In this guide, we’ll walk you through the key things to check for when you’re looking at potential dental practices to buy. Whether you’re an experienced associate finally ready to buy your own practice, looking to start a dental group or you’re just starting to explore your options, here are the different things you need to consider when looking for the perfect practice.

Key Takeaways

- Location is everything – A good postcode can make or break your success.

- Know your patients – Demographics, activity levels, and patient types reveal the real value.

- Check the finances – EBITDA, turnover, and overheads must all add up.

- Reputation matters – Patient loyalty, online reviews, and brand recognition are priceless.

- Staff stability counts – A happy, experienced team makes your life easier.

- Inspect the setup – Facilities, equipment, and digital readiness can impact your day-to-day.

- Understand the model – NHS, private, mixed, or squat, choose what suits your strengths.

- Do your homework – Legal, compliance, and past issues can haunt your future.

- Think long-term – Growth potential through new services and marketing is a real asset.

It’s All About Location

You’ve probably heard it a hundred times and there’s a good reason for it. Location isn’t just about a dot on a map. It’s about the people who live there, how they live, and whether your future practice fits in with that lifestyle.

Know Your Neighbours: Demographics

Start by getting to know the people in the area. Is it a family-friendly suburb where patients will need regular check-ups, specialties for children and hygiene visits? Or a busy city centre where cosmetic treatments like whitening and veneers are in high demand?

Knowing who lives nearby helps you work out what kind of services will be popular. For instance, if you specialise in implants or high-end cosmetic work, setting up in a quiet rural town with tight budgets might not work out. But if you’re planning to run a busy NHS practice, areas with higher population density and modest incomes could be just right.

How Easy Are You to Find? Footfall & Visibility

You might be the top dentist in town, but it won’t help much if people can’t find your practice. Take a good look at how easy it is to spot and get to. Is it on a main road with plenty of foot traffic, or tucked away down a quiet street with no signs and nowhere to park?

Transport links matter too. Can patients get to you by bus or train? Is there parking nearby? Can they reach you without any stress? These practical things really do affect how many people walk through your door.

Also, think about the layout of the building. Being on the ground floor is a big plus, it’s easier to see from the street and much more accessible for older patients, wheelchair users, or anyone who finds stairs a challenge. Let’s be honest no one wants to hike up a flight of stairs just to get their teeth checked.

Is the Area Right for You? Lifestyle Match

It’s not just about your patients, it’s about your life too. What’s the cost of living like in the area? Could you see yourself living nearby, settling into the community, and dealing with the daily commute?

A quick tip: Don’t just fall for the practice, make sure you like the postcode as well.

Patient Numbers & Demographics

A dental practice isn’t just about buildings and equipment it’s about the people who walk through the door. Your patients are the heart of the business, so it’s important to understand who they are and how often they actually come in.

How Active Is the Patient List?

It’s not just about how many patients are on the books, but how many of them are truly active. That means they’ve had an appointment in the last 12 to 24 months. A big list might sound great, but if half the names haven’t visited since 2019, it doesn’t mean much in real terms.

Are New Patients Signing Up?

Is the practice regularly welcoming new patients? A steady flow of new bookings is a strong sign the practice is growing, visible, and trusted in the community. If that number’s dropped, ask why. Is it a lack of marketing? Or has the practice’s reputation taken a hit?

Who Are the Patients?

Take a closer look at the type of patients the practice serves. Is it mostly NHS, private, or a mix of both? Are people coming in for routine check-ups, or are they looking for cosmetic work and high-end treatments? If there is an aging patients you may want to think more about implantology. If is the area is family-focused then orthodontics might be more profitable.

Knowing the kind of patients the practice attracts can help you understand its earning potential and whether it fits with the type of dentistry you enjoy doing.

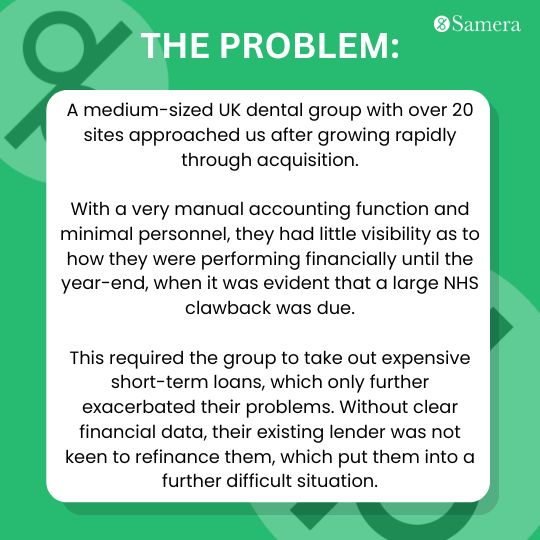

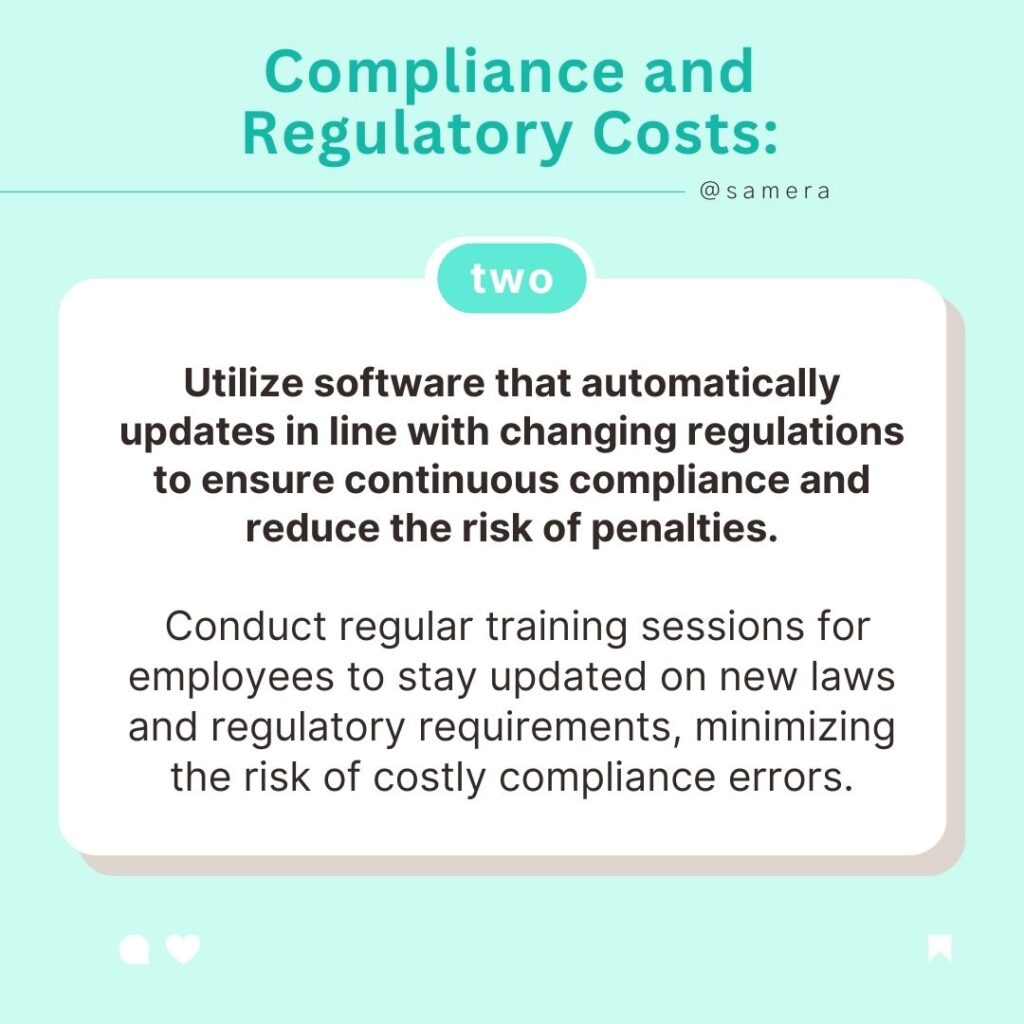

Financial Health Check

Time for the not-so-glamorous but very important bit, the finances. Because if the numbers don’t add up, the rest simply doesn’t matter.

EBITDA – What’s That?

EBITDA stands for Earnings Before Interest, Tax, Depreciation, and Amortisation. It’s a fancy name for a simple idea, how much real profit the practice makes before all the complicated accounting stuff. This number gives you a clear picture of the business’s performance and it’s the one lenders will focus on, so you should too.

Turnover Trends

Look at how much money the practice has brought in over the past three to five years. Is income going up steadily? Staying flat? Or dropping? A healthy upward trend shows the business is stable and growing. Sudden ups and downs could mean poor management or unreliable patient numbers.

Overheads – What’s Being Spent?

It’s great if a practice earns well but not if it spends even more. Take a close look at running costs like staff wages, lab fees, materials, rent, and maintenance. These all eat into your profit. Make sure you know exactly where the money goes before you sign anything.

Red Flag: If the income looks good but the expenses are sky-high, you might be walking into a financial headache, not a successful business. Make sure you do your due diligence to figure out what is going on.

Goodwill and Reputation

You won’t find it on a balance sheet, but a practice’s reputation is just as important as its profits. What people think and say about the place can make or break your success.

Patient Loyalty

Are patients coming back because they trust the team and feel looked after or just because there’s no other option nearby? A loyal patient base is a real asset, especially if the current owner is stepping away. Ask about recall rates and how long patients have been coming. If people have stuck around for years, that’s a great sign.

What’s the Word on the Street (and Online)?

These days, Google reviews and social media comments speak volumes. What are people saying? Are the reviews recent and positive? Good feedback shows that the practice is trusted and has built strong relationships in the community.

Don’t panic if you see a few negative reviews, no business is perfect. But pay attention to what they’re about. They can tell you where things might need improving. Depending on how you approach your new practice, this could be a hindrance or an opportunity.

Brand Recognition

Is the practice well-known locally? Does it have a strong name, clear branding, and a good reputation? Or is it just another faceless clinic on the high street?

A trusted, recognisable brand helps keep existing patients and attract new ones. If the brand’s forgettable, you might have to invest time (and money) into refreshing its image.

Did You Know!

- Location Significantly Influences Patient Choices: Patients often prioritize convenience when selecting a dental practice. Factors like proximity to home or work and ease of access can heavily influence their decisions. (Source)

- Demographics Affect Appointment Attendance: Studies have shown that appointment cancellations and no-shows are more prevalent among certain demographic groups, such as young adults aged 19 to 24 and individuals from low to mid-range socioeconomic backgrounds. (Source)

- Modern Equipment Enhances Patient Experience: Investing in the latest dental technology not only improves treatment efficiency but also enhances patient comfort, particularly for those with dental anxieties. (Source)

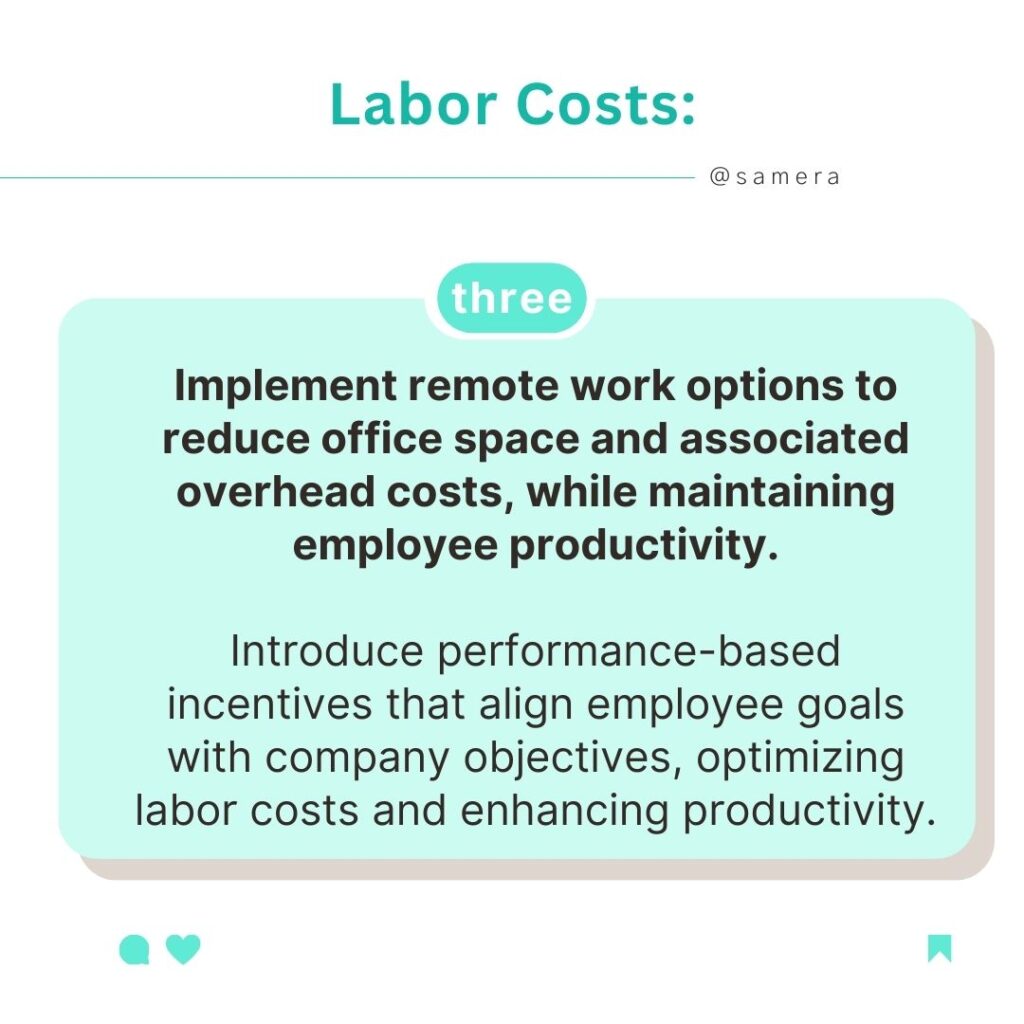

Team Dynamics

When you buy a dental practice, you’re not only getting the equipment and patient list, you’re also inheriting the staff. And that can be a real blessing … or a bit of a headache.

How Often Do Staff Leave?

If people are constantly leaving and being replaced, it could be a red flag. It might point to poor management, low morale, or a bad working atmosphere. But if the same team has been around for years, it usually means things run smoothly, and the staff are happy.

Who Does What – and How Well?

Take time to find out who’s in the team. How experienced are the dental nurses, receptionists, and practice manager? Are they well-trained and genuinely care about the practice, or are they just there to get through the day?

A strong, reliable team will make your handover much easier and give you peace of mind as you settle in.

Know the Rules: TUPE

Under something called TUPE (Transfer of Undertakings), staff have legal rights when a business is sold. You’ll need to keep them on under the same terms and conditions. So before you take over, make sure you’re happy to work with the existing team.

Facilities & Equipment

The space you’re buying isn’t just walls and floors it’s where you’ll build your future. So it’s worth checking everything properly before you commit.

What Shape Are the Surgeries In?

Are the treatment rooms clean, modern, and in good working order? Or do they look worn out and in need of a full refurb? A tired-looking practice can put patients off and refurbishing can cost a lot more than you think.

Take a close look at the plumbing, ventilation, and infection control setup too. Don’t just glance around, get a proper inspection done.

Is the Practice Up to Date Digitally?

Do they use electronic patient records, digital X-rays, and an online booking system? Or are they still flicking through dusty paper files?

A digital setup makes everything faster, smoother, and more secure. It also helps you stay compliant with regulations and ready to grow.

Can You Expand?

Is there space to add another surgery, a consultation room, or extra services in future? If the practice is already bursting at the seams, it might hold back your plans for growth.

Type of Practice

When choosing a practice, think about what suits your experience, goals, and how much risk you’re happy to take on. Different practice models come with different pros and cons.

Types of Practice Models

- NHS: Brings steady income, but comes with strict rules and targets you have to meet.

- Private: Offers more earning potential, but you’ll need strong marketing and patient loyalty to keep things going.

- Mixed: Gives you a bit of both—though it often means extra admin and more juggling.

- Squat: You’re starting from zero. It’s a big risk, but if you get it right, the rewards can be huge.

Choose a model that matches your skills and what you’re comfortable managing.

Read the Small Print

If you’re looking at an NHS contract, check the details carefully. What’s the UDA (Units of Dental Activity) target? Is it realistic? Are there fines if you don’t hit it?

Make sure you fully understand what you’re agreeing to and what’s expected of you.

Legal & Compliance Checkpoints

Before you buy, make sure you’re not walking into a mess. Do a proper check on the practice’s background especially anything to do with rules and regulations.

Check the CQC Report

Look up the latest Care Quality Commission (CQC) report. Have there been any warnings, missed standards, or issues during inspection? If there are problems, they’ll need sorting before you take over otherwise, they’ll become your headache.

Are You Buying or Renting?

Find out if the property is freehold (you own the building) or leasehold (you’re renting it). If it’s leasehold, check how long the lease runs for and whether there are any tricky clauses. Things like rent increases or restrictions could affect your long-term plans.

Any Past Issues with the NHS, CQC, or GDC?

Ask directly about NHS clawbacks, these are repayments you might have to make if the practice missed its UDA targets. Also ask if there have been any warnings or disciplinary actions from the CQC or GDC. If something went wrong before, make sure it won’t come back to bite you.

Digital Footprint

In today’s world, a strong online presence can make a big difference especially if you’re running a private or cosmetic practice where first impressions count.

Website & Social Media

Take a look at the practice’s website. Is it modern, easy to use, and mobile-friendly? What about their social media, are the pages active, up to date, and professional?

If things look old-fashioned or rarely updated, it could mean they’re missing out on new patients or giving off the wrong impression altogether.

How Are They Marketing Themselves?

Ask how the practice promotes itself. Do they use things like Google Ads, Facebook campaigns, or local search engine optimisation (SEO)? Or do they just rely on word of mouth and the odd flyer?

If there’s no real marketing plan, don’t worry it’s not the end of the world. But it does mean there’s room to grow.

Growth Potential

When you buy a practice, you’re not just paying for what’s already there, you’re investing in what it could become.

Unused Services

Does the practice currently offer things like facial aesthetics, implants, orthodontics, or hygiene therapy? If not, and you have those skills, there’s a real chance to grow the business by adding new services.

Sometimes the best practices aren’t the polished ones, they’re the ones waiting for someone like you to take them to the next level.

Room to Grow

Can the business grow with you? Could you extend the opening hours, bring in new associates, or invest in new equipment or tech?

Don’t just look for a perfect setup, look for potential you can build on.

Conclusion

Buying a dental practice isn’t just ticking a business box, it’s about building your future. Every patient, every number, and every online review tells part of the story. The real question is, is it a story you want to be part of?

Don’t get swept away by fancy equipment or big promises. Ask the right questions. Look at the figures. Trust your instincts but make sure your accountant agrees with them!

Because after all, the only hole you want after buying a practice should be in a tooth not in your wallet.

Frequently Asked Questions

What’s the most important factor to consider before buying a dental practice?

The location tops the list, footfall, visibility, and local demographics all play a huge role in patient flow and business success.

How do I know if a dental practice’s patient list is truly valuable?

Look beyond the number, check how many patients are active (seen in the last 12–24 months) and whether new patients are regularly signing up.

What does EBITDA mean and why should I care?

EBITDA (Earnings Before Interest, Tax, Depreciation, and Amortisation) is a key indicator of profitability. It gives a clearer picture of how well the business is actually performing. It gives a much better picture of the finances of the business than just the income. It is also how a dental practice is valued when negotiating a price.

How can I check a practice’s reputation before buying?

Read Google reviews, explore their social media, look on sites like TrustPilot ask about patient loyalty and recall rates, and speak to locals if possible.

Should I be worried about high staff turnover?

Yes, frequent staff changes can indicate low morale or management issues. A stable, experienced team is a good sign.

What kind of practice should I buy- NHS, private, or mixed?

It depends on your experience and goals. NHS brings consistency, private allows flexibility and growth, and mixed gives you a bit of both.

What legal checks should I do before buying a practice?

Review the CQC report, check the lease (if leasehold), look for past NHS clawbacks, and make sure there are no outstanding issues with CQC or GDC. Consult with a solicitor who has experience in the dental sector before making any decisions.

Can I grow the business after I buy it?

Absolutely! Look for unused services you can offer, potential to expand hours, space to add surgeries, or digital marketing improvements.

Glossary: Key Terms to Know

- EBITDA: Earnings Before Interest, Tax, Depreciation, and Amortisation – A measure of a business’s actual profit before complicated accounting adjustments.

- Footfall: The number of people who pass by or enter a location – used to judge how busy or visible a place is.

- Demographics: Statistical data about a population, like age, income, or lifestyle – useful to understand what kind of patients a practice might attract.

- Turnover: The total income a business generates over a certain period – essentially how much money is coming in.

- Overheads: Ongoing costs required to run a business, like rent, salaries, utilities, and equipment.

- Goodwill: The non-physical value of a business – built from things like its reputation, loyal patients, and brand recognition.

- TUPE: Transfer of Undertakings (Protection of Employment) – UK law that protects employees when a business is sold, meaning they transfer to the new owner under the same contract.

- NHS Clawback: A repayment required if a dental practice fails to meet its NHS treatment targets (measured in UDAs).

- UDA (Units of Dental Activity): A way the NHS measures dental treatments – each treatment type is worth a set number of UDAs.

- Leasehold vs Freehold:

- Leasehold: You rent the premises.

- Freehold: You own the property outright.

- Brand Recognition: How well people know and trust a business by name or logo – essential for attracting and keeping patients.

- Digital Footprint: The online presence of a business, including its website, social media, and online reviews.

Learn more: Related Articles

About the Author

Neha Jain

Neha Jain is a skilled content writer with a rich background in business and financial knowledge. With a bachelor’s degree in English Literature and Psychology, Neha has honed her writing skills, furthering her expertise with the Content Writing Master Course (CWMC) at IIM SKILLS and a Content Marketing Certification from HubSpot Academy.

Working alongside our business development experts, Neha specialises in helping accountants, dentists and other healthcare professionals start, scale and sell their businesses.

Reviewed By:

Arun Mehra

Samera CEO

Arun, CEO of Samera, is an experienced accountant and dental practice owner. He specialises in accountancy, financial directorship, squat practices and practice management.

Buying a Dental Practice: Get Started

When buying a dental practice (especially if it’s for the first time), you need the competent hands of qualified professionals. Not only have we been helping the UK’s dentists to buy, start and sell dental practices for over 20 years, we are dental practice owners ourselves! We know what it takes to buy the right dental practice, we can help you find it, buy it and get it up and running.

Book a free, no-obligation consultation with one of our team at a time that suits you (including evenings). We’ll call you back and have a chat about how we can help buy your dream practice.

With Samera Business Advisors you can rest easy knowing that your investment is secure and your future is brighter. Contact us today so we can help plan for your tomorrow.

Learn More: Buying a Dental Practice

For more information please check out the articles and webinars in the buying a dental practice section of our Learning Centre like the Guide to Buying a Dental Practice.

Make sure you never miss any of our articles, webinars, videos or events by following us on Facebook, LinkedIn, YouTube and Instagram.