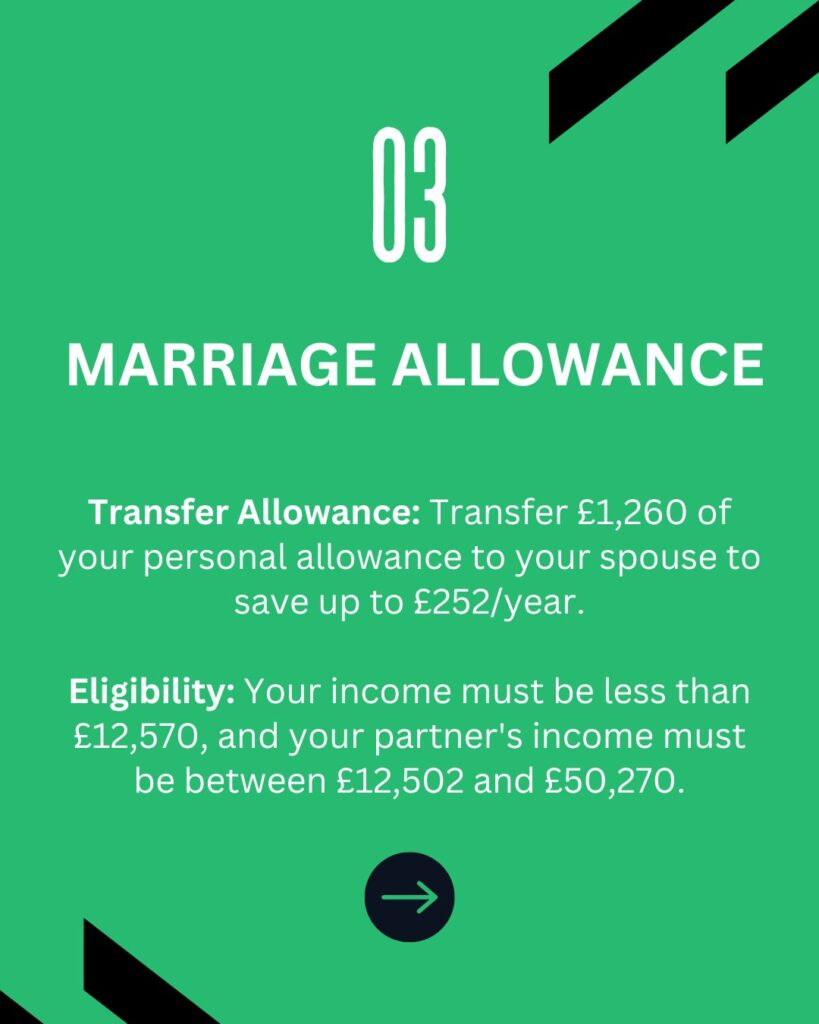

Marriage tax allowance allows you to transfer £1,260 of your personal allowance (this is the same amount you can earn tax-free each tax year) to your spouse or civil partner if they earn more than you. It is free to apply for Marriage Allowance. This can reduce your tax bill by £252 every tax year.

In order to benefit from this allowance as a couple, you need to earn less than your partner and have an income of less than £12,570. Your partner’s income has to range between £12,502 and £50,270 for you to be eligible.

You are able to backdate your claim to include any tax year since 5 April 2017 that you were eligible for Marriage Allowance.

In order to register for Marriage Allowance register at: www.gov.uk/marriageallowance

