Most companies will generally pay corporation tax on both their income as well as their capital gains tax.

For the financial year beginning on 1st April 2021, all companies (except for those in the oil and gas sector) will pay the same flat rate of 19% corporation tax. This rate will also continue into the financial year of 2022.

In 2023, the corporation tax rate will increase to 25% which was announced during March 2021.

You must pay Corporation Tax on profits form doing business as:

- A limited company

- A club, co-operative, or any unincorporated association

- Any foreign company with a UK office or branch

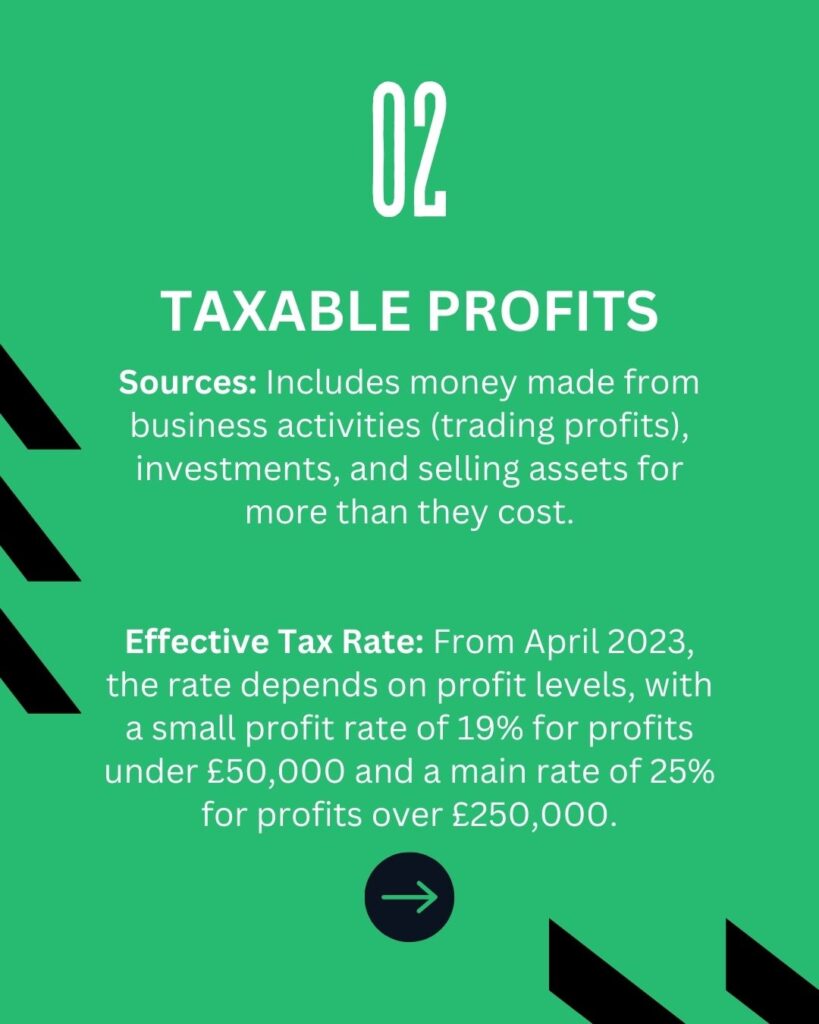

Profits you pay Corporation Tax on

Taxable profits for Corporation Tax include the money your company makes from:

- Investments

- Doing business (trading profits)

- Selling assets for a profit

Calculating Your Company’s Effective Tax Rate

From April 2023 corporation tax will not only get increased, but it will also become a bit more complicated. There will be two official corporation tax rates:

- Small profits rate: 19%

- Main rate 25%

Companies with taxable profits of £50,000 or less will continue to pay 19% tax on all their profits. Companies with taxable profits of more than £250,000 will pay 25% tax on all their profits.

If profits are between £50,000 or £250,000 a ‘marginal relief’ calculation will be made. The practice effect of this is that there will effective be three different corporation tax rates:

First £50,000: 19%

Between £50,000 and £250,000: 26.5%

Over £250,000: 25%

Multiple Companies

There are many company owners who think about setting up a second company which is separate from their existing business. Often there are a few commercial reasons for using more than one company including:

- Reducing risk and limiting liability

- Involve different shareholders

- Enable a stand-alone sale of each business

With corporation tax increasing in the near future, it is possible for multiple companies with one owner, enjoying up to £50,0000 of profit taxed at 19%. However, in order to achieve this the companies must not be associated companies.

Contact us to find out more

Associated Company Rules

When the new corporation tax rates come into operation within the next couple of years, to prevent people artificially spreading their business activities across multiple companies, the £50,000 lower limit and £250,000 upper limit will be divided up if there are any associated companies.

A company will only be associated with another company if:

- One company controls the other company

- Both are under the control of the same person / people

Family Members and Business Partners

When deciding who controls a company, your associates interests are treated as your own if there is substantial commercial interdependence between the companies.

Business associates include:

- Your spouse or civil partner

- Close relatives

- Legal business partners

Trading Companies vs Investment Companies

A trading company is essentially a company that is involved in regular business activities such as a company that sells goods online or a catering company or a firm. Common types of non-trading companies include those that hold substantial investments in financial securities or property or earn substantial royalty income.

Corporation Tax

If your company is mainly engaged in non-trading activities, in 2021 it will be paying corporation tax at the same rate as most other companies (19%). However, when the new corporation tax rates come into effect, a lot of these investment companies will have to pay the main rate of corporation tax which will be a rate of 25% on all their profits.

This is because any company classed as a close investment holding company (CIC) will not be able to benefit from the small profits rate of 19%. The company will be forced to pay corporation tax at the main rate on all profits.

Companies that mainly derive their profits from renting properties to unconnected third parties (not to family members, etc) are excluded from the CIC provisions. Hence, the majority of property investment companies will be allowed to enjoy the small profits rate.

If a company has too many non-trading activities (including most property investment and property letting) it may lose its trading status for capital gains tax purposes. This will result in the loss of two important CGT reliefs:

- Business Asset Disposal Relief

- Holdover Relief

Business Asset Disposal Relief

Business Asset Disposal Relief allows you to pay capital gains tax at just 10% (instead of 20%) when you sell your company.

Holdover Relief allows you to give shares in the business to your children, common-law unmarried partner, or other individuals and postpone CGT. You do not need Holdover Relief to transfer shares to your spouse because such transfers are always exempt.

A company will only lose its trading status for CGT purposes if it has ‘substantial’ non-trading activities. Unfortunately to HMRC ‘substantial’ usually means as little as 20% of various measures such as:

- Expenses

- Assets

- Profits

- Turnover

- Directors’ and employees’ time

HMRC may attempt to apply the 20% rule to any of the above measures.

Inheritance Tax Shares in trading companies usually qualify for business property relief. This means they can be passed on free from inheritance tax. However, if the company holds investments (including any rental properties), this could result in the loss of business property relief.

The qualification criteria are more generous than for CGT purposes and a company generally only loses its trading status for inheritance tax purposes if it is either wholly or mainly involved in investment related activities. To be on the safe side you will want to ensure that the company’s qualifying activities exceed 50% of each of the measures listed above (e.g. turnover, time, profits etc).

Companies registered as Tax Shelters Corporation tax is often a lot lower than the income tax and national insurance paid by sole traders and partnerships. Companies don’t always pay less tax than self-employed business owners but, as profits increase, the tax savings also naturally increase.

A business owner will therefore potentially have a lot more after-tax profit left to reinvest. Companies are normally most powerful as tax shelters when profits are reinvested. Most company owners need to extract money for their own personal use. At this point additional tax may be payable. The income tax payable on dividends reduces the tax benefits of using a company in many cases.

Learn more: Related Articles

Frequently Asked Questions Corporation Tax

What is Corporation Tax, and who is required to pay it?

Corporation Tax is a tax that companies and organizations must pay on their profits. In the UK, any company operating as a limited company, including dental practices, is required to pay Corporation Tax on taxable profits. This includes profits from trading, investments, and the sale of assets. The amount owed depends on the company’s income, allowable expenses, and applicable tax reliefs. Ensuring accurate and timely filing is essential to avoid penalties from HMRC.

How is Corporation Tax calculated for dental practices?

Corporation Tax for dental practices is calculated based on taxable profits, which include income from dental services, investments, and the sale of assets. To determine the tax owed, subtract allowable business expenses, capital allowances, and any reliefs (such as R&D credits) from total income. The remaining profit is taxed at the current Corporation Tax rate. It’s important for dental practices to accurately track income and expenses to ensure correct calculations and timely payments to HMRC.

What are the key deadlines for Corporation Tax payments?

Corporation Tax deadlines include filing your company’s tax return with HMRC within 12 months after your accounting period ends. However, payment of Corporation Tax is due 9 months and 1 day after the end of your accounting period. Late payments or filings can result in penalties and interest charges. It’s essential to stay organized and ensure timely submissions to avoid additional costs.

Can I reduce Corporation Tax through allowable expenses?

Yes, you can reduce Corporation Tax through allowable expenses. These are costs that are essential for running your dental practice, such as salaries, rent, dental supplies, and professional fees. By deducting these expenses from your total income, you reduce your taxable profit, leading to a lower Corporation Tax bill. It’s important to keep accurate records and ensure that all expenses claimed are legitimate and comply with HMRC rules.

How do capital allowances impact Corporation Tax?

Capital allowances allow businesses, including dental practices, to deduct the cost of certain assets like dental equipment from their taxable profits, reducing their Corporation Tax bill. These allowances are applied to assets like machinery, vehicles, and office equipment. By claiming capital allowances, businesses can offset the purchase cost over several years or all at once (depending on the type), lowering the taxable income and, in turn, the Corporation Tax owed.

What is the difference between Corporation Tax and income tax for business owners?

Corporation Tax is paid by limited companies on their profits, while income tax is paid by individuals on their personal earnings. For business owners, Corporation Tax applies to the profits made by the company, and income tax applies to any salary or dividends they take from the business. The rates and rules for both taxes differ, with Corporation Tax often being lower than higher-rate income tax, offering potential tax savings for business owners who structure their income efficiently.

Are dividends subject to Corporation Tax?

Dividends themselves are not subject to Corporation Tax, as they are paid out of the company’s post-tax profits. This means the company pays Corporation Tax on its profits before distributing dividends to shareholders. However, when shareholders receive dividends, they may be liable to pay personal income tax on those dividends, depending on their tax bracket and the amount received. This setup allows for potential tax efficiencies when compared to taking a salary.

How can dental practices optimize their tax structure for Corporation Tax savings?

Dental practices can optimize their tax structure for Corporation Tax savings by claiming all allowable expenses, including dental supplies and staff salaries, and utilizing capital allowances for equipment purchases. Incorporating the practice can also provide tax benefits by allowing owners to take dividends instead of a full salary, which may be taxed at a lower rate. Strategic tax planning, such as pension contributions and taking advantage of R&D tax credits, further reduces taxable profits, leading to significant savings.

What happens if I miss the Corporation Tax deadline?

If you miss the Corporation Tax deadline, HMRC will impose penalties and interest charges. The initial fine for late filing starts at £100, with increasing penalties if further delays occur. Interest will also accrue on any unpaid tax. Continued non-compliance can lead to more severe financial penalties, so it’s crucial to meet deadlines or contact HMRC if you’re unable to pay on time.

How does the Annual Investment Allowance affect Corporation Tax?

The Annual Investment Allowance (AIA) allows dental practices and businesses to deduct the full cost of qualifying equipment, like dental chairs or machinery, from their taxable profits in the year of purchase. This reduces the amount of Corporation Tax owed by lowering taxable income. The AIA has an annual cap, so planning purchases to fall within the allowance can maximize tax savings and improve cash flow.

Can losses be carried forward to reduce Corporation Tax?

Yes, losses can be carried forward to reduce Corporation Tax in future years. If a dental practice incurs trading losses, those losses can be applied to offset future taxable profits, reducing the amount of Corporation Tax owed in subsequent periods. This helps businesses manage cash flow and tax liabilities more effectively by spreading out the impact of losses over time. Accurate record-keeping and timely filing are essential to utilize this benefit.

How can incorporating a dental practice reduce overall tax liability?

Incorporating a dental practice can reduce overall tax liability by allowing the practice to pay Corporation Tax on profits, which is often lower than personal income tax rates. Owners can also take dividends, which are taxed at a lower rate than salaries, resulting in further tax savings. Additionally, incorporation offers opportunities to claim more expenses, capitalize on tax reliefs like pension contributions, and structure income more efficiently, leading to significant reductions in taxable income.

What are the rates of Corporation Tax for small vs. large businesses?

As of 2023, the standard UK Corporation Tax rate is 25% for businesses with profits above £250,000. For small businesses with profits below £50,000, the rate is 19%. A tapered rate applies for profits between £50,000 and £250,000, where companies pay a marginal rate. These rates affect how businesses, including dental practices, calculate their tax liabilities, and proper tax planning can help optimize the amount owed.

What financial records must be kept for Corporation Tax compliance?

Income and expense records: All business transactions, such as sales invoices and purchase receipts.

- Payroll records: Documentation of staff wages and benefits.

- Asset records: Details of equipment and property purchased for the business.

- Bank statements: Evidence of business account transactions.

- VAT records: If applicable, keep VAT returns and related documents.

These records should be retained for at least six years for HMRC auditing purposes

How do pension contributions affect Corporation Tax for a company?

Pension contributions made by a company reduce its taxable profits, leading to lower Corporation Tax. Contributions to employee pensions are treated as allowable business expenses and can be deducted from the company’s income before Corporation Tax is calculated. This provides both a tax-efficient way to support employees and a method for the business to reduce its overall tax liability. Contributions to the directors’ pensions can also be structured for tax efficiency.

What is the role of R&D tax credits in reducing Corporation Tax?

R&D (Research and Development) tax credits allow companies, including dental practices, to claim relief on expenses related to innovation and development. Qualifying R&D activities can result in a reduction of Corporation Tax by either lowering taxable profits or providing a payable credit for loss-making companies. This tax incentive encourages businesses to invest in improving processes, developing new treatments, or innovating equipment, potentially leading to significant tax savings.

How do I calculate taxable profits for Corporation Tax?

To calculate taxable profits for Corporation Tax, start by determining your company’s total income, including revenue from services, investments, and asset sales. Next, subtract allowable expenses, such as salaries, rent, dental supplies, and other operating costs. You can also deduct capital allowances for equipment purchases and any applicable reliefs like R&D tax credits. The remaining amount is your taxable profit, which is then subject to the appropriate Corporation Tax rate.

What qualifies as allowable expenses for Corporation Tax deductions?

Allowable expenses for Corporation Tax deductions include costs necessary for running a business, such as salaries, rent, utilities, office supplies, dental equipment, and marketing expenses. Other qualifying expenses include professional fees, insurance premiums, training costs, and travel expenses for business purposes. Capital allowances can also be claimed on equipment and machinery. However, non-business expenses, like personal costs or entertainment, are not deductible.

What are the common pitfalls in Corporation Tax filing and how to avoid them?

Common pitfalls in Corporation Tax filing include miscalculating taxable profits, failing to claim all allowable expenses, and missing important deadlines, which can lead to penalties. Other issues involve inaccurate record-keeping, not accounting for capital allowances, and misunderstanding tax reliefs like R&D credits. To avoid these, ensure thorough record maintenance, use accounting software to track income and expenses, and work with a tax advisor to stay compliant and maximize tax savings.

How can a tax advisor help reduce Corporation Tax for a dental practice?

A tax advisor can help reduce Corporation Tax for a dental practice by identifying all eligible deductions, such as allowable expenses and capital allowances. They can also ensure the practice claims available tax reliefs, such as R&D tax credits, and optimize the business structure for tax efficiency. Additionally, a tax advisor can provide strategic planning around pension contributions, dividends, and other financial decisions to minimize the overall tax burden while staying compliant with HMRC regulations.

About the Author

Arun Mehra

With almost twenty years of commercial experience and knowledge in Dentistry, Arun’s expertise is valued by hundreds of businesses across the UK. His financial acumen and know-how, along with his hands-on commercial expertise have helped clients, large and small, new and established to achieve great things.

Arun is the founder of the Samera Group, starting the business with just one client sitting at his father’s dining table. Fifteen years on, Team Samera now service hundreds of Dental clients, run exciting events, help clients raise finance, and are very active in helping clients buy or sell Dental practices.

Further Information on Accounts & Tax

Our team of specialist accountants and tax experts can help manage, process and structure your business’s finances. From management accounts and payroll & pensions to tax planning and cash flow management, we can take care of the full back-office function of your business.

Book a free, no-obligation consultation with one of the team to find out how we can make your accounts & tax easier, quicker and cheaper.

Make sure you never miss any of our articles, webinars, videos or events by following us on Facebook, LinkedIn, YouTube and Instagram.