Different incomes and their tax levels

Income between £100,000 and £125,140

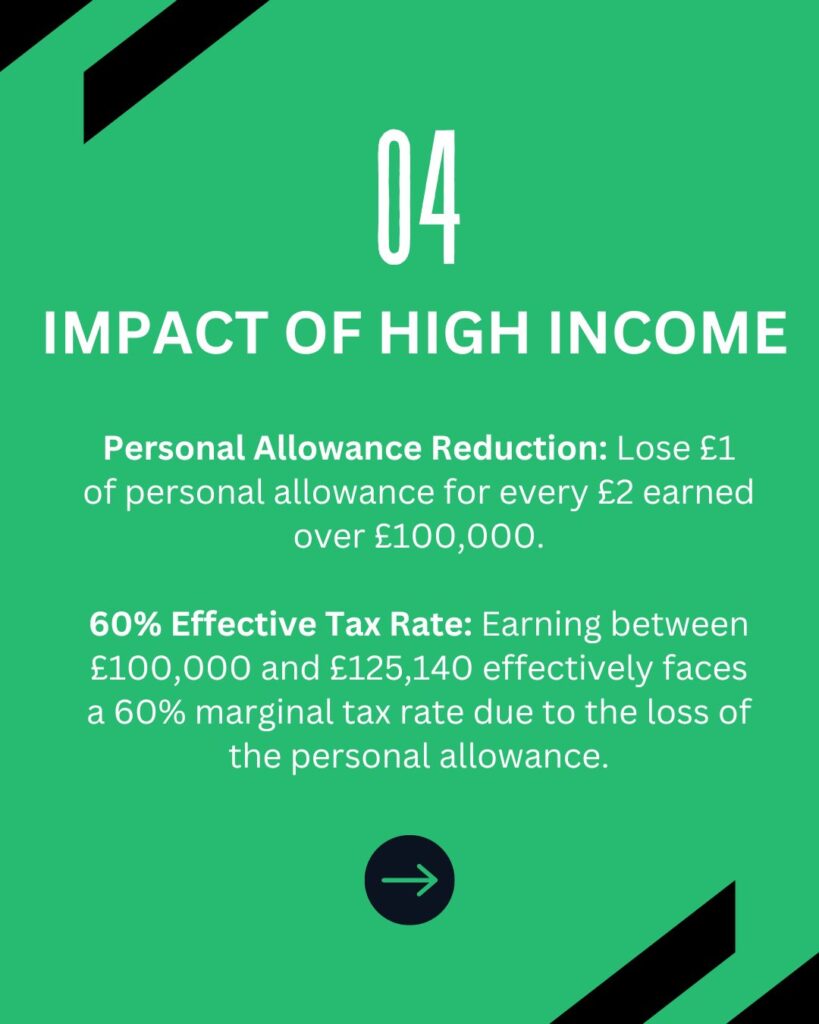

If your income exceeds the £100,00, your personal income tax allowance is gradually taken away from you. The more you earn, the less you get for your personal allowance. It is reduced by £1 for every £2 you earn above £100,000. This means that if your income exceeds £125,140 this year, you will have no personal allowance at all.

It is reduced by £1 every £2 you earn after £100,000.

If you are earning over £100,00 this tax will really take its toll on you.

Paying 60% tax

If you are earning a high income of £100,00 or more, the effect is that anyone earning this or higher will face a hefty marginal income tax rate of 60%.

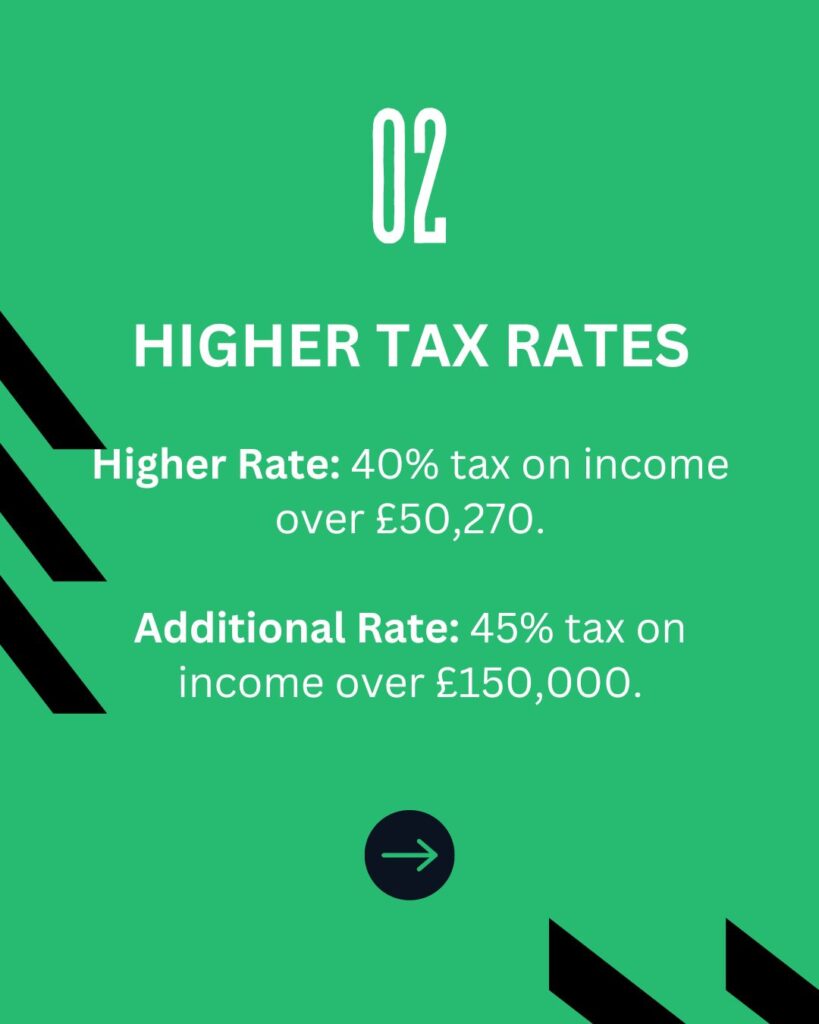

Income over £150,000

Once your income rises above £150,000, you will have to start paying income tax at 45% on most types of your income. This is also known as the additional rate of tax.

You can find out more about how to reduce your tax here.

What income is taxed?

The above tax rates apply to most types on income including:

- Salaries

- Pensions

- Self-employment profits

- Rental profits

- Sole traders and partnerships

Many types of income are also subject to national insurance, whereas some types of income are subject to different income tax rates.

Contact us to find out more

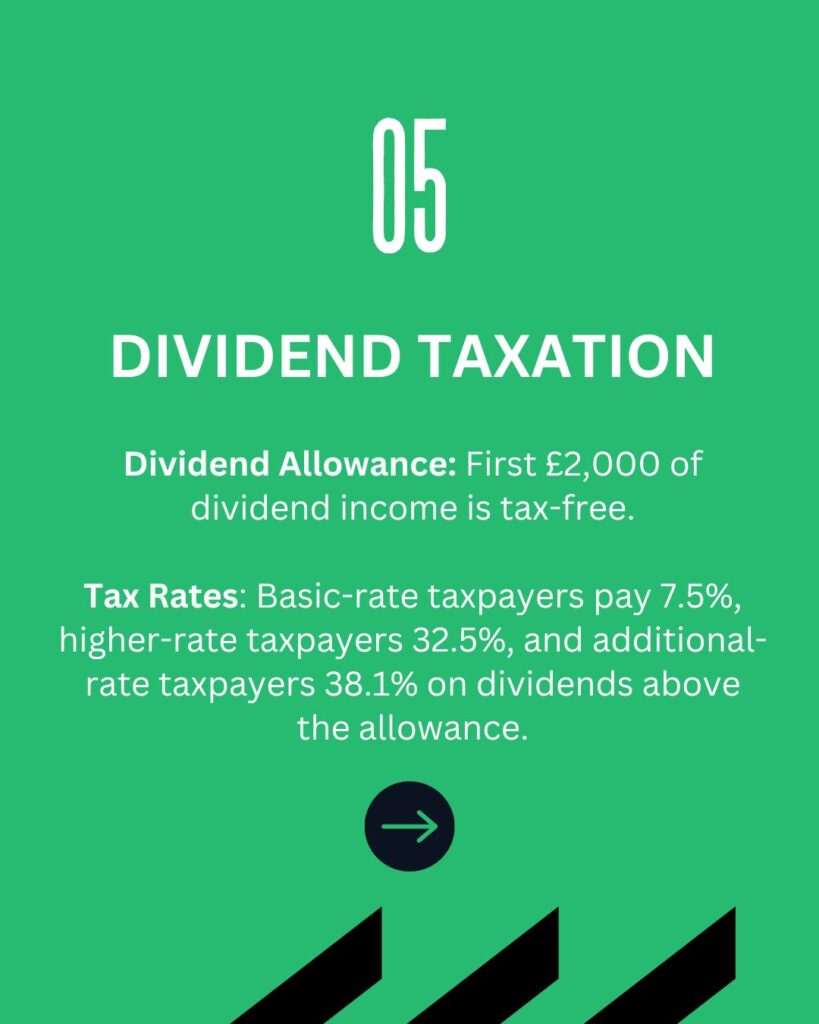

Dividends

Many individuals receive dividends from stock market companies or from their own private companies. You may get dividend payments if you own shares in a company. You can earn some of your dividend income tax free each year.

You do not have to pay tax on any dividend income that falls within your personal allowance. This is the amount of income you earn per tax year that is tax free.

You do not have to pay tax on dividends from share in an ISA or any dividends received from a pension. You also get a dividend allowance each year.

You only pay tax on any dividend income above the dividend allowance.

For dividends that are taxable, the tax rates on those dividends are usually lower than other types of income. This is due to the fact that dividends are paid out after companies’ after-tax profits. This essentially means that dividend income is taxed twice.

Dividend tax credits have been abolished since 2016. Therefore, it is no longer necessary to gross up your dividends to calculate your tax. It is now a lot simpler, as all tax calculations now work with cash dividends.

Although that is great news, it also comes with some bad news: new tax rates for cash dividends have been introduced. These new rates are 7.5% higher than the previous ones. However, due to the ‘dividend allowance’, the first £2,000 dividend income you receive is completely tax free. Regardless of income, all taxpayers can benefit from this allowance.

For those receiving dividends, these following tax rates apply:

- Basic-rate taxpayers: 7.5%

- Higher-rate taxpayers: 32.5%

- Additional-rate taxpayers: 38.1%

These rates will always be subject to the highest possible tax rate as dividends are always treated as the top slice of your income.

Click here to read our blog on 10 tax saving tips for vets.

How dividend allowance works

The dividend allowance is available for anyone (regardless of income) who has dividend income. The dividend allowance means that you will not have to pay tax on the first £5,000 of the dividend income. The dividend allowance is not given as an additional standalone tax-free amount of £2,000.

Instead, it usually uses up some of your basic-rate band of higher-rate band. Dividends aren’t treated as sole income; they are treated as the top addition to your income and is, therefore, taxed at your highest marginal rate. The dividend allowance exempts the bottom £2,000 of that income from tax.

This means that if you have dividend income taxed at both x7.5% and 32.5%, the allowance will exempt some of the income taxed at 7.5%.

The recent changes in dividend tax rates includes an increase that was designed to extract more tax from those company owners who take most of their income as dividends. The main beneficiaries are higher-rate taxpayers and additional-rate taxpayers who receive relatively small amounts of income which is usually accumulated from stock market investments.

Changes in tax laws over the years has meant that if your investments were not stored and sheltered in a pension, an ISA or a capital trust you would have had to pay 25% or 30.6% tax on all dividend income. However, at present, you can receive £2,000 tax free.

Action Points

- Review your dividend income to determine if it falls within the £2,000 dividend allowance for tax-free treatment.

- Understand that the dividend allowance consumes part of your basic or higher-rate tax band, rather than acting as a separate tax-free amount.

- Assess how your dividends are taxed, considering they are added on top of your other income and taxed at your highest marginal rate.

- If applicable, identify portions of your dividend income that may be taxed at different rates (e.g., 7.5% and 32.5%) and apply the allowance to minimize tax liability.

- Stay informed about recent changes in dividend tax rates, especially if you are a company owner who receives significant income through dividends.

- Consider financial planning strategies such as investing in pensions, ISAs, or capital trusts to shelter dividend income from higher tax rates.

Income tax examples

Example 1:

In 2021/22 Brendan has a pension income of £49,270 and dividend income of £6,000.

The first £12,570 of his pension is covered by his personal allowance and the next £36,700 is taxed at 20%.

This leaves him with £1,000 of basic-rate band remaining.

£2,000 of his dividend income is tax free. The first £1,000 uses up what’s left of his basic-rate band (preventing him from paying 7.5% tax), leaving £1,000 of dividend allowance to use in the higher-rate band (preventing him from paying 32.5% tax).

The final £4,000 of dividend income is taxed at the 32.5% higher rate. 10

Example 2:

In 2021/22 Julia has £60,000 of rental income and £3,000 of dividend income. Her rental income uses up her personal allowance and basic-rate band and some of it is taxed at the 40% higher rate.

The first £2,000 of her dividend income is covered by the dividend allowance, leaving £1,000 subject to tax at the 32.5% higher rate.

The dividend allowance does not use up her basic-rate band because none of her dividends fall into the basic-rate band.

Example 3:

In 2021/22 Leon has a £130,000 salary and £50,000 dividend. With this much income his personal allowance is completely withdrawn.

The first £2,000 of his dividend income is covered by the dividend allowance, leaving £18,000 taxed at the 32.5% higher rate. Along with his salary this takes Leon up to the £150,000 additional rate threshold.

The final £30,000 of his dividend income is taxed at 38.1%.

Note, Leon has dividend income taxed at both the higher rate and additional rate. The dividend allowance reduces the amount of his dividend income taxed at the 32.5% higher rate.

Example 4:

In 2021/22 Martin has a £100,000 salary, £50,000 of rental income and £50,000 of dividend income. With this much income his personal allowance is completely withdrawn.

His salary and rental income take him up to the £150,000 additional rate threshold. The first £2,000 of his dividend income is covered by the dividend allowance, leaving £48,000 taxed at the 38.1% additional rate. The dividend allowance reduces the amount of his dividend income taxed at the additional rate.

UK tax on foreign dividends

Buying into shares worldwide is very common these days, particularly within US companies. This impacts your dividend income as these foreign dividends are often subject to withholding tax.

Usually, the overseas company will deduct tax before actually paying you the dividend. It also works in your favour that the UK has double tax treaties with many countries overseas that reduces the amount of payable foreign tax, this is usually between 10% and 15%.

The dividend withholding tax rate in the US is normally 30% but due to the double tax agreement between the UK and US, the amount of withholding tax can now be reduced to 15%. This can be done by completing form W-8BEN, issued by the US Internal Revenue Service (IRS). In many cases, mostly with online investment, stockbrokers will handle these forms for you on your behalf to ensure a smooth process for you.

This double tax agreement also provides a specific exemption for pension schemes. This means that US dividends can be received tax-free if the shares are held inside a pension scheme. If your overseas shares are held outside a pension scheme (e.g., SIPP) or an ISA, your income from your overseas dividends will be subject to UK income tax. The double tax agreement does not recognise ISAs. ISA investors will still be subject to the 15% withholding tax.

You may be able to claim Foreign Tax Credit Relief when you submit your tax return. This allows the overseas tax paid to be deducted from the owed amount of UK tax. However, the amount deducted cannot exceed the UK tax payable on the income.

Contact us to find out more

Interest Income

Personal Savings Allowance

Your Personal Savings Allowance is provided at a 0% tax rate for up to £1,000 of your interest income if you are a basic-rate taxpayer and up to £500 if you are a higher-rate taxpayer. The more you earn, the more your personal saving allowance decreases. Additional rate taxpayers do not receive this allowance.

The amount of income that falls within your savings allowance will still count towards your basic-rate or higher-rate limit and can, therefore, affect the level of savings allowance you are entitled to and the rate of tax payable on any savings income you receive in excess of this allowance.

The starting rate band

There is a 0% starting rate for up to £5,000 of interest income. However, in most cases only those who are on low incomes can use it. You are only able to benefit from this 0% starting rate this tax year if your non-savings income is less than £17,570 (this is £12,570 personal allowance + £5,000 starting rate band). Normally, your non-savings income will include your salary and pensions, but it does not include your dividends.

Many of you reading this probably won’t be able to use the 0% starting rate this is due to you having more than £17,570 of non-savings income. However, there may be another option for you. If you are unable to benefit from starting rate band, you may be able to benefit from the Personal Saving Allowance.

Future income tax changes

Rishi Sunak has promised that after the devasting affects of the pandemic, our government is not going to raise the rates of income tax, national insurance, or VAT. This means that most income tax thresholds and allowances will be frozen until 5th April 2026. This includes:

– Personal allowance £12,570

– Income tax higher rate

Income Tax and National Insurance FAQs

What is income tax?

Income tax is a tax levied by the government on an individual’s earnings, including wages, salaries, and other forms of income. The amount of income tax you pay depends on your total income for the year and is calculated based on specific tax bands and rates. In the UK, income tax is deducted at source through the PAYE (Pay As You Earn) system for employees, or it is paid directly by self-employed individuals through Self Assessment.

How is income tax calculated in the UK?

Income tax in the UK is calculated based on your total income within a tax year, after deducting any personal allowances. Your income is taxed in bands, with different rates applying to each band. The rates increase progressively, meaning higher income portions are taxed at higher rates. The main bands are the basic rate, higher rate, and additional rate. Your employer usually deducts income tax through PAYE, or you pay it directly if self-employed.

What are the current income tax rates and thresholds?

Income tax rates and thresholds in the UK vary depending on your income. For the 2023/24 tax year:

- Personal Allowance: Up to £12,570 (tax-free)

- Basic Rate: 20% on income from £12,571 to £50,270

- Higher Rate: 40% on income from £50,271 to £125,140

- Additional Rate: 45% on income above £125,140

What is National Insurance (NI)?

National Insurance (NI) is a tax in the UK that funds state benefits, including the NHS, state pensions, and unemployment benefits. Employees, employers, and the self-employed pay NI contributions based on their earnings. Different classes of NI apply depending on your employment status, and contributions determine eligibility for certain benefits, such as the state pension.

How does National Insurance differ from income tax?

National Insurance (NI) and income tax are both taxes on earnings in the UK, but they serve different purposes. NI funds state benefits like the NHS and state pensions, while income tax funds general government spending. NI contributions are based on earnings and are paid by employees, employers, and the self-employed. Income tax is calculated on total income and applies at progressive rates depending on income levels. NI contributions also affect eligibility for certain benefits, unlike income tax.

When do you start paying National Insurance?

You start paying National Insurance (NI) when you reach the age of 16 and earn above the minimum earnings threshold. For the 2023/24 tax year, this threshold is £242 per week for employees and £12,570 annually for the self-employed. Contributions are made through your pay if you’re employed or via Self-assessment if you’re self-employed.

What are the different classes of National Insurance?

There are several classes of National Insurance (NI):

- Class 1: Paid by employees and employers based on earnings.

- Class 1A/1B: Paid by employers on employee benefits.

- Class 2: A flat rate paid by self-employed individuals earning above a certain threshold.

- Class 3: Voluntary contributions to fill gaps in NI records.

- Class 4: Paid by self-employed individuals based on profits.

How can I check my income tax and National Insurance contributions?

You can check your income tax and National Insurance contributions through your personal tax account on the HMRC website. This account lets you view your tax payments, and contributions history, and update your details. You can also see how much tax you’ve paid and what you owe, and request refunds if applicable.

Can I claim relief on income tax?

Yes, you can claim income tax relief in the UK through various allowances and deductions. Common forms of relief include Personal Allowance, Marriage Allowance, and pension contributions. Charitable donations, job-related expenses, and investment-related reliefs like the Enterprise Investment Scheme (EIS) can also reduce your tax liability. To claim these, you may need to submit a self-assessment tax return or inform HMRC directly.

What happens if I don’t pay National Insurance?

If you don’t pay National Insurance (NI) when required, you may face penalties, interest on unpaid contributions, and loss of eligibility for certain state benefits like the state pension and maternity allowance. HMRC may also take enforcement action to recover unpaid amounts. Keeping up with NI payments is crucial to avoid these consequences.

How does self-employment affect income tax and National Insurance?

Self-employment affects income tax and National Insurance (NI) by requiring you to pay both through the Self Assessment process. You pay income tax on your profits after deducting allowable business expenses. For NI, you’ll pay Class 2 contributions if your profits exceed a certain threshold, and Class 4 contributions based on a percentage of your profits. You must keep accurate records and submit an annual tax return to HMRC.

What is PAYE, and how does it relate to income tax?

PAYE (Pay As You Earn) is a system used by HMRC to collect income tax and National Insurance directly from your wages or pension. Your employer deducts these amounts from your salary before you get paid and sends them to HMRC on your behalf. This ensures that you pay the correct tax throughout the year based on your income, reducing the need for additional payments or refunds at the end of the tax year.

How do pension contributions affect income tax?

Pension contributions can reduce your taxable income, thereby lowering the amount of income tax you pay. Contributions are often made before tax is applied (through salary sacrifice) or eligible for tax relief if paid directly into a personal pension. This means you effectively get back the tax you would have paid on that portion of your income, depending on your tax rate

What is a tax code, and how does it work?

A tax code is a series of numbers and letters used by HMRC to determine how much income tax should be deducted from your pay or pension. It reflects your tax-free allowance and any adjustments for other income, benefits, or tax underpayments. The most common tax code is 1257L, indicating that you’re entitled to the standard tax-free Personal Allowance. Your employer uses this code to calculate the tax to deduct under the PAYE system.

How are bonuses taxed in the UK?

In the UK, bonuses are taxed as part of your income, meaning they are subject to the same income tax and National Insurance contributions as your regular salary. The bonus is added to your salary for the tax year and taxed according to your income tax band. Depending on your tax code and income, your bonus could push you into a higher tax bracket, resulting in a higher tax rate on the bonus amount.

What should I do if I overpay income tax?

If you overpay income tax in the UK, you can request a refund from HMRC. This can be done by completing a self-assessment tax return or by using HMRC’s online service. HMRC will review your case and, if an overpayment is confirmed, they will issue a refund either through your bank account or by check.

Can I claim back National Insurance contributions?

In most cases, you cannot claim back National Insurance contributions, as they are used to fund state benefits like the NHS and state pensions. However, if you overpay due to an administrative error or if you paid NI while earning below the threshold, you can apply for a refund. You would need to contact HMRC to review your contributions and process any refund due.

How do tax-free allowances work?

Tax-free allowances in the UK reduce the amount of your income that is subject to tax. The most common is the Personal Allowance, which allows you to earn a certain amount each year (currently £12,570) tax-free. Other allowances include the Marriage Allowance, which lets one spouse transfer part of their unused allowance to the other, and the Dividend Allowance, which is tax-free income from dividends up to a certain limit.

What is a P60 and how is it used?

A P60 is an end-of-year tax document provided by your employer that summarizes your total earnings and the tax and National Insurance contributions you’ve paid during the tax year. It’s essential for confirming your income and tax payments, and it can be used to claim tax refunds, apply for tax credits, or verify your tax records. You should keep your P60 for at least 22 months after the end of the tax year.

What is the impact of tax bands on my earnings?

Tax bands in the UK determine the rate at which your income is taxed. As your income increases, portions of it fall into different bands with progressively higher tax rates. The basic rate (20%) applies to income up to £50,270, the higher rate (40%) to income between £50,271 and £125,140, and the additional rate (45%) to income above £125,140. These bands impact your overall tax liability, with higher earners paying more tax on their income.

Learn more: Related Articles

About the Author

Arun Mehra

With almost twenty years of commercial experience and knowledge in Dentistry, Arun’s expertise is valued by hundreds of businesses across the UK. His financial acumen and know-how, along with his hands-on commercial expertise have helped clients, large and small, new and established to achieve great things.

Arun is the founder of the Samera Group, starting the business with just one client sitting at his father’s dining table. Fifteen years on, Team Samera now service hundreds of Dental clients, run exciting events, help clients raise finance, and are very active in helping clients buy or sell Dental practices.

Further Information on Accounts & Tax

Our team of specialist accountants and tax experts can help manage, process and structure your business’s finances. From management accounts and payroll & pensions to tax planning and cash flow management, we can take care of the full back-office function of your business.

Book a free, no-obligation consultation with one of the team to find out how we can make your accounts & tax easier, quicker and cheaper.

Make sure you never miss any of our articles, webinars, videos or events by following us on Facebook, LinkedIn, YouTube and Instagram